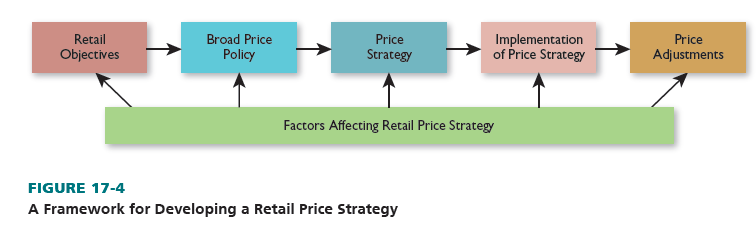

As Figure 17-4 shows, a retail price strategy has five steps: objectives, policy, strategy, implementation, and adjustments. Pricing policies must be integrated with the total retail mix, which occurs in the second step. The process can be complex due to the often erratic nature of demand, the number of items carried, and the impact of the external factors already noted.

1. Retail Objectives and Pricing

A retailer’s pricing strategy has to reflect its overall goals and be related to sales and profits. There must also be specific pricing goals to avoid such potential problems as confusing people by having too many prices, spending too much time bargaining with customers, offering frequent discounts to stimulate customer traffic, having low profit margins, and placing too much focus on price.

OVERALL OBJECTIVES AND PRICING Sales goals may be stated in terms of revenues and/or units. An aggressive strategy, known as market penetration pricing, is used when a retailer seeks large revenues by setting low prices and selling many units. Profit per unit is low, but total profit is high if sales projections are met. This approach is proper if customers are price sensitive, low prices discourage actual and potential competition, and retail costs do not rise much with volume.

With a market skimming pricing strategy, a firm sets premium prices and attracts customers less concerned with price than service, assortment, and prestige. It usually does not maximize sales but achieves high profit per unit. It is proper if the targeted segment is price insensitive, if new competitors are unlikely to enter the market, and if added sales will greatly increase retail costs. See Figure 17-5.

Return on investment and early recovery of cash are other possible profit-based goals for retailers using a market skimming strategy. Return on investment is sought if a retailer wants profit to be a certain percentage of its investment, such as 20 percent of inventory investment. Early recovery of cash is used by retailers that may be short on funds, wish to expand, or be uncertain about the future.

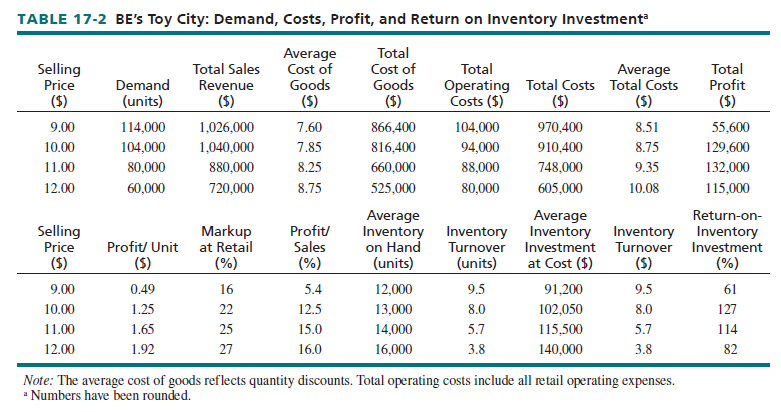

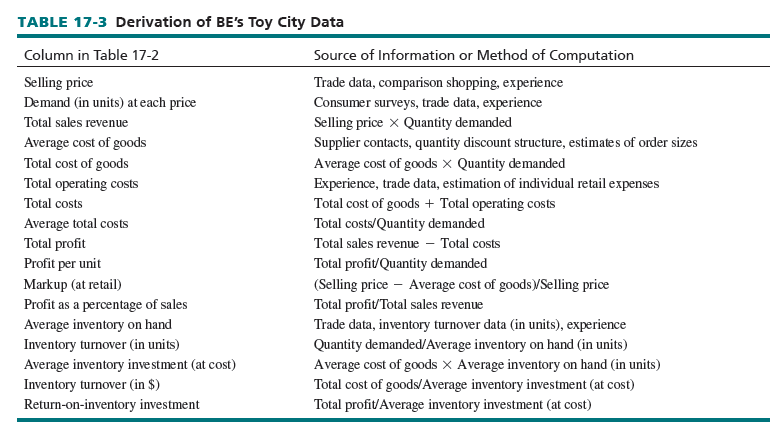

BE’s Toy City, the discounter we introduced earlier in this chapter, may be used to illustrate how a retailer sets sales, profit, and return-on-investment goals. The firm sells inexpensive toys and overruns to avoid competing with mainstream toy stores, has one price for all toys (to be set within the $9 to $12 range), minimizes operating costs, encourages self-service, and carries a good selection. Table 17-2 has data on BE’s Toy City pertaining to demand, costs, profit, and returnon-inventory investment at prices from $9 to $12. The firm must select the best price within that range. Table 17-3 shows how the figures in Table 17-2 were derived. Several conclusions can be drawn from Table 17-2:

A sales revenue goal would lead to a price of $10. Total sales are highest ($1,040,000).

- A dollar profit goal would lead to a price of $11. Total profit is highest ($132,000).

