1. Filing Entry Papers

The entry process requires filing the necessary documents to enable customs to determine whether the merchandise may be released from its custody, as well as for duty assessment and statistical purposes. Both of these processes can be accomplished electronically via the Automatic Broker Interface Program. What are entry documents? Entry documents generally consist of (1) an entry manifest (Form 7533) or application and special permit for immediate delivery (Form 3461); (2) a commercial invoice (or pro forma invoice when the commercial invoice cannot be produced); (3) a bill of lading, air waybill, or other evidence of right to make entry; (4) a packing list, if appropriate; and (5) other documents necessary to determine the admissibility of the merchandise. This may include information to determine whether the imported merchandise bears an infringing trademark. If the goods are to be released from customs on entry documents, an entry summary for consumption must be filed. An entry summary includes the entry package returned that allows for release of merchandise and other forms (Form 7501) (see International Perspective 18.2 for different types of entries).

2. Release of Merchandise and Deposit of Estimated Duty

Once the complete entry is made by filing with customs (i.e., the declared value, classification, and rate of duty applicable to the merchandise, as well as an entry summary for consumption), the product is released by customs and the estimated duty deposited. A bond must be posted before filing the entry summary to guarantee payment of duties or taxes upon the final assessment of duties or other fees by customs (liquidation of entry). Bonds are required for almost all formal entries and may be required for some informal entries and temporary importation under bond entries. There are also bonds covering the activities of warehouse proprietors, carriers, and so on.

If goods are to be released upon entry, an entry summary for consumption must be filed and estimated duties deposited at the port of entry within ten working days of the goods’ entry. Immediate release of a shipment can be obtained through a special permit (Form 3461) prior to arrival of the goods. Carriers participating in the Automated Manifest System can receive conditional release authorizations after leaving the foreign country and up to five days before landing in the United States. Upon approval by CBP, shipments are released expeditiously after arrival of the merchandise. However, entry summary must be filed and estimated duties deposited within ten working days after release. Immediate delivery release is allowed for certain types of goods: articles for a trade fair, shipment consigned to an agency of the U.S. government, tariff quota merchandise (in some cases, merchandise under absolute quota), or merchandise arriving from Canada or Mexico (when approved by bond director and bond is on file). In cases where articles subject to different rates of duty are packed together, the commingled articles shall be subject to the highest rate of duty applicable to any part of the commingled lot. However, the consignee or agent can segregate the merchandise to allow customs agents to ascertain the appropriate duty (within thirty days after notice by customs of such commingling).

A bond is different from a carnet because the latter serves as a customs entry document and as a customs bond. Carnets are ordinarily acceptable without the need for additional security. Institutions that issue carnets or guarantee the payment obligation under carnets must be approved by CBP. In cases where a carnet is not used, a bond is usually required to secure a customs transaction. A single-entry bond application is made by the importer or designated person to secure the entry of a single customs transaction, while a continuous- bond application is made for multiple transactions. Such application is made to the port director. A single-entry bond is generally for the value of the merchandise plus duties, taxes, and fees. Customs bonds (usually 10 percent of the duties, taxes, and fees paid by the importer during the previous thirteen months) are valid until canceled either by the importer or surety. In lieu of a bond, an importer may pledge cash, savings bonds, or Treasury notes. Bonds and /or cash are held until one year after an importation is liquidated (in the case of transportation under bond, the importer demonstrates that the merchandise was either exported or destroyed properly). Customs bonds can be terminated by sending a letter to the port where the bond was originally registered, and the cancellation takes effect ten days after the request is received (sureties are required to send a request to customs and principal, and this takes effect thirty days after receipt).

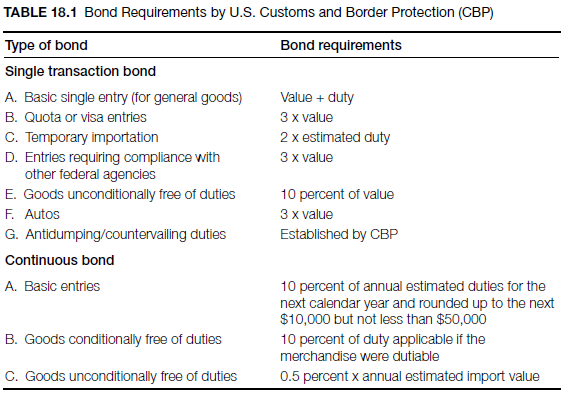

Bonds may be secured through a resident U.S. surety company, through a resident and citizen of the United States, or in the form of cash or other government obligations. The list of corporations authorized to act as sureties on bonds and the limits of their bonds is published by the Treasury Department. If individuals sign as sureties, customs often requires two sureties on a bond to protect the revenue and to ensure compliance with the regulations. There are also other requirements that individuals have to meet to act as sureties: U.S. residency and citizenship, evidence of solvency and financial responsibility, and ownership of property that could be used as security within the limits of the port where the contract of suretyship is approved. The current market value of the property less any debts must be equal to or greater than the amount of the bond. In the event of default by the importer, the surety and importer are liable to pay liquidated damages to customs (Serko, 1985) (Table 18.1).

3. Liquidation, Protests, and Petitions

Liquidation is the final ascertainment of the duties and drawback accruing on an entry by customs. Liquidation is required for all entries of imported merchandise except the following: temporary importation bond entry, transportation in bond, and imports that are subject to immediate exportation. The liquidation procedure involves determination of the value of imports, ascertainment of their classification and applicable rate of duty, and the computation of the final amount of duty to be paid. Customs will then establish whether any additional (excess) duty has to be paid (refunded) to the importer as the case may be and notify the importer, consignee, or agent of the liquidation by posting a public notice. A formal entry is liquidated when an entry appears on the bulletin notice of liquidation posted in customs.

It is also important to note the following:

- Limitation on liquidation: If imported merchandise is not liquidated within one year from the date of entry, it is considered liquidated at the rate and amount of duty stated at the time of entry.

- Voluntary reliquidation by customs: Customs could reliquidate any entry within ninety days from the date of notice of the original liquidation.

- Liquidation for informal, mail, and baggage entries: The effective date of liquidation for such entries is the date of payment of estimated duties upon entry of merchandise or the date of release by customs under free duty or permit for immediate delivery (Ros- sides, 1986).

Conversion of Currency

The date of exportation of the goods is the date used to determine the applicable rate of exchange for customs purposes.

Liquidation is not final until any protest that has been filed against it has been decided. An importer who disagrees with the liquidation of an entry may file a protest in writing within ninety days after the date of notice of liquidation. The protest could be with respect to any one or more of the following: the appraised value of the merchandise, classification, duties and other charges, the exclusion of a product from entry, or the refusal to reliquidate an entry. If a protest is denied by the district director, the importer can appeal to the Court of International Trade. The parties have a right to further appeal to the Court of Appeals for the Federal Circuit and from there to the highest court in the country, the Supreme Court of the United States. An importer can also request a further review of the protest beyond than that provided by the district director. If the protest is denied by the latter, the matter is forwarded for review by the regional commissioner.

Any interested party could file a petition with the secretary of the Treasury if the individual or group believes that the appraised value, classification, or rate of duty for an imported merchandise is not correct. The term interested party includes manufacturers, producers, wholesalers, or trade unions in the United States.

Source: Seyoum Belay (2014), Export-import theory, practices, and procedures, Routledge; 3rd edition.

Thanks for sharing your info. I really appreciate your efforts and I will be waiting

for your further write ups thank you once again.

It is in reality a great and useful piece of information. I am satisfied that you just shared this helpful info with us. Please stay us up to date like this. Thanks for sharing.