1. Business Checking Accounts

One of your first tasks as a new business owner is to obtain a checking account. I remember my very first business and the feeling of seeing my company’s name printed on an official document that had the means of actually paying for something. Today it doesn’t offer quite as much excitement, but is nonetheless an essential step to making your business legit and providing it financial viability.

You have many options; most banks, even small ones, offer business checking. Find free accounts—almost every bank offers one. Don’t get caught up in the duplicate check copies for a fee and the printed statements—the more electronic your business becomes the more efficient you’ll find yourself. The key is to get a checking account with a major bank that offers the ability to assign multiple employees different credit or debit cards. This allows you to let others in your business make deposits and handle other things you may not always have time for. One word of caution, though—make sure those whom you provide access, even depository access, are thoroughly trust-worthy!

Most banks today offer online banking as well, but only some offer online payroll. I use Bank of America and use their features, which they are constantly adding to, to the max.

1.1. Requirements to Open a Business Checking Account

To open your business checking account, you need: Two forms of photographic personal identification, a statement of incorporation (articles of incorporation, for instance), your Employee Identification Number (EIN) or DBA (Doing Business As) statement if you’re using your personal Social Security number, and documentation showing you have a business license as well as the ability to use the business name you selected. Also, if others can sign on the account, be sure you bring them with you to the bank to sign the signature card. (Yes most banks still use this antiquated method!)

As a quick note, with regard to your articles of incorporation, make sure you bring the ones that you received back from the state—the set that has been stamped with your state’s approval. The bank will need the “official” articles to open a business checking account when using this method. If you use a DBA statement and incorporate at a later date, your bank of choice will be able to switch the account records to reflect your business’s status, so you don’t have to worry that you will lose your account should you legally restructure your business at a later date.

1.2. Fictitious Name Statements and Banking

Many new business owners ask me why the bank harassed them over not having their Doing Business As (DBA) or fictitious name statement (FNS) completed yet. Banks need proof that you are allowed to operate under the new business name.

A fictitious business name statement provides this legitimacy. Take it with you to the bank. With a fictitious business name statement, you can take it to the bank and then get the ability to cash checks with your DBA name.

Unless you are operating your business under your own name or have completed the steps to be a corporation (incorporated), LLC, Limited Liability Partnership (LLP), etc., you will be required by your state or county to apply for a DBA.

This legitimizes your business and establishes that you are doing business as (get it? DBA?) XYZ Company.

In most situations that I am aware of, a DBA is as simple as completing the DBA form within 3 0 days of completing your first transaction and following through on each county’s rules with regard to publication, although I always advise you do so prior to conducting business. Completing this step will allow you to establish a business checking account prior to “opening your doors.” Most states also require that you notify the public of your newly established business by posting an announcement in local newspapers and then submitting proof of publication to the state.

To learn more about your state’s requirements, check your state’s official website and search for “DBA.”

1.3. “Doing Business As” (DBA)

If you are doing business as another name, you will need your proof of the DBA to opening a business checking account. For instance, one of my businesses is my own name and Social Security number, doing business as … my company name. Many sole proprietors do business this way, particularly in the beginning.

It is an important side note that if you are using a DBA (which includes, by the way, your previously used names if, for instance, you are recently married and want to be able to cash checks made out to you, your previous name, or your business’s name) you need to bring proof of this.

1.4. Best Banking Deals

Seek out the best deal; compare checking accounts. Here are some things to look for:

- Fees (initial and recurring)

- Minimum balance requirements

- Automatic credit cards

- Overdraft options

- Number of ATMs

- Nonbank ATM fees

- Ability to manage the account online

- Ability to get debit and credit cards in others’ names (with set limits, or deposit-only cards)

- Fraud responsibility—if your card is stolen, how does the bank handle it?

- Maximum number of checks you can write in a month (many still have limits!)

- Miscellaneous fees, like if a client bounces a check on you

- Merchant service capabilities, specifically those that integrate with your website

- Online banking tools

- Online payroll

- Downloadable information into QuickBooks or Quicken

If a bank meets your minimum needs, it’s time to sign up! Expect an hour or so at the bank. I recommend asking for a business line of credit at the same time, and even walking away if they say “no” to your request. Usually they will want the new account badly enough to offer you something.