- A return-on-inventory investment goal would lead to a price of $10. Return on inventory investment is 127 percent.

- Although the most items can be sold at $9, that price would lead to the least profit ($55,600).

- A price of $12 would yield the highest profit per unit ($1.92) and as a percentage of sales, but total dollar profit is not maximized at this price.

- The highest inventory turnover (9.5 times at $9.00) would not lead to the highest total profits.

As a result, BE’s Toy City decides on a price of $11 because it would earn the highest dollar profits, while generating good profit per unit and good profit as a percentage of sales.

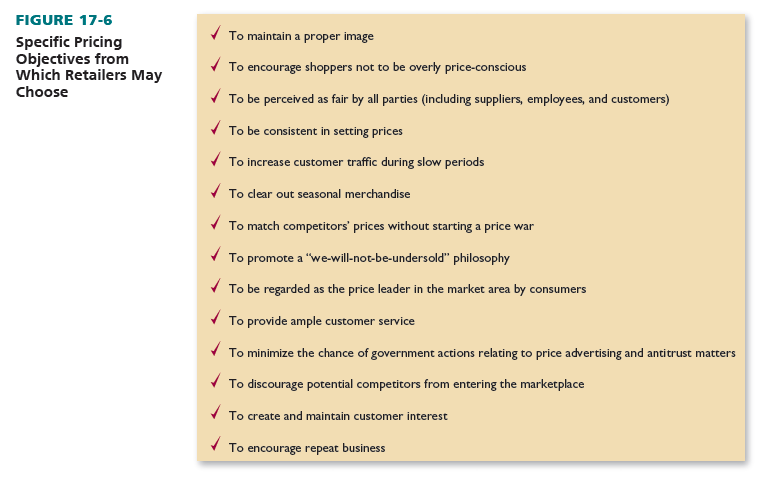

SPECIFIC PRICING OBJECTIVES Figure 17-6 lists specific pricing goals other than sales and profits. Each retailer must determine its relative importance for its situation—and plan accordingly. Some goals may be incompatible, such as “to not encourage shoppers to be overly price-conscious” and a “we-will-not-be-undersold” philosophy.

2. Broad Price Policy

Through a broad price policy, a retailer generates an integrated price plan with short- and long-run perspectives (balancing immediate and future goals) and a consistent image (vital for chains and franchises). The retailer interrelates price policy with the target market, the retail image, and the other elements of the retail mix. These are some price policies from which a firm could choose:

- No competitors will have lower prices, no competitors will have higher prices (for prestige purposes), or prices will be consistent with competitors’ prices.

- All items will be priced independently, depending on the demand for each, or the prices for all items will be interrelated to maintain an image and ensure proper markups.

- Price leadership will be exerted, competitors will be price leaders and set prices first, or prices will be set independently of competitors.

- Prices will be constant over a year or season, or prices will change if costs change.

3. Price Strategy

In demand-oriented pricing, a retailer sets prices based on consumer desires. It determines the range of prices acceptable to the target market. The top of this range is the demand ceiling—the most that people will pay for a good or service. With cost-oriented pricing, a retailer sets a price floor, the minimum price acceptable to the firm so it can reach a specified profit goal. A retailer usually computes merchandise and operating costs and adds a profit margin to these figures. For competition-oriented pricing, a retailer sets its prices in accordance with those of its competitors. The price levels of key competitors are studied and applied.

As a rule, retailers should combine these approaches in enacting a price strategy. The approaches should not be viewed as operating independently.

DEMAND-ORIENTED PRICING Retailers use demand-oriented pricing to estimate the quantities that customers would buy at various prices. This approach studies customer interests and the psychological implications of pricing. Two aspects of psychological pricing are the price-quality association and prestige pricing.

According to the price-quality association concept, many consumers believe high prices connote high quality and low prices connote low quality. This association is especially important if competing firms or products are hard to judge on bases other than price, consumers have little experience or confidence in judging quality (as with a new retailer), shoppers perceive large differences in quality among retailers or products, and brand names are insignificant in product choice. Although various studies have documented a price-quality relationship, research also indicates that if other quality cues—such as retailer atmospherics, customer service, and popular brands—are involved, these cues may be more important than price in a person’s judgment of overall retailer or product quality.

Prestige pricing—which assumes that consumers will not buy goods and services at prices deemed too low—is based on the price-quality association. Its premise is that consumers may feel too low a price means poor quality and status. Some people look for prestige pricing when selecting retailers and do not patronize those with prices viewed as too low. Saks Fifth Avenue and Neiman Marcus do not generally carry low-end items because their customers may believe such items are inferior. Prestige pricing does not apply to all shoppers. Some people may be economizers and always shop for bargains; and neither the price-quality association nor prestige pricing may be applicable for them.

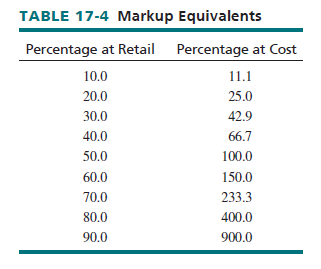

COST-ORIENTED PRICING One form of cost-oriented pricing, markup pricing, is the most widely used pricing technique. In markup pricing, a retailer sets prices by adding per-unit merchandise costs, retail operating expenses, and desired profit. The difference between merchandise costs and selling price is the markup. If a retailer buys a desk for $200 and sells it for $300, the extra $100 covers operating costs and profit. The markup is 33-1/3 percent at retail or 50 percent at cost. The markup level depends on a product’s traditional markup, the supplier’s suggested list price, inventory turnover, competition, rent and other overhead costs, the extent to which the product must be serviced, and the selling effort.

