When preparing financial statements, the economic life of the business is divided into time periods. This accounting period concept requires that revenues and expenses be reported in the proper period. To determine the proper period, accountants use generally accepted accounting principles (GAAP), which requires the accrual basis of accounting.

Under the accrual basis of accounting, revenues are reported on the income statement in the period in which they are earned. For example, revenue is reported when the services are provided to customers. Cash may or may not be received from customers during this period. The accounting concept supporting this reporting of revenues is called the revenue recognition concept.

Under the accrual basis, expenses are reported in the same period as the revenues to which they relate. For example, utility expenses incurred in December are reported as an expense and matched against December’s revenues even though the utility bill may not be paid until January. The accounting concept supporting reporting revenues and related expenses in the same period is called the matching concept, or matching principle. By matching revenues and expenses, net income or loss for the period is properly reported on the income statement.

Although GAAP requires the accrual basis of accounting, some businesses use the cash basis of accounting. Under the cash basis of accounting, revenues and expenses are reported on the income statement in the period in which cash is received or paid. For example, fees are recorded when cash is received from clients; likewise, wages are recorded when cash is paid to employees. The net income (or net loss) is the difference between the cash receipts (revenues) and the cash payments (expenses).

Small service businesses may use the cash basis, because they have few receivables and payables. For example, attorneys, physicians, and real estate agents often use the cash basis. For them, the cash basis provides financial statements similar to those of the accrual basis. For most large businesses, however, the cash basis will not provide accurate financial statements for user needs. For this reason, the accrual basis is used in this text.

1. The Adjusting Process

At the end of the accounting period, many of the account balances in the ledger are reported in the financial statements without change. For example, the balances of the cash and land accounts are normally the amounts reported on the balance sheet. Some accounts, however, require updating for the following reasons:[1]

- Some expenses are not recorded daily. For example, the daily use of supplies would require many entries with small amounts. Also, the amount of supplies on hand on a day-to-day basis is normally not needed.

- Some revenues and expenses are incurred as time passes rather than as separate transactions. For example, rent received in advance (unearned rent) expires and becomes revenue with the passage of time. Likewise, prepaid insurance expires and becomes an expense with the passage of time.

- Some revenues and expenses may be unrecorded. For example, a company may have provided services to customers that it has not billed or recorded at the end of the accounting period. Likewise, a company may not pay its employees until the next accounting period even though the employees have earned their wages in the current period.

The analysis and updating of accounts at the end of the period before the financial statements are prepared is called the adjusting process. The journal entries that bring the accounts up to date at the end of the accounting period are called adjusting entries. All adjusting entries affect at least one income statement account and one balance sheet account. Thus, an adjusting entry will always involve a revenue or an expense account and an asset or a liability account.

2. Types of Accounts Requiring Adjustment

Four basic types of accounts require adjusting entries as shown below.

- Prepaid expenses Accrued revenues

- Unearned revenues Accrued expenses

Prepaid expenses are the advance payment of future expenses and are recorded as assets when cash is paid. Prepaid expenses become expenses over time or during normal operations. To illustrate, the following transaction of NetSolutions from Chapter 2 is used.

Dec. 1 NetSolutions paid $2,400 as a premium on a one-year insurance policy.

On December 1, the cash payment of $2,400 was recorded as a debit to Prepaid Insurance and credit to Cash for $2,400. At the end of December, only $200 ($2,400 divided by 12 months) of the insurance premium is expired and has become an expense. The remaining $2,200 of prepaid insurance will become an expense in future months. Thus, the $200 is insurance expense of December and should be recorded with an adjusting entry.

Other examples of prepaid expenses include supplies, prepaid advertising, and prepaid interest.

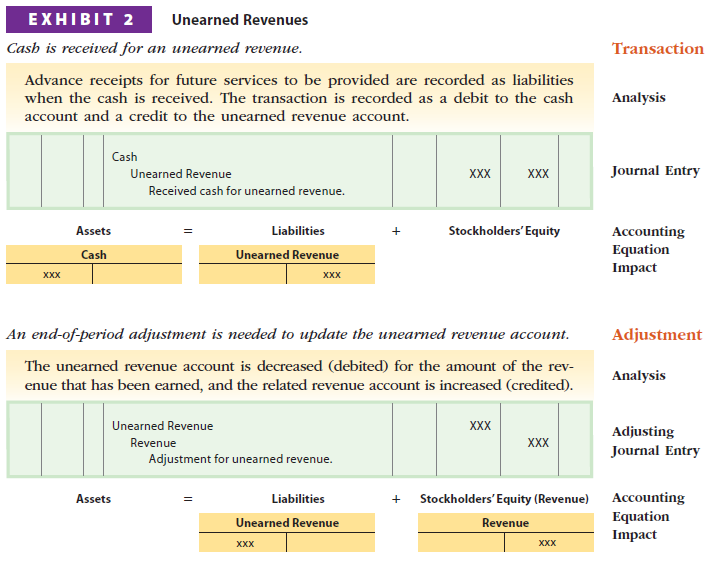

Unearned revenues are the advance receipt of future revenues and are recorded as liabilities when cash is received. Unearned revenues become earned revenues over time or during normal operations. To illustrate, the following December 1 transaction of NetSolutions is used.

Dec. 1 NetSolutions received $360 from a local retailer to rent land for three months.

On December 1, the cash receipt of $360 was recorded as a debit to Cash and a credit to Unearned Rent for $360. At the end of December, $120 ($360 divided by 3 months) of the unearned rent has been earned. The remaining $240 will become rent revenue in future months. Thus, the $120 is rent revenue of December and should be recorded with an adjusting entry.

