You can’t develop a consistent international financial policy until you understand the reasons for the differences in exchange rates and interest rates. We consider the following four problems:

- Problem 1. Why is the dollar rate of interest different from, say, the rate on Ruritanian pesos (RUPs)?

- Problem 2. Why is the forward rate of exchange for the peso different from the spot rate?

- Problem 3. What determines next year’s expected spot rate of exchange between dollars and pesos?

- Problem 4. What is the relationship between the inflation rate in the United States and the inflation rate in Ruritania?

Suppose that individuals were not worried about risk and that there were no barriers or costs to international trade on capital flows. In that case, the spot exchange rates, forward exchange rates, interest rates, and inflation rates would stand in the following simple relationship to one another:

Why should this be so?

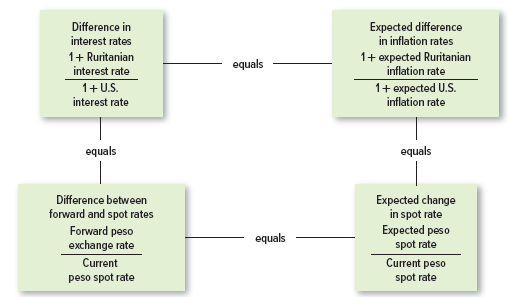

1. Interest Rates and Exchange Rates

Suppose that you have $1,000 to invest for one year. U.S. dollar deposits are offering an interest rate of 5%; Ruritanian peso deposits are offering (an attractive?) 15.5%. Where should you put your money? Does the answer sound obvious? Let’s check:

- Dollar loan. The rate of interest on one-year dollar deposits is 5%. Therefore, at the end of the year you get 1,000 X 1.05 = USD1,050.

- Peso loan. The current exchange rate is RUP50/USD1. Therefore, for $1,000, you can buy 1,000 X 50 = RUP50,000. The rate of interest on a one-year peso deposit is 15.5%. Therefore, at the end of the year you get 50,000 X 1.155 = RUP57,750. Of course, you don’t know what the exchange rate is going to be in one year’s time. But that doesn’t matter. You can fix today the price at which you sell your pesos. The one-year forward rate is RUP55/USD1. Therefore, by selling forward, you can make sure that you will receive 57,750/55 = $1,050 at the end of the year.

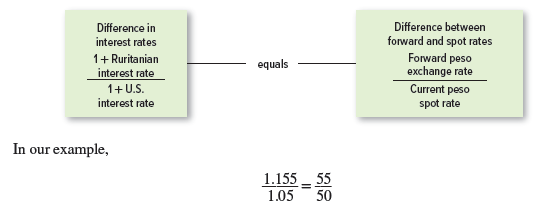

Thus, the two investments offer the same rate of return. They have to—they are both risk-free. If the domestic interest rate were different from the covered foreign interest rate, you would have a money machine.

When you make the peso loan, you receive a higher interest rate. But you get an offsetting loss because you sell pesos forward at a lower price than you pay for them today. The interest rate differential is

And the differential between the forward and spot exchange rates is

![]()

Interest rate parity theory says that the difference in interest rates must equal the difference between the forward and spot exchange rates:

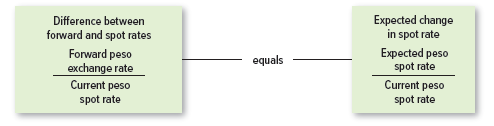

2. The Forward Premium and Changes in Spot Rates

Now let’s consider how the forward premium is related to changes in spot rates of exchange. If people didn’t care about risk, the forward rate of exchange would depend solely on what people expected the spot rate to be. For example, if the one-year forward rate on pesos is RUP55/USD1, that could only be because traders expect the spot rate in one year’s time to be RUP55/USD1. If they expected it to be, say, RUP60/USD1, nobody would be willing to buy pesos forward. They could get more pesos for their dollar by waiting and buying spot.