Markups can be computed on the basis of retail selling price or cost but are usually calculated using the retail price. Why? (1) Retail expenses, markdowns, and profit are always stated as a percentage of sales. Thus, markups as a percentage of sales are more meaningful. (2) Manufacturers quote selling prices and discounts to retailers as percentage reductions from retail list prices. (3) Retail price data are more readily available than cost data. (4) Profitability seems smaller if expressed on the basis of price. This can be useful in communicating with the government, employees, and consumers.

This is how a markup percentage is calculated. The difference is in the denominator:

Table 17-4 shows several markup percentages at retail and at cost. As markups go up, the disparity between the percentages grows. Suppose a retailer buys a watch for $20 and considers whether to sell it for $25, $40, or $100. The $25 price yields a markup of 20 percent at retail and 25 percent at cost, the $40 price a markup of 50 percent at retail and 100 percent at cost, and the $100 price a markup of 80 percent at retail and 400 percent at cost.

The following three examples indicate the usefulness of the markup concept in planning:

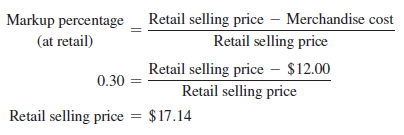

1. A discount clothing store can buy a shipment of men’s long-sleeve shirts at $12 each and wants a 30 percent markup at retail.9 What retail price should the store charge to achieve this markup?

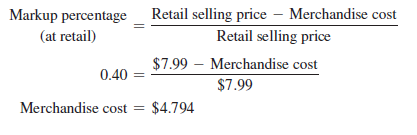

2. A stationery store desires a minimum 40 percent markup at retail.10 If standard envelopes retail at $7.99 per box, what is the maximum price the store should pay for each box?

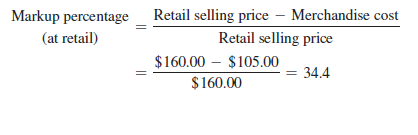

3. A sporting goods store has been offered a closeout purchase for bicycles. The cost of each bike is $105, and it should retail for $160. What markup percentage at retail would the store obtain?

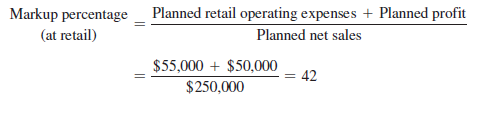

A retailer’s markup percentage may also be determined by examining planned retail operating expenses, profit, and net sales. Suppose a florist estimates yearly operating expenses to be $55,000. The desired profit is $50,000 per year, including the owner’s salary. Net sales are forecast to be $250,000. The planned markup percentage would be:

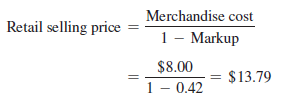

If potted plants cost the florist $8.00 each, the retailer’s selling price would be: Retail selling price =

The florist must sell about 18,129 plants (assuming this is the only item it carries) at $13.79 apiece to achieve sales and profit goals. To reach these goals, all plants must be sold at the $13.79 price.

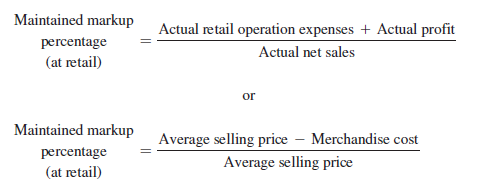

Because it is rare to sell all items in stock at their original prices, initial markup, maintained markup, and gross margin should each be computed. Initial markup is based on the original retail value assigned to merchandise less the costs of the merchandise. Maintained markup is based on the actual prices received for merchandise sold during a time period less merchandise cost. Maintained markups relate to actual prices received, so they can be hard to predict. The difference between initial and maintained markups is that the latter reflect adjustments for markdowns, added markups, shortages, and discounts.

The initial markup percentage depends on planned retail operating expenses, profit, reductions, and net sales:

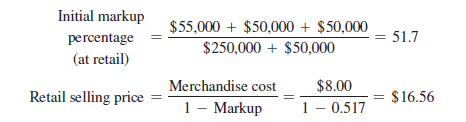

If planned retail reductions are 0, the initial markup percentage equals planned retail operating expenses plus profit, both divided by planned net sales. To resume the florist example, suppose the firm projects that retail reductions will be 20 percent of estimated sales, or $50,000. To reach its goals, the initial markup and the original selling price would be:

The original retail value of 18,129 plants is about $300,000. Retail reductions of $50,000 lead to net sales of $250,000. Thus, the retailer must begin by selling plants at $16.56 apiece if it wants an average selling price of $13.79 and a maintained markup of 42 percent.

The maintained markup percentage is:

Gross margin is the difference between net sales and the total cost of goods sold (which adjusts for cash discounts and additional expenses):

Gross margin (in $) = Net sales — Total cost of goods

The florist’s gross margin (the dollar equivalent of maintained markup) is roughly $105,000.