Other examples of unearned revenues include tuition received in advance by a school, an annual retainer fee received by an attorney, premiums received in advance by an insurance company, and magazine subscriptions received in advance by a publisher.

Exhibit 2 summarizes the nature of unearned revenues.

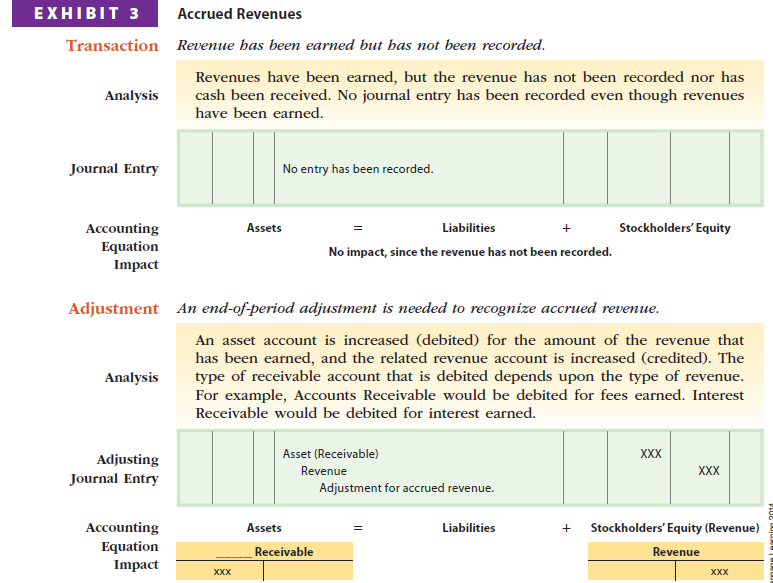

Accrued revenues are unrecorded revenues that have been earned and for which cash has yet to be received. Fees for services that an attorney or a doctor has provided but not yet billed are accrued revenues. To illustrate, the following example involving NetSolutions and one of its customers is used.

Dec. 15 NetSolutions signed an agreement with Dankner Co. under which NetSolutions will bill Dankner Co. on the fifteenth of each month for services rendered at the rate of $20 per hour.

From December 16-31, NetSolutions provided 25 hours of service to Dankner Co. Although the revenue of $500 (25 hours X $20) has been earned, it will not be billed until January 15. Likewise, cash of $500 will not be received until Dankner pays its bill. Thus, the $500 of accrued revenue and the $500 of fees earned should be recorded with an adjusting entry on December 31.

Other examples of accrued revenues include accrued interest on notes receivable and accrued rent on property rented to others.

Exhibit 3 summarizes the nature of accrued revenues.

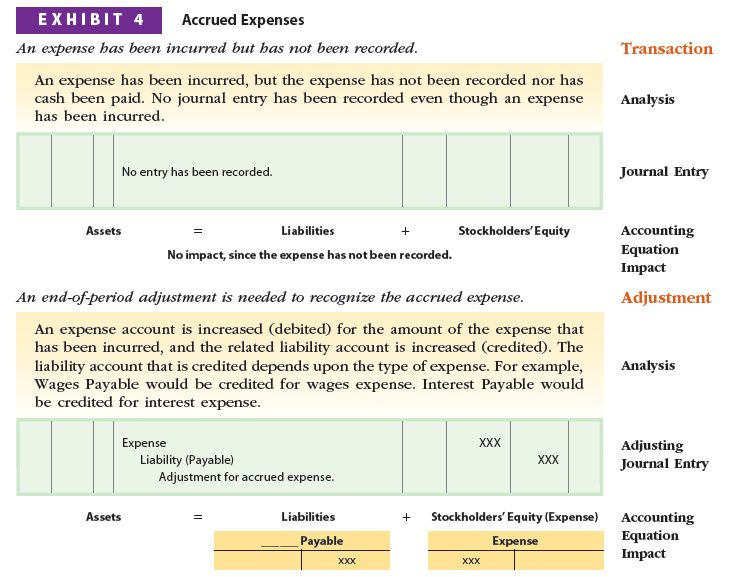

Accrued expenses are unrecorded expenses that have been incurred and for which cash has yet to be paid. Wages owed to employees at the end of a period but not yet paid are an accrued expense. To illustrate, the following example involving

NetSolutions and its employees is used.

Dec. 31 NetSolutions owes its employees wages of $250 for Monday and Tuesday, December 30 and 31.

NetSolutions paid wages of $950 on December 13 and $1,200 on December 27, 2013. These payments covered the biweekly pay periods that ended on those days. As of December 31, 2013, NetSolutions owes its employees wages of $250 for Monday

and Tuesday, December 30 and 31. The wages of $250 will be paid on January 10, 2014; however, they are an expense of December. Thus, $250 of accrued wages should be recorded with an adjusting entry on December 31.

Other examples of accrued expenses include accrued interest on notes payable and accrued taxes.

Exhibit 4 summarizes the nature of accrued expenses.

As illustrated in Exhibits 3 and 4, accrued revenues are earned revenues that are unrecorded. The cash receipts for accrued revenues are normally received in the next accounting period. Accrued expenses are expenses that have been incurred, but are unrecorded. The cash payments for accrued expenses are normally paid in the next accounting period.

Prepaid expenses and unearned revenues are sometimes referred to as deferrals. This is because the recording of the related expense or revenue is deferred to a future period. Accrued revenues and accrued expenses are sometimes referred to as accruals. This is because the related revenue or expense should be recorded or accrued in the current period.

Source: Warren Carl S., Reeve James M., Duchac Jonathan (2013), Corporate Financial Accounting, South-Western College Pub; 12th edition.

Hi to all, it’s genuinely a good for me to pay a visit this site,

it contains priceless Information.

Appreciate this post. Let me try it out.