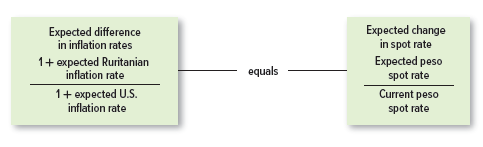

Therefore the expectations theory of exchange rates tells us that the percentage difference between the forward exchange rate and today’s spot rate is equal to the expected change in the spot rate:

Of course, this assumes that traders don’t care about risk. If they do care, the forward rate can be either higher or lower than the expected spot rate. For example, suppose that you have contracted to receive one million pesos in three months. You can wait until you receive the money before you change it into dollars, but this leaves you open to the risk that the price of the peso may fall over the next three months. Your alternative is to sell the peso forward. In this case, you are fixing today the price at which you will sell your pesos. Since you avoid risk by selling forward, you may be willing to do so even if the forward price of pesos is a little lower than the expected spot price.

Other companies may be in the opposite position. They may have contracted to pay out pesos in three months. They can wait until the end of the three months and then buy pesos, but this leaves them open to the risk that the price of the peso may rise. It is safer for these companies to fix the price today by buying pesos forward. These companies may, therefore, be willing to buy forward even if the forward price of the peso is a little higher than the expected spot price.

Thus, some companies find it safer to sell the peso forward, while others find it safer to buy the peso forward. When the first group predominates, the forward price of pesos is likely to be less than the expected spot price. When the second group predominates, the forward price is likely to be greater than the expected spot price. On average you would expect the forward price to underestimate the expected spot price just about as often as it overestimates it.

3. Changes in the Exchange Rate and Inflation Rates

Now we come to the third side of our quadrilateral—the relationship between changes in the spot exchange rate and inflation rates. Suppose that you notice that silver can be bought in Ruritania for 1,000 pesos a troy ounce and sold in the United States for $30.00. You think you may be on to a good thing. You take $20,000 and exchange it for $20,000 X RUP50/USD1 = 1,000,000 pesos. That’s enough to buy 1,000 ounces of silver. You put this silver on the first plane to the United States, where you sell it for $30,000. You have made a gross profit of $10,000. Of course, you have to pay transportation and insurance costs out of this, but there should still be something left over for you.

Money machines don’t exist—not for long, anyway. As others notice the disparity between the price of silver in Ruritania and the price in the United States, the price will be forced up in Ruritania and down in the United States until the profit opportunity disappears. Arbitrage ensures that the dollar price of silver is about the same in the two countries. Of course, silver is a standard and easily transportable commodity, but the same forces should act to equalize the domestic and foreign prices of other goods. Those goods that can be bought more cheaply abroad will be imported, and that will force down the price of domestic products. Similarly, those goods that can be bought more cheaply in the United States will be exported, and that will force down the price of the foreign products.

This is often called purchasing power parity? Just as the price of goods in Walmart stores must be roughly the same as the price of goods in Target, so the price of goods in Ruritania when converted into dollars must be roughly the same as the price in the United States:

Purchasing power parity implies that any differences in the rates of inflation will be offset by a change in the exchange rate. For example, if prices are rising by 1.0% in the United States and by 11.1% in Ruritania, the number of pesos that you can buy for $1 must rise by 1.111/1.01 – 1, or 10%. Therefore purchasing power parity says that to estimate changes in the spot rate of exchange, you need to estimate differences in inflation rates:[1] [2]

In our example,

Current spot rate x expected difference in inflation rates = expected spot rate

![]()

4. Interest Rates and Inflation Rates

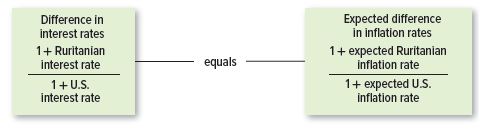

Now for the fourth leg! Just as water always flows downhill, so capital tends to flow where returns are greatest. But investors are not interested in nominal returns; they care about what their money will buy. So, if investors notice that real interest rates are higher in Ruritania than in the United States, they will shift their savings into Ruritania until the expected real returns are the same in the two countries. If the expected real interest rates are equal, then the difference in nominal interest rates must be equal to the difference in the expected inflation rates:[3]

Difference in interest rates 1 + Ruritanian interest rate

In Ruritania the real one-year interest rate is 4%:

In the United States it is also 4%:

5. Is Life Really That Simple?

We have described four theories that link interest rates, forward rates, spot exchange rates, and inflation rates. Of course, such simple economic theories are not going to provide an exact description of reality. We need to know how well they predict actual behavior. Let’s check.