Although a retailer must set a companywide markup goal, markups for categories of merchandise or individual products may differ—sometimes dramatically. At many full-line discount stores, maintained markup as a percentage of sales ranges from under 20 percent for consumer electronics to as much as 30 to 40 percent or more for jewelry and watches.

With a variable markup policy, a retailer purposely adjusts markups by merchandise category.

- A variable markup policy recognizes that costs of different goods/services categories may fluctuate widely. Some items require alterations or installation. Even within a product line, expensive items may require greater end-of-year markdowns than inexpensive ones. The high- priced line needs a larger initial markup.

- A variable markup policy allows for differences in product investments. For major appliances, where the retailer orders regularly from a wholesaler, lower markups are needed than with fine jewelry, where the retailer must have a complete stock of unique merchandise.

- A variable markup policy accounts for differences in sales efforts and merchandising skills. For example, a feature-laden food processor may require a substantial effort, whereas a standard toaster involves much less effort.

- A variable markup policy may help a retailer to generate more customer traffic by advertising certain products at deep discounts. This entails leader pricing (discussed later in the chapter).

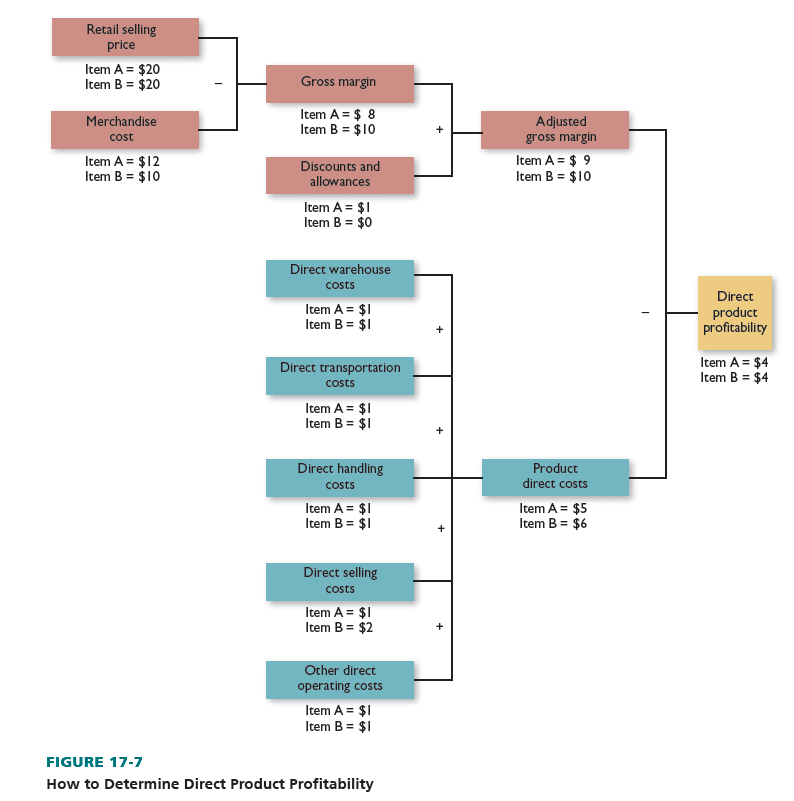

One way to plan variable markups is direct product profitability (DPP), a technique that enables a retailer to find the profitability of each category of merchandise by computing adjusted per-unit gross margin and assigning direct product costs for such expense categories as warehousing, transportation, handling, and selling. The proper markup for each category or item is then set. Direct product profitability is used by some supermarkets, discounters, and other retailers. However, it is complex to assign costs.

Figure 17-7 illustrates DPP for two items with a selling price of $20. The retailer pays $12 for Item A; per-unit gross margin is $8. Since the retailer gets a $1 per unit allowance to set up a special display, the adjusted gross margin is $9. Total direct retail costs are estimated at $5. Direct product profit is $4 (20 percent of sales). The retailer pays $10 for Item B; per-unit gross margin is $10. There are no special discounts or allowances. Because Item B needs more selling effort, total direct retail costs are $6. The direct profit is $4 (20 percent of sales). To attain the same direct profit per unit, Item A needs a 40 percent markup (per-unit gross margin/selling price), and Item B needs 50 percent.

Cost-oriented (markup) pricing is popular among retailers. It is simple, because a retailer can apply a standard markup for a product category more easily than it can estimate demand at various prices. The firm can also adjust prices according to demand or segment its customers. Markup pricing has a sense of equity given that the retailer earns a fair profit. When retailers have similar markups, price competition is reduced. Markup pricing is efficient if it takes into account competition, seasonal factors, and the intricacies in selling some products.

COMPETITION-ORIENTED PRICING A retailer can use competitors’ prices as a guide. That firm might not alter prices in reaction to changes in demand or costs unless competitors alter theirs. Similarly, it might change prices when competitors do, even if demand or costs remain the same.