2. Merchant Accounts

A merchant account is a bank account set up with a payment processor to allow for the acceptance of credit card payments. Most banks offer this service, although keep in mind that it is a fee service. This means that you pay for the transactions the bank processes for you. Going through your local bank will often result in your having a physical credit card terminal, which is great if you have a brick-and-mortar establishment or are willing to enter credit card information each time you accept an order.

There are also merchant account providers online, the most notable being PayPal. In my opinion, PayPal is really a strong choice today. The fees are minimal (they can afford to keep fees low due to the amount of customers they have and the streamlined process between PayPal and eBay) and through their service you can accept PayPal transfers, credit card transactions, and online checks. They handle everything, literally, even protecting you in the event of fraud or declined charges, just as they protect you as a consumer of goods and services online.

Visit PayPal.com, and go to “Business—Merchant Services” for more information on available services, fees, etc.

2.1. Choosing a Merchant Vendor

Chances are your bank will offer merchant services, but they may not offer the best deal on them. You can use one bank for your checking and another for merchant services, but you may not get a fee advantage by doing this. One reason I recommend inquiring about this before you sign up for checking is so you can compare the banks you’re evaluating.

What should you look for when evaluating a merchant account vendor? Start with this list:

- Transaction fees

- Ability to handle a virtual terminal (see the rest of this section for more information)

- Online website integration for credit card processing

- Security

- Protection in case card numbers are stolen

- Reporting to you in case security is breached

- Monthly routine costs and any associated “maintenance fees”

- Integration with American Express or Discover, should you wish to accept them now or in the future

- Dispute resolution practices—Do they automatically side with the consumer? With you? It isn’t unusual for the burden of proof to be on the business, even though the merchant might say it’s the consumer’s burden.

2.2. Online Integration

Be sure your merchant account has online integration. For instance, you want to be able to hand your web developer the plug-ins for handling transactions online in any form, whether through Google Checkout or your own website.

2.3. Web Transactions for Credit Cards

Most merchant services offer you the ability to run a credit card through a virtual terminal. You will want this capability if you take phone orders. Much like with an old credit card machine, you go to a website, type in the payer’s credit card information, the last three digits on the back of their card, and their billing address. This charges the buyer and deposits the money into the account that you have linked to that service, which will most likely be your business checking account.

3. Alternative Payment Options

In today’s Internet environment, you have more than traditional merchant accounts available to you. Numerous online sources offer systems that allow your consumers to pay for items online. Versions 1-4 of my primary website at www. drdaniellebabb.com offered nothing more than PayPal as a payment option, using their shopping cart. Not knowing how this was affecting sales, my www. teachonlinetraining.com site offers integrated merchant services, and my new version of www.drdaniellebabb.com next year will offer credit card payments without the use of PayPal, too. This is discussed more in a few paragraphs.

3.1. Google Checkout

Google Checkout provides a fully complementary merchant service that is directly linked to your website. It is literally as simple as a customer shops on your site and “checks out” through Google Checkout. If you advertise through Google, Google Checkout is provided to you free of charge. Companies like Linens-N-Things and Aeropostale are even starting to use Google Checkout within their websites.

Some additional benefits of Google Checkout, according to their website (which you can check out at checkout.google.com):

Guaranteed Payment: Checkout’s Payment Guarantee protects 98 percent of Checkout orders on average—when an order is guaranteed, you get paid even if it results in a chargeback.

Free Protection: While merchants are typically charged for fraud protection services, Google’s comprehensive protection is free.

Lower Fraud Costs: Checkout’s fraud detection systems reduce fraud and manual review costs by proactively filtering out fraudulent orders.

More Sales: The same systems also help increase sales by identifying legitimate orders that you might otherwise mark as fraudulent.