- Interest Rate Parity Theory Interest rate parity theory says that the peso rate of interest covered for exchange risk should be the same as the dollar rate. Before the financial crisis of 2007-2009, interest rate parity almost always held, provided money could be moved easily between deposits in the different currencies. In fact, dealers would set the forward price of pesos by looking at the difference between the interest rates on deposits of dollars and pesos. However, during the financial crisis this relationship broke down. Du, Tepper and Verdahlan provide evidence that the relationship was persistently violated for some time following 2009 among

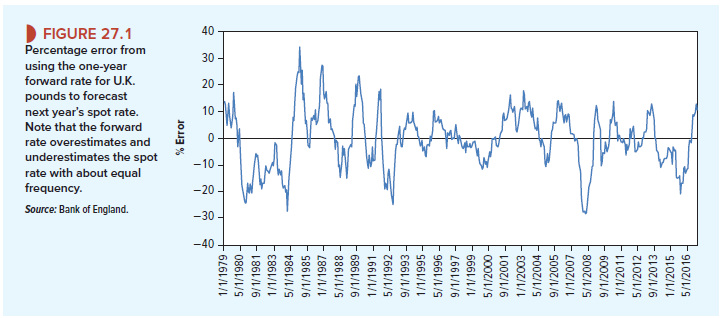

the major currencies. They argue that this persistence was partly due to new leverage restrictions on banks, which increased arbitrage costs and caused them to shy away from such activity.[4] [5] - The Expectations Theory of Forward Rates How well does the expectations theory explain the level of forward rates? Scholars who have studied exchange rates have found that forward rates typically exaggerate the likely change in the spot rate. When the forward rate appears to predict a sharp rise in the spot rate (a forward premium), the forward rate tends to overestimate the rise in the spot rate. Conversely, when the forward rate appears to predict a fall in the currency (a forward discount), it tends to overestimate this fall.11

This finding is not consistent with the expectations theory. Instead it looks as if sometimes companies are prepared to give up return to buy forward currency and other times they are prepared to give up return to sell forward currency. In other words, forward rates seem to contain a risk premium, but the sign of this premium swings backward and forward.[6] You can see this from Figure 27.1. Almost half the time the forward rate for the U.K. pound overstates the likely future spot rate and half the time it understates the likely spot rate. On average, the forward rate and future spot rate are almost identical. This is important news for the financial manager; it means that a company that always uses the forward market to protect against exchange rate movements does not pay any extra for this insurance.

That’s the good news. The bad news is that the forward rate is a fairly awful forecaster of the spot rate. For example, in Figure 27.1 the large error in 1985 reflects the total failure of the forward rate to anticipate the 34% rise in the value of sterling.

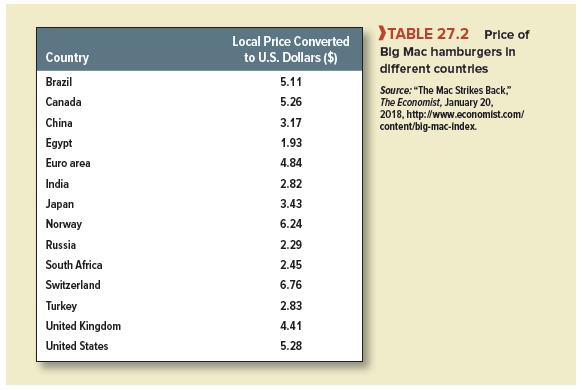

- Purchasing Power Parity Theory What about the third side of our quadrilateral— purchasing power parity theory? No one who has compared prices in foreign stores with prices at home really believes that prices are the same throughout the world. Look, for example, at Table 27.2, which shows the price of a Big Mac in different countries. Notice that at current rates of exchange a Big Mac costs $6.76 in Switzerland but only $5.28 in the United States. To equalize prices in the two countries, the number of Swiss francs that you could buy for your dollar would need to increase by 6.76/5.28 – 1 = .28, or 28%.