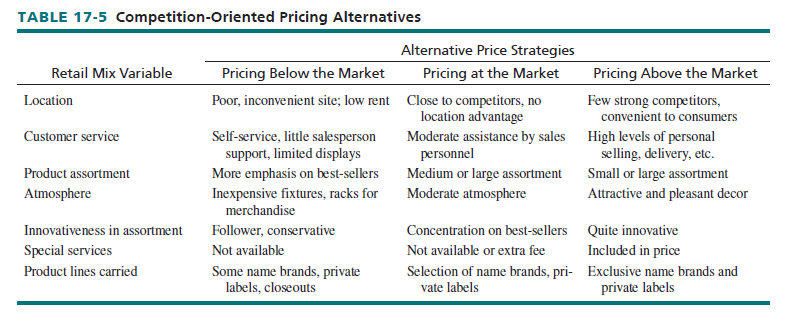

As shown in Table 17-5, a competition-oriented retailer can price below, at, or above the market. A firm with a strong location, superior service, good assortments, a favorable image, and exclusive brands can set prices above competitors. However, above-market pricing is not suitable for a retailer that has an inconvenient location, relies on self-service, is not innovative, and offers no real product distinctiveness.

Competition-oriented pricing does not require calculations of demand curves or price elasticity. The average market price is assumed to be fair for both the consumer and the retailer. Pricing at the market level does not disrupt competition and therefore does not usually lead to retaliation.

INTEGRATION OF APPROACHES TO PRICE STRATEGY To properly integrate the three approaches— demand-oriented pricing, cost-oriented pricing, and competition-oriented pricing—questions such as these should be addressed:

- If prices are reduced, will revenues increase greatly? (Demand orientation)

- Should different prices be charged for a product based on negotiations with customers, seasonality, and so on? (Demand orientation)

- Will a given price level allow a traditional markup to be attained? (Cost orientation)

- What price level is needed for an item with special buying, selling, or delivery costs? (Cost orientation)

- What price levels are competitors setting? (Competitive orientation)

- Can above-market prices be set due to a superior image? (Competitive orientation)

NEW USES FOR CREDIT AND DEBIT CARDS According to a leading research and consulting firm, the sales of pre-paid credit and debit cards grew from $12 billion in 2007 to more than $235 billion in 2015 and accounted for 4 percent of all payment card purchases with retailers.11 This high growth rate can be explained by two developments: the increase in the gift card market and the greater number of consumers who do not have traditional bank accounts.

Firms such as Home Depot (www.homedepot.com), Gap (www.gap.com), and Nike (www.nike .com) offer closed-loop (firm-specific) gift cards. Visa (www.visa.com), MasterCard (www .mastercard.com), Discover (www.discovercard.com), and American Express (www.american express.com) offer open-loop gift cards that can be redeemed by any merchant.

The growth in pre-paid cards and gift cards has encouraged convenience stores to enter the banking business. Stripes (www.stripesstores.com), which operates about 700 convenience stores—primarily in New Mexico, Oklahoma, and Texas—offers a pre-paid credit card in conjunction with nFinanSe (www.nfinanse.com), a financial services company. For a $2.95 monthly fee, Stripes customers can participate in the firm’s credit-card programs. This fee entitles users to an unlimited number of purchase transactions, no-cost direct deposit of payroll checks, and 24/7 customer support. The card is particularly attractive to Stripes because it operates in markets where a high percentage of consumers do not have traditional bank accounts. Stripes is now a subsidiary of Energy Transfer Partners, the parent company of Sunoco.12

4. Implementation of Price Strategy

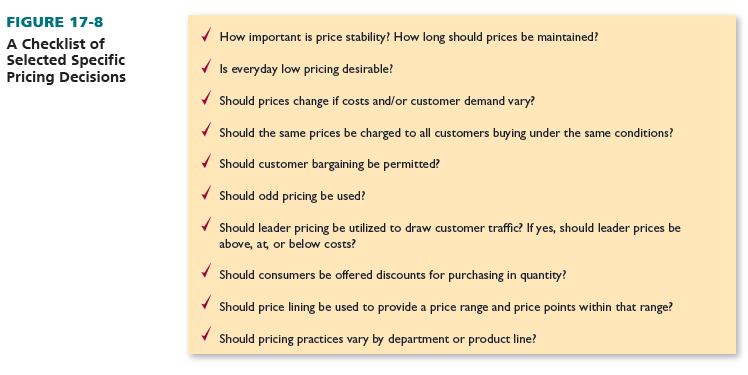

Implementing a price strategy involves a variety of separate but interrelated specific decisions, in addition to those broad concepts already discussed. A checklist of selected decisions is shown in Figure 17-8. In this section, the specifics of a pricing strategy are detailed.

CUSTOMARY AND VARIABLE PRICING With customary pricing, a retailer sets prices for goods and services and seeks to maintain them for an extended period. Examples of items with customary prices are newspapers, candy, arcade games, vending machine items, and foods on restaurant menus. In each case, the retailer wants to establish set prices and have consumers take them for granted.

A version of customary pricing is everyday low pricing (EDLP), in which a retailer strives to sell its goods and services at consistently low prices throughout the selling season. Low prices are set initially, and there are few or no advertised specials, except on discontinued items or end- of-season closeouts. The retailer reduces its advertising and product re-pricing costs, and this approach increases the credibility of its prices in the consumer’s mind. On the other hand, with EDLP, suppliers may eliminate special trade allowances designed to encourage retailers to offer price promotions during the year. Walmart, McDonald’s, and Ikea are among the retailers successfully using everyday low pricing. See Figure 17-9.