Fair Treatment: Unlike other services that immediately deduct funds from you for “chargebacks,” Google does so only after a decision has been made as to who is at fault. (Note that a chargeback is when a customer files a dispute and wants their money back because they feel as though you haven’t satisfactorily completed the transaction. Also note that some customers do this as a form of fraud, so you need a helpful, reputable merchant that will handle these types of situations.) (Google, 2008)

3.2. PayPal

Getting its start as the primary payment option for eBay and then later becoming an eBay-owned business, PayPal has been and remains sufficient for many business owners. Of course, PayPal payments must be initiated by those with PayPal accounts, possibly turning many users off or creating too much of a hassle for some buyers. However, it does have basic invoicing capabilities, the ability to transfer funds to accounts and easily handle payments from any source (including checking accounts), and provides security and low fees—as well as cash back when you use it as a credit card.

In summary, PayPal’s website notes that they offer five ways to get paid online: Website Payment Standard, Website Payment Pro, E-mail Payments, Express Checkout, and eBay Payments.

Website Payment Standard is the most basic service that you can sign up for, allowing you to accept credit card payments quickly and easily. There is no application process, no fancy programming that you will have to do to include it on your website. PayPal will provide you with simple HTML code “buttons” that you can use throughout your site, allowing your customers to “Buy Now,” “Add to Cart,” and “Donate.” All that is required to use this option is a PayPal account.

Website Payment Pro is a highly upgraded version of Website Payment Standard— so much so that you will need to either have a fairly thorough understanding of web programming or the ability to hire a website developer. As the criteria and standards are fairly involved, visit PayPal.com for more information. You will find the option for Website Payment Pro under the main “Business” tab.

E-mail Payments is a highly efficient and simple way of invoicing your customers. This option is geared more toward invoicing a client for services than a customer for a product, which is better accomplished through live or real time payment acceptance. With E-mail Payments, you enter the e-mail address of your client, the amount that you are invoicing, and the reason for the invoice, and click “send invoice.” Your client receives the invoice in his or her e-mail inbox, with a direct link to PayPal to make the payment. The only requirements of you and your client is that you both have active PayPal accounts. This is an issue for some business owners who find that their clients want to use a credit card without PayPal. If your client does not have an account, he or she will be prompted to sign up for one, which is both free and quick.

Express Checkout is a system that integrates your customer’s PayPal account information with your website. If your customers are PayPal customers, they can login to Express Checkout with their username and password, auto filling out all billing and shipping information. They can of course alter the shipping and billing information should they need to. This option is quick and simple for both you and your customers. Remember, keeping your customers’ experience simple is one way to keep them happy, which means they will likely return!

eBay Payments is a fantastic option for anyone who is setting up an eBay Store or who will simply be conducting many auctions. With eBay Payments, you will be able to accept PayPal as your primary payment method, with automatic PayPal logo insertion in your auctions or store.

3.3. Other Available Systems

There are other competing systems with PayPal and Google payment options that are purely online. Two of the leading companies, along with a notation about each, are as follows:

Authorize.net. Authorize.net is a simple service provider that will allow you to accept credit card payments online, on your web-enabled mobile device (like your BlackBerry), through mail order and telephone sales, and even within a retail establishment (meaning you can utilize their services even if you run a traditional brick-and-mortar establishment). This is the company that I use on my teachonlinetraining.com website that has easy integration with lots of tools.

MerchantExpress.com. Merchant Accounts Express has been providing online merchant services since 1998, and like the others that I have already mentioned, offers both quick and easy solutions for accepting credit card payments online. Merchant Accounts Express also handles physical acceptance of credit cards with point-of-sale (POS) terminals and service using an online card processing system as well.

As a reminder, fees and services for merchant accounts vary. Feel free to shop around and weigh all available options before signing up!

4. Handling Payroll

Payroll is daunting to many business owners; in fact, it is a top reason that entrepreneurs prefer to use contractors rather than hiring employees. As a business owner, you have to be careful not to cross IRS lines with regard to who is a contractor and who is an employee, and equally important, when a contractor really becomes an employee based on job requirements.

