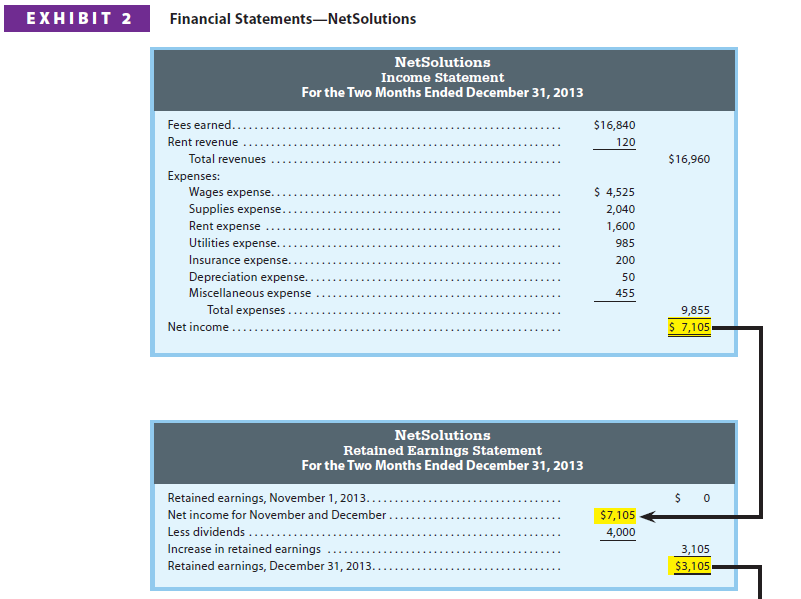

Using the adjusted trial balance shown in Exhibit 1, the financial statements for NetSolutions can be prepared. The income statement, the retained earnings statement, and the balance sheet are shown in Exhibit 2.

1. Income Statement

The income statement is prepared directly from the Adjusted Trial Balance columns of the Exhibit 1 spreadsheet, beginning with fees earned of $16,840. The expenses in the income statement in Exhibit 2 are listed in order of size, beginning with the larger items. Miscellaneous expense is the last item, regardless of its amount.

2. Retained Earnings Statement

The first item normally presented on the retained earnings statement is the balance of the retained earnings account at the beginning of the period. Since NetSolutions began operations on November 1, this balance is zero in Exhibit 2. Then, the retained earnings statement shows the net income for the two months ended December 31, 2013. The amount of dividends is deducted from the net income to arrive at the retained earnings as of December 31, 2013.

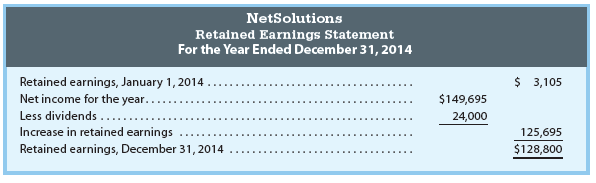

For the following period, the beginning balance of retained earnings for NetSolutions is the ending balance that was reported for the previous period. For example, assume that during 2014, NetSolutions earned net income of $149,695 and paid dividends of $24,000. The retained earnings statement for the year ending December 31, 2014, for NetSolutions is as follows:

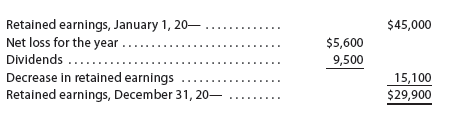

For NetSolutions, the amount of dividends was less than the net income. If the dividends had exceeded the net income, the order of the net income and the dividends would have been reversed. The difference between the two items would then be deducted from the beginning Retained Earnings balance. Other factors, such as a net loss, may also require some change in the form of the retained earnings statement, as shown in the following example:

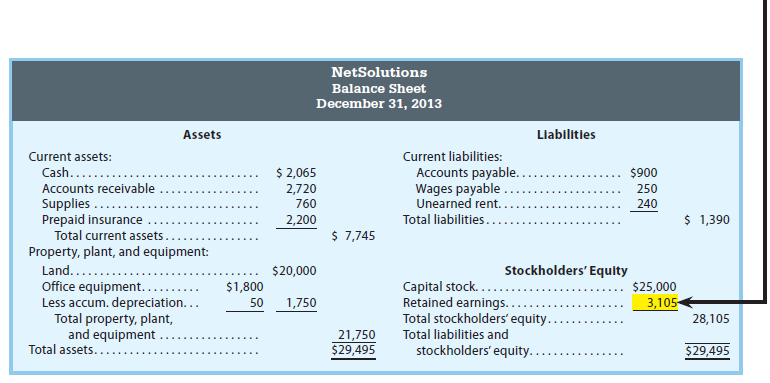

3. Balance Sheet

The balance sheet is prepared directly from the Adjusted Trial Balance columns of the Exhibit 1 spreadsheet, beginning with Cash of $2,065. The asset and liability amounts are taken from the spreadsheet. The retained earnings amount, however, is taken from the retained earnings statement, as illustrated in Exhibit 2.

The balance sheet in Exhibit 2 shows subsections for assets and liabilities. Such a balance sheet is a classified balance sheet. These subsections are described next.

Assets Assets are commonly divided into two sections on the balance sheet: (1) current assets and (2) property, plant, and equipment.

Current Assets Cash and other assets that are expected to be converted to cash or sold or used up usually within one year or less, through the normal operations of the business, are called current assets. In addition to cash, the current assets may include notes receivable, accounts receivable, supplies, and other prepaid expenses.

Notes receivable are amounts that customers owe. They are written promises to pay the amount of the note and interest. Accounts receivable are also amounts customers owe, but they are less formal than notes. Accounts receivable normally result from providing services or selling merchandise on account. Notes receivable and accounts receivable are current assets because they are usually converted to cash within one year or less.

Property, Plant, and Equipment The property, plant, and equipment section may also be described as fixed assets or plant assets. These assets include equipment, machinery, buildings, and land. With the exception of land, as discussed in Chapter 3, fixed assets depreciate over a period of time. The original cost, accumulated depreciation, and book value of each major type of fixed asset are normally reported on the balance sheet or in the notes to the financial statements.

Liabilities Liabilities are the amounts the business owes to creditors. Liabilities are commonly divided into two sections on the balance sheet: (1) current liabilities and (2) long-term liabilities.

Current Liabilities Liabilities that will be due within a short time (usually one year or less) and that are to be paid out of current assets are called current liabilities. The most common liabilities in this group are notes payable and accounts payable. Other current liabilities may include Wages Payable, Interest Payable, Taxes Payable, and Unearned Fees.

Long-Term Liabilities Liabilities that will not be due for a long time (usually more than one year) are called long-term liabilities. If NetSolutions had long-term liabilities, they would be reported below the current liabilities. As long-term liabilities come due and are to be paid within one year, they are reported as current liabilities. If they are to be renewed rather than paid, they would continue to be reported as long term. When an asset is pledged as security for a liability, the obligation may be called a mortgage note payable or a mortgage payable.

Stockholders’ Equity The stockholders’ right to the assets of the business is presented on the balance sheet below the liabilities section. The stockholders’ equity is added to the total liabilities, and this total must be equal to the total assets. The stockholders’ equity consists of capital stock and retained earnings.

Source: Warren Carl S., Reeve James M., Duchac Jonathan (2013), Corporate Financial Accounting, South-Western College Pub; 12th edition.

There is visibly a lot to realize about this. I assume you made various nice points in features also.