In many instances, a retailer cannot or should not use customary pricing. A firm cannot hold constant prices if costs are rising. A firm should not keep prices constant if customer demand varies. Under variable pricing, a retailer alters its prices to coincide with fluctuations in costs or consumer demand. Variable pricing may offer excitement due to special sales opportunities for customers.

Cost fluctuations can be seasonal or trend-related. Supermarket and florist prices vary over the year due to the seasonal nature of many food and floral products. When seasonal items are scarce, the cost to the retailer goes up. If costs continually rise (as with luxury cars) or fall (as with computers), the retailer must change prices permanently (unlike temporary seasonal changes).

Demand fluctuations can be place- or time-based. Place-based fluctuations exist for retailers selling seat locations (such as concert halls) or room locations (such as hotels). Different prices can be charged for different locales, such as tickets close to the stage commanding higher prices. Time- based fluctuations occur if consumer demand differs by hour, day, or season. Demand for a movie theater is greater on Saturday than on Wednesday. Prices should be lower in periods of less demand.

Yield management pricing is a computerized, demand-based, variable pricing technique whereby a retailer (typically a service firm) determines the combination of prices that yield the greatest total revenues for a given period. It is widely used by airlines and hotels. A key airline decision is how many first-class, full-coach, and discount tickets to sell on each flight. With this approach, an airline has fewer discount tickets in peak periods than in off-peak times. The airline has two goals: fill as many seats as possible on every flight and sell as many full-fare tickets as it can. (An airline doesn’t want to sell a seat for $199 if someone will pay $599!) Yield management pricing may be too complex for small firms and requires software

It is possible to combine customary and variable pricing. A movie theater can charge $5 each Wednesday night and $9 every Saturday. A bookstore can lower prices by 20 percent for bestsellers that have been on shelves for three months.

ONE-PRICE POLICY AND FLEXIBLE PRICING Under a one-price policy, a retailer charges the same price to all customers buying an item under similar conditions. This policy may be used together with customary pricing or variable pricing. With variable pricing, all customers interested in a particular section of concert seats would pay the same price. This approach is easy to manage, does not require skilled salespeople, makes shopping quicker, permits self-service, puts consumers under less pressure, and is tied to price goals. One-price policies are the rule for most U.S. retailers, and bargaining is often not permitted.

Flexible pricing lets consumers bargain over prices; those who are good at it obtain lower prices. Jewelry stores, car dealers, and others use flexible pricing. They post “list prices” but shoppers who are able to haggle can purchase at lower prices. Shoppers need prior knowledge to bargain well. Flexible pricing encourages consumers to spend more time, gives an impression the firm is discount-oriented, and generates high margins from shoppers who do not like haggling. It requires high initial prices and good salespeople.13

A special form of flexible pricing is contingency pricing, whereby a service retailer does not get paid until after the service is performed and payment is contingent on the service being satisfactory. In some cases, such as real-estate, consumers like contingency payments so they know the service is done properly. This represents some risk to the retailer because a lot of time and effort may be incurred without payment. A real-estate broker may show a house 25 times, not sell it, and, therefore, not be paid.

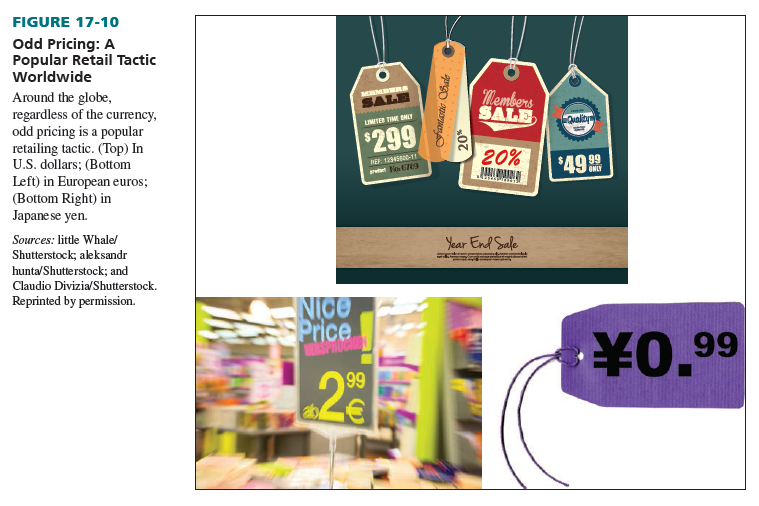

ODD PRICING In odd pricing, retail prices are set at levels below even dollar values, such as $0.49, $4.98, and $199. The assumption is that people feel these prices represent discounts or that the amounts are beneath consumer price ceilings. Odd pricing is a form of psychological pricing.14 Realtors hope consumers with a price ceiling of less than $350,000 are attracted to houses selling for $349,500. See Figure 17-10.

Odd prices that are 1 cent or 2 cents below the next highest even price ($0.29, $0.99, $2.98) are common up to $10.00. Beyond that point and up to $50.00, 5-cent reductions from the highest even price ($19.95, $49.95) are more usual. For more expensive items, prices are in dollars ($399, $4,995).