There are many tools out there today, thankfully, to help you with payroll. Automatic Data Processing Inc., or ADP, is known for their payroll and human resources services, and offer many options for small businesses all the way up to Fortune 500 corporations. From preemployment services (background checks, substance abuse testing, identification, etc.) to time and labor management to payroll services, 401(k) services, and benefits administration, ADP is truly a one-stop shop for all of your businesses management and operational needs.

To find out more about what ADP has to offer, visit www.ADP.com or call 1-800-Call-ADP.

Intuit, the same company that brought you QuickBooks, also offers payroll services. Visit Payroll.Intuit.com for more information.

There are other options, too, for online payroll services to help you handle this requirement with ease. Most banks will allow you to process payroll through your online business account. For example, my Bank of America online login allows me to pay employees directly from the home page, set up routine payments (including taxes), handle withholdings, and so on.

When you hire employees, you have to have them fill out different paperwork. An employee fills out a W4 for withholding, and then a state withholding form, which varies by state. You can find your state’s withholding form at www.irs.gov/ formspubs.

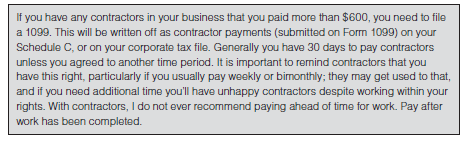

4.1. Contractor Payments

If you are paying a contractor, the rules are easier and the hassles lessen. You simply get an invoice from the contractor; be sure you have his or her Social Security number and current address on file, and submit a 1099-MISC form at the end of the year. The box for nonemployee compensation is what you complete for payments to contractors. Contractors are required to pay their own taxes, relieving you of the burden of calculating withholdings and sending W2s at the end of the year. Several online companies make 1099 submissions easier.

A couple of the most notable ones are FileTaxes.com and eFileForBusiness.com, both offering online completing and filing of the 1099 (and even W2 forms) at very reasonable rates—a couple of bucks per form.

4.2. Employee Payments

How and when you pay employees is based on your employment contract. When you hire employees, you will provide them with information on when and how you will pay them, if you offer direct deposit, and so on. One reason I recommend using an online company is that they handle direct deposits, withholdings, and employee payments all for you, with easy-to-read reports and simple end-of-year reporting.

When you make a payment to an employee, you can select when and how—and you can change whether you offer direct deposit and when you pay, but you must provide adequate notice of any changes. A few of my employers, for instance, have changed from every-two-weeks to bimonthly pay schedules. Give your employees enough time to plan on their end. You can begin or end direct deposit at any time, too. If you are writing manual checks and you aren’t going to be in town on pay day, be sure you have a plan to handle this. You are now responsible for your employees.

4.3. Automated Online Payments

You can automatically pay your employees or contractors online. For some of my contractors, I use transfers initiated in Bank of America’s transfer system. This allows the contractor to receive payment same-day (sometimes same-hour) with near-immediate clearance of funds. You can also use services to pay based on a specific time period. You really should do what is easiest and best for you, and make it clear to employees that anything you do electronically is a bonus to them—it is not a requirement of any sort.

4.4. Handling Taxes for Employees

Taxes for employees aren’t fun—from paying them to filing them. As a business owner, you are responsible for withholding payroll taxes, including:

- Social Security at 12.4 percent (6.2 percent split employer/employee)

- Medicare at 2.9 percent (1.45 percent split employer/employee)

- Federal withholdings (dependent on completed W4)

- State withholdings (dependent on completed W4)

- Any employee-paid costs for healthcare (varies by plan and other factors)

- Any pretax offerings, such as a flexible spending account (FSA) or health spending account (HSA) (varies)

So what do you do with the federal and state withholding money? In short, you are paying the money to the IRS under the employee’s name.

As you can imagine, these matters are highly sensitive and legally binding—if you mess up, you’re going to have to pay! As I am no tax expert and will never claim to be, it is my most sincere advice that you contract with a payroll service, either a local or national firm, such as ADP, to handle this aspect of your business. The last thing you need to worry about is the IRS coming after you for not dotting your Is or crossing your Ts.

Remember that you have to offer employees the ability to adjust their withholdings. How they calculate their numbers isn’t your call—they can withhold (or not) as much or as little as they want. The tax burden at the end of the year is their responsibility, provided you withheld the amount that they asked you to (which you are legally obligated to do).