This suggests a possible way to make a quick buck. Why don’t you buy a hamburger to-go in (say) Egypt for the equivalent of $1.93 and take it for resale in Switzerland, where the price in dollars is $6.76? The answer, of course, is that the gain would not cover the costs. The same good can be sold for different prices in different countries because transportation is costly and inconvenient.[7]

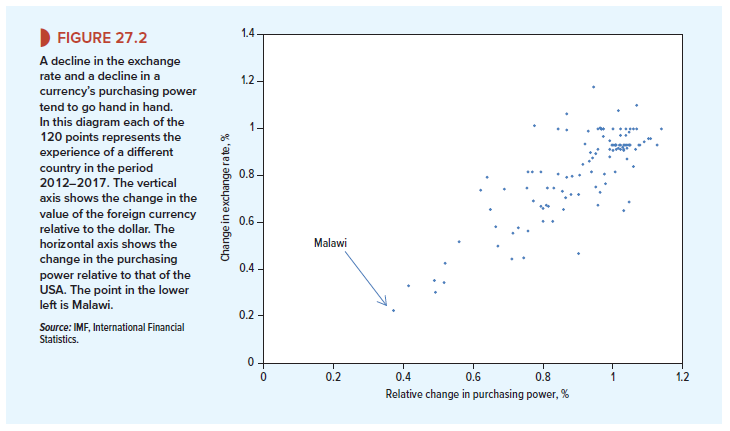

On the other hand, there is clearly some relationship between inflation and changes in exchange rates. For example, between 2012 and 2017 prices in Malawi rose by 270% relative to prices in the United States. Or, to put it another way, you could say that the relative purchasing power of money in Malawi declined by almost two-thirds. If exchange rates had not adjusted, exporters in Malawi would have found it impossible to sell their goods. But, of course, exchange rates did adjust. In fact, the value of the Malawian kwacha fell by 78% relative to the U.S. dollar.

In Figure 27.2, we have plotted the relative change in purchasing power for a sample of countries against the change in the exchange rate. Malawi is tucked in the bottom left-hand corner. You can see that although the relationship is far from exact, large differences in inflation rates are generally accompanied by an offsetting change in the exchange rate.[8]