LEADER PRICING In leader pricing, a retailer advertises and sells selected items in its goods/ services assortment at less than the usual profit margins. The goal is to increase customer traffic for the retailer so that it can sell regularly priced goods and services in addition to the specially priced items. This is different from bait-and-switch, in which sale items are not sold.

Leader pricing typically involves frequently purchased, nationally branded, high-turnover goods and services because it is easy for customers to detect low prices. Supermarkets, home centers, discount stores, drugstores, and fast-food restaurants are just some of the retailers that utilize leader pricing to draw shoppers. There are two kinds of leader pricing: loss leaders and sales at lower than regular prices (but higher than cost). Loss leaders are regulated in some states under minimum-price laws.

MULTIPLE-UNIT PRICING With multiple-unit pricing, a retailer offers discounts to customers who buy in quantity or who buy a product bundle. By pricing items at two for $0.75, a retailer attempts to sell more products than at $0.39 each. There are three reasons to use multiple-unit pricing: (1) A firm could seek to have shoppers increase their total purchases of an item. (If people buy multiple units to stockpile them, instead of consuming more, the firm’s overall sales do not increase.) (2) This approach can help sell slow-moving and end-of-season merchandise. (3) Price bundling may increase sales of related items.

In bundled pricing, a retailer combines several items in one basic price. A digital camera bundle could include a camera, batteries, a telephoto lens, a case, and a tripod for $259. This approach increases overall sales and offers people a discount over unbundled prices. However, it is unresponsive to the needs of customers who vary in their needs and preferences. Many retailers offer hybrid bundles that combine complementary products(s) and service(s) for a single price; home improvement stores may charge a single price for floor tiles, installation, and disposal of previous flooring materials. As an alternative, many retailers use unbundled pricing—they charge separate prices for each product or service sold. A TV rental firm could charge separately for TV set rental, home delivery, and a monthly service contract. This closely links prices with costs and gives people more choice. Unbundled pricing may be harder to manage and may lead to people buying fewer related items.15

PRICE LINING Rather than stock merchandise at all different price levels, retailers often employ price lining and sell merchandise at a limited range of price points, with each point representing a distinct level of quality. Retailers first determine their price floors and ceilings in each product category. They then set a limited number of price points within the range. Department stores generally carry good, better, and best versions of merchandise consistent with their overall price policy—and set individual prices accordingly. See Figure 17-11.

Price lining benefits both consumers and retailers. If the price range for a box of handkerchiefs is $6 to $25 and the price points are $6, $15, and $25, consumers know that distinct product qualities exist. However, should a retailer have prices of $6, $7, $8, $9, $10, $11, $12, $13, $14, $15, $16, $17, $18, $19, $20, $21, $22, $23, $24, and $25, the consumer may be confused about product differences. For retailers, price lining aids merchandise planning. Retail buyers can seek suppliers carrying products at appropriate prices and better negotiate with suppliers. They can automatically disregard products not fitting within price lines and thereby reduce inventory investment. Also, stock turnover goes up when the number of models carried is limited.

Difficulties do exist in price lining: (1) Depending on the price points selected, price lining may leave excessive gaps. A parent shopping for a graduation gift might find a $30 briefcase to be too cheap and a $200 one to be too expensive. (2) Inflation can make it tough to keep price points and price ranges. (3) Markdowns may disrupt the balance in a price line, unless all items in a line are reduced proportionally. (4) Price lines must be coordinated for complementary product categories, such as blazers, skirts, and shoes.

5. Price Adjustments

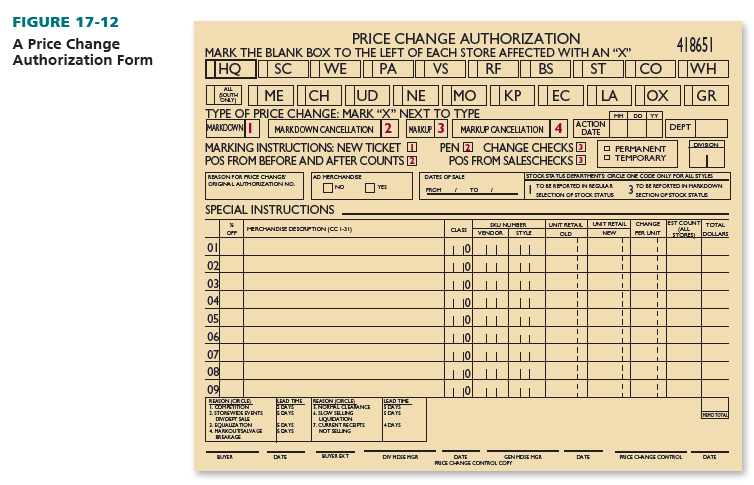

Price adjustments enable retailers to use price as an adaptive mechanism. Markdowns and additional markups may be needed due to competition, seasonality, demand patterns, merchandise costs, and pilferage. Figure 17-12 shows a price change authorization form.