Many business owners also ask about overtime. You do not need to pay a salaried employee overtime, as long as certain common criteria are met. These issues do vary by state, field of work, etc. EmployeeIssues.com provides a detailed yet succinct explanation of the complications with overtime. You can view their full explanation at www.EmployeeIssues.com/overtime_pay.

The basic explanation is that one workweek consists of 7 consecutive 24-hour days. Overtime is monetary compensation for all hours worked in one workweek above 40 hours. The current overtime wage is 1.5 times the normal hourly rate, which is what you would pay for all hours worked above 40. For example, if the hourly wage of an employee is $20, the overtime rate would be $30 per hour.

EmployeeIssues.com notes that, “Employers may pay eligible employees by some other method than hourly, such as by piecework or annual salary. But in any case, employers must still calculate overtime pay based on the hours eligible employees work per workweek.”

Here are the general criteria regarding overtime, again according to EmployeeIssues.com:

“Overtime pay is due on the regularly-scheduled paydays for which employees earned it. For example, if an employer pays regular wages every Friday, then every Friday the overtime pay employees earned in the same workweek is also due and payable.

“Non-management, ‘blue-collar’ hourly, and salaried employees who perform manual labor for the types of organizations listed below are eligible for overtime pay. ‘White-collar’ hourly and salaried employees who work for the types of organizations listed below and earn less than $455 weekly (or less than $910 biweekly or $1971.66 monthly) are also broadly eligible.”

- Any engaged in interstate commerce

- Any that gross $500,000 or more annually

- Federal, state, and local government agencies

- Hospitals and other institutions engaged in the care of sick, aged, or mentally ill people

- Educational institutions

EmployeeIssues.com also notes that job titles have no relevance when determining eligibility for overtime pay. Overtime eligibility is determined based on “occupations, wages or salaries, and job duties,” although they note that exceptions may apply.

Breaking down the overtime law even further, the information on EmployeeIssues.com continues with the definition of those who are exempt from overtime pay—those employees who do not receive overtime pay. They state that:

“Generally, employers may classify the following types of employees as exempt from (not eligible for) overtime pay:

- White-collar executive, administrative, and professional employees who earn more than $455 per week and regularly exercise discretion and independent judgment with respect to matters of significance.

- Employees who earn $100,000 or more per year, and also customarily and regularly perform any one or more of the exempt duties or responsibilities of executive, administrative, or professional employees.

- Certain computer professionals who earn more than $455 in weekly salaries or $27.63 in hourly wages, depending on their specific job duties.” (EmployeeIssues.com, 2008)

Now of course, the list of variables that are taken into account with regard to who is and who is not eligible for overtime is long, and gets longer with each passing revision of the tax code. The information provided above by EmployeeIssues.com is a general overview of the federal tax laws that relate to overtime issues. Please note that state laws may vary from those listed above and may supersede federal tax law, as well. When in doubt, consult with financial or legal counsel for additional information and guidance.

4.5. Social Security Taxes

The Social Security Administration splits up who pays what between the employer and employee. Each party pays 50 percent of the total percentage noted in the withholding list above (12.4). The current cap for Social Security withholdings is $97,500 annually, according to the Social Security Administration’s website. If you are considered “self employed,” you are required to pay the full amount, as you are both the employer and employee. (Social Security Administration, 2008)

Social Security taxes, while currently paying for those withdrawing the money, were designed to be used to ensure that each individual, upon retirement, would have some income and not be left without money when they’re unable to work.

In recent times, due to lack of money in the Social Security coffer and the ability of many of us to invest better than the government does, some people have called for employees to have a choice as to whether to invest in higher-yield funds or traditional Social Security benefits, while still paying into the system for those who will need it soon.