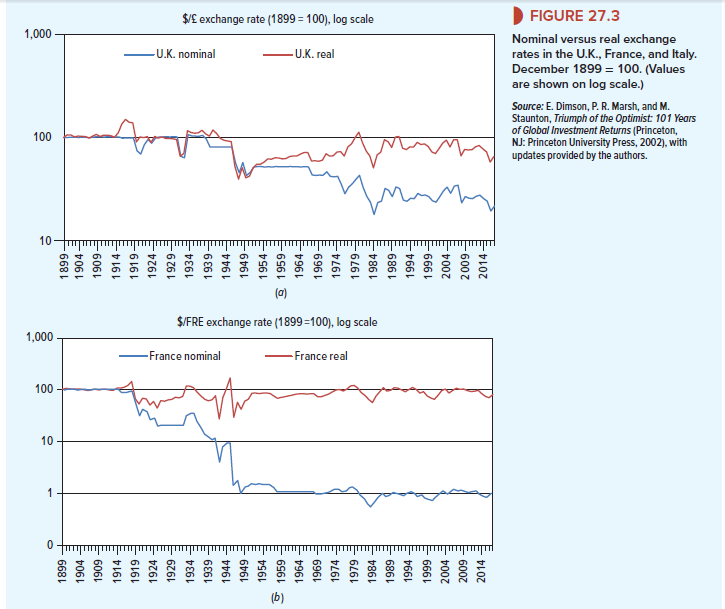

Strictly speaking, purchasing power parity theory implies that the differential inflation rate is always identical to the change in the spot rate. But we don’t need to go as far as that. We should be content if the expected difference in the inflation rates equals the expected change in the spot rate. That’s all we wrote on the third side of our quadrilateral. Look, for example, at Figure 27.3. The blue line in the first plot shows that in 2014 £1 sterling bought only 32% of the dollars that it did at the start of the twentieth century. But this decline in the value of sterling was largely matched by the higher inflation rate in the U.K. The red line shows that the inflation-adjusted, or real, exchange rate ended the century at roughly the same level as it began.[9] The second and third plots show the experiences of France and Italy, respectively. The fall in nominal exchange rates for both countries is much greater. Adjusting for changes in currency units, the equivalent of one French franc in 2014 bought about 1% of the dollars that it did at the start of 1900. The equivalent of one Italian lira bought about .4% of the number of dollars. In both cases the real exchange rates in 2014 are not much different from those at the beginning of the twentieth century. Of course, real exchange rates do change, sometimes quite sharply. For example, the real value of sterling fell by 13% in two weeks following the Brexit vote in 2017. However, if you were a financial manager called on to make a long-term forecast of the exchange rate, you could not have done much better than to assume that changes in the value of the currency would offset the difference in inflation rates.

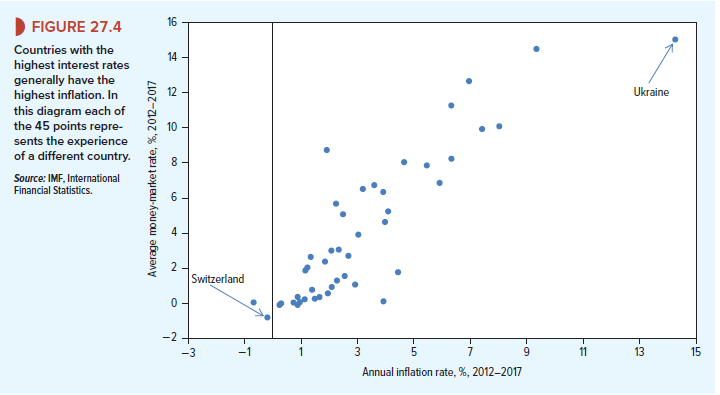

- Equal Real Interest Rates Finally we come to the relationship between interest rates in different countries. Do we have a single world capital market with the same real rate of interest in all countries? Does the difference in money interest rates equal the difference in the expected inflation rates?

This is not an easy question to answer since we cannot observe expected inflation. However, in Figure 27.4, we have plotted the average interest rate in each of 45 countries against the average inflation rate. Switzerland is tucked into the bottom-left corner of the chart, while Ukraine is represented by the dot in the top-right corner. You can see that, in general, the countries with the highest interest rates also had the highest inflation rates. There were much smaller differences between the real rates of interest than between the nominal (or money) rates.

This may be a good point at which to offer a warning: Do not naively borrow in currencies with the lowest interest rates. Those low interest rates may reflect the fact that investors expect inflation to be low and the currency to appreciate. In this case, the gain that you realize from “cheap” borrowing is liable to be offset by the high cost of the currency that is needed to service the loan. Many have learned this lesson the hard way. For example, in recent years over 500,000 Poles were lured by low Swiss interest rates into taking out mortgages in Swiss francs. When the Swiss franc jumped by 23% against the Polish zloty in January 2015, many of those borrowers found themselves in big trouble.

Professional foreign exchange traders may, from time to time, enter into carry trades in which they take on currency risk by borrowing in countries with low interest rates and then use the cash to buy bonds in countries with high interest rates. But wise corporate managers do not speculate in this way; they use foreign currency loans to offset the effect that exchange rate fluctuations have on the company’s business.

Its like you read my thoughts! You appear to know so much approximately this, such as you wrote the e-book in it or something. I believe that you can do with a few to pressure the message house a bit, but other than that, that is wonderful blog. A great read. I will certainly be back.