A markdown from an item’s original price is used to meet the lower price of another retailer, adapt to inventory overstocking, clear out shopworn merchandise, reduce assortments of odds and ends, and increase customer traffic. An additional markup increases an item’s original price because demand is unexpectedly high or costs are rising. In today’s competitive marketplace, markdowns are applied much more frequently than additional markups.

A third price adjustment, the employee discount, is noted here because it may affect the computation of markdowns and additional markups. Although an employee discount is not an adaptive mechanism, it influences morale. Some firms give employee discounts on all items and also let workers buy sale items before they are made available to the general public.

COMPUTING MARKDOWNS AND ADDITIONAL MARKUPS Markdowns and additional markups can be expressed in dollars or percentages.

The markdown percentage is the total dollar markdown as a percentage of net sales (in dollars). Although it is simple to compute, this formula does not enable a retailer to learn the percentage of items that are marked down relative to those sold at the original price:

A complementary measure is the off-retail markdown percentage, which looks at the markdown for each item or category of items as a percentage of original retail price. The markdown percentage for every item can be computed, as well as the percentage of items marked down:

Suppose a gas barbecue grill sells for $400 at the beginning of the summer and is reduced to $280 at the end of the summer. The off-retail markdown is 30 percent [($400 — $280)/$400]. If 100 grills are sold at the original price and 20 are sold at the sale price, the percentage of items marked down is 17 percent, and the total dollar markdown is $2,400.

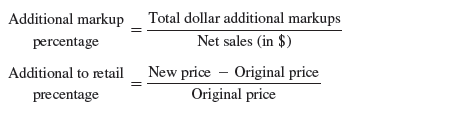

The additional markup percentage looks at total dollar additional markups as a percentage of net sales, whereas the addition to retail percentage measures a price rise as a percentage of the original price:

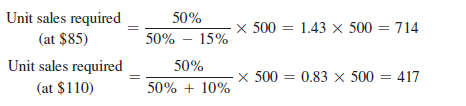

Retailers must realize that many more customers would have to buy at reduced prices for those retailers to have a total gross profit equal to that at higher prices. A retailer’s judgment regarding price adjustments is affected by operating costs at various sales volumes and customer price elasticities. The true impact of a markdown or an additional markup can be learned from this formula:

Suppose a Brother printer with a cost of $50 has an original retail price of $100 (a markup of 50 percent). A retailer expects to sell 500 units over the next year, generating a total gross profit of $25,000 ($50 X 500). How many units does the retailer have to sell if it reduces the price to $85 or raises it to $110—and still earn a $25,000 gross profit? Here are the answers:

MARKDOWN CONTROL Through markdown control, a retailer evaluates the number of mark- downs, the proportion of sales involving markdowns, and the causes. The control must be such that buying plans can be altered in later periods to reflect markdowns. A good way to evaluate the cause of markdowns is to have retail buyers record the reasons for each markdown and then examine them periodically. Possible buyer notations are “end of season,” “to match the price of a competitor,” and “obsolete style.”

Through markdown control, a retailer can monitor policies, such as the way items are displayed. Careful planning may also enable a retailer to avoid some markdowns by running more ads, training workers better, shipping goods more efficiently among branch units, and returning items to vendors.

The need for markdown control should not be interpreted as meaning that all markdowns can or should be minimized or eliminated. In fact, too low a markdown percentage may indicate that a retailer’s buyers have not assumed enough risk in purchasing goods.

TIMING MARKDOWNS There are different perspectives among retailers about the best markdown timing sequence, but much can be said about the benefits of an early markdown policy: It requires lower markdowns to sell products than markdowns late in the season. Merchandise is offered at reduced prices while demand is still fairly active. Early markdowns free selling space for new merchandise. The retailer’s cash flow position can be improved. The main advantage of a late markdown policy is that a retailer gives itself every opportunity to sell merchandise at original prices. Yet, the advantages associated with an early markdown policy cannot be achieved under a late markdown policy.

Retailers can also use a staggered markdown policy and discount prices throughout a selling period. One pre-planned staggered markdown policy is an automatic markdown plan, in which the amount and timing of markdowns are controlled by the length of time merchandise remains in stock.

A storewide clearance, done once or twice a year, is another way to time markdowns. It often takes place after peak selling periods such as Christmas and Mother’s Day. The goal is to clear out merchandise before taking a physical inventory and beginning the next season. The advantages of a storewide clearance are that a longer period is provided for selling items at original prices and that frequent markdowns can destroy a consumer’s confidence in regular prices: “Why buy now, when it will be on sale next week?” Clearance sales limit bargain hunting to once or twice a year.

In the past, many retailers would introduce merchandise at high prices and then mark down many items by as much as 60 percent to increase store traffic and improve inventory turnover. This caused customers to wait for price reductions and treat initial prices skeptically. Today, more retailers start out with lower prices and try to run fewer sales and apply fewer markdowns than before. Nonetheless, a big problem facing some retailers is that they have gotten consumers too used to buying when items are discounted.

One interesting example of markdown management support is Markdown Manager software that eBay offers as a service for its sellers (http://pages.ebay.com/help/sell/items_on_sale.html).

Source: Barry Berman, Joel R Evans, Patrali Chatterjee (2017), Retail Management: A Strategic Approach, Pearson; 13th edition.

Good info. Lucky me I reach on your website by accident, I bookmarked it.