4.6. Bill Pay Services

Bill pay services are yet another aspect of business checking and payroll services. Many of us use bill pay services, like Bank of America’s “e-bill” service, to pay everything from utilities to credit card bills. But businesses have the same options to pay their bills online. Be careful of companies now putting corporate credit cards into “corp accounts” that must be paid instead of the credit card company (I recently ran into an issue here myself). You should use a banking organization that allows you to set up bill pay, and not just if your company accepts electronic payments but also if it requires mailed cashier’s checks. Let the bank handle all of this. Since most online banking systems don’t show you pending payments in your balances, I always recommend using a secondary system that also allows you to categorize payments for tax purposes and for expenditure tracking and allocation.

5. Financial Management

Everything we have talked about so far rolls up under the umbrella of financial management. You will need to manage all aspects of your finances, and you need to plan for the costs of each.

5.1. Payroll Taxes

We already noted that having employees is costly. If you create a business plan that doesn’t assume you will have employees in year two and then you need them, revise your plan to include the new costs you will incur as a result of this decision; for instance, the cost of training your new employee(s), the cost of payroll services, uniform costs (as applicable), additional taxes that you as the employer must pay (Social Security, Medicare, etc.), and additional insurance costs (workers’ compensation, etc.). More information on this is available in Chapter 7 as well.

Some business owners worry that as employees change their withholdings, it will impact their bottom line. It won’t, because you either pay the government or the employee. There is no need to make adjustments based on withholding changes.

5.2. Budgeting

It seems daunting to think of everything you need to budget for your business. One thing you can do is ask other business owners what they didn’t budget for that they learned later was a mistake—particularly the most costly ones. Of course, not all of these will apply to your business.

Some items to budget for that you may not have thought about:

- Bonuses for jobs that are above and beyond the call of duty

- Overtime

- Unforeseen office supplies (like water, or whatever you want to offer at your office)

- Healthcare

- Sick time

- Temporary workers

- Gifts (birthdays, holidays)

- Specialized training or certifications (notary training, etc.)

- Additional technology (more computers, printers, etc.)

- Additional space

- Uniforms

5.3. Corporate and Sole Proprietor Taxes

Regardless of what your business is created as (sole proprietorship, partnership, LLC, etc.), you will have to file business taxes from its inception. Be sure that you note the actual date you started business, because all costs are prorated in year one based on how many days you were in business that year.

Sole proprietors use what is called pass-through income; the income is noted on a Schedule C and passed through to the individual. Sole proprietors still take all business deductions—including depreciation, and so on—in their business, just like corporations do. Some note that the taxes can be higher because personal income tax is higher than most corporate tax, depending on the income of the business. Sole proprietors usually only need to file once per year on their annual tax return, depending on annual profit or income, though many scenarios may make it necessary to file quarterly—many sole proprietors file quarterly no matter what. Ask your tax authority on whether you need to file yearly or more often.

Corporations file corporate tax returns, often at a lower tax rate than those who file as self employed (sole proprietors). As there are many variations of legal structure, each with their own set of determinant factors with regard to taxability, consult with a tax attorney for more information on the tax implications of each.

5.4. Insurance

Last but not least of your cost and budget requirements is insurance; everything from employee insurance you provide to business insurance to disability insurance for yourself.

I recommend asking a lawyer and an insurance specialist what is necessary for a business owner. Personally, I have umbrella insurance (it covers all of my properties), I require anyone driving my cars for business to have personal insurance (something you should always do), liability insurance (how much depends on what you do and your risk level), and disability insurance for yourself should you get sick.

Some other common insurance plans include:

- Property insurance—protection for your property from damage/loss.

- Legal liability—product and general.

- Workers’ Compensation—protection in case of an on-the-job accident.

- Key person loss—especially important for the small business with one or two “key” individuals, without whom would cease to exist or suffer a large loss to business.

- Business interruption—this policy pays the business, should something occur that prevents the business from operating.

- E-commerce insurance—this is a more recent trend. This policy protects the business should it suffer a great loss of its Internet presence due to hackers or other problems.

Source: Babb Danielle (2009), The Accidental Startup: How to Realize Your True Potential by Becoming Your Own Boss. Alpha.

I’m very happy to read this. This is the kind of manual that needs to be given and not the random misinformation that is at the other blogs. Appreciate your sharing this best doc.