Those leading entrepreneurial ventures can also expect to encounter a number of important legal issues when launching and then, at least initially, operating their firm. We discuss a number of these issues next.

1. Choosing an attorney for a Firm

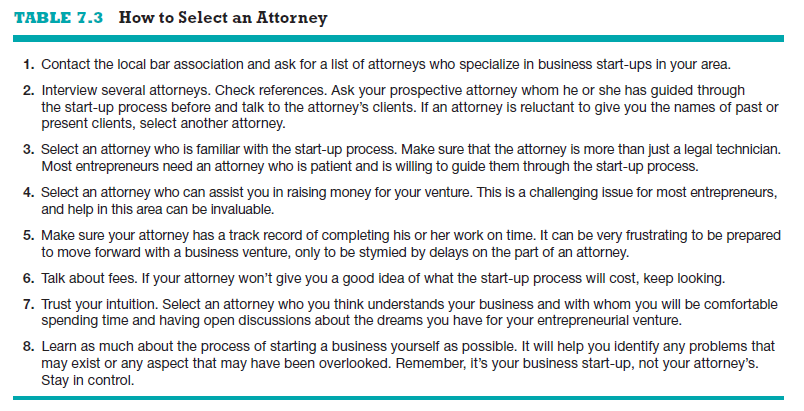

It is important for an entrepreneur to select an attorney as early as possible when developing a business venture. Selecting an attorney was instrumental in helping Tempered Mind, the company profiled in the opening feature, estab- lish a firm legal foundation. Table 7.3 provides guidelines to consider when se- lecting an attorney. It is critically important that the attorney be familiar with start-up issues and that he or she has successfully shepherded entrepreneurs through the start-up process before. It is not wise to select an attorney just because she is a friend or because you were pleased with the way she prepared your will. For issues dealing with intellectual property protection, it is essential to use an attorney who specializes in this field; such as a patent attorney when filing a patent application.9

While hiring an attorney is advisable, it is not the only option available for researching, preparing, and filing the necessary forms to get a business up and running legally. Most business owners can do much of the preliminary work on their own, and they rely on an attorney for guidance and advice. If you’re particularly tight on money and feel as though you can handle por- tions of the legal process on your own (which is not generally recommended but may apply in some cases), there are online companies that can help you with the necessary forms and filings. Examples include LegalZoom (www.le– galzoom.com), Rocket Lawyer (www.rocketlawyer.com), and Nolo (www.nolo. com). All three companies provide a comprehensive menu of legal services for business owners, including the ability to ask a lawyer questions either for free or for a modest fee. It’s a judgment call as to whether to hire a lawyer to do your legal work, utilize a service such as LegalZoom, RocketLawyer, or Nolo, or pursue a blended approach. A blended approach might involve hiring an attorney to obtain legal advice (such as determining your form of business ownership) and then utilizing one of the online services to prepare the documents and file them with the appropriate governmental agencies on your behalf.

2. Drafting a Founders’ agreement

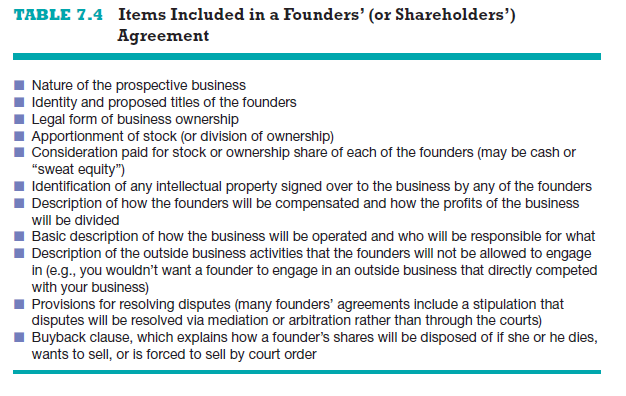

If two or more people start a business, it is important that they have a found- ers’ (or shareholders’) agreement. A founders’ agreement is a written docu- ment that deals with issues such as the relative split of the equity among the founders of the firm, how individual founders will be compensated for the cash or the “sweat equity” they put into the firm, and how long the founders will have to remain with the firm for their shares to fully vest.10

The items typically included in a founders’ agreement are shown in Table 7.4. An important issue addressed by most founders’ agreements is what hap- pens to the equity of a founder if the founder dies or decides to leave the firm. Most founders’ agreements include a buyback clause, which legally obligates departing founders to sell to the remaining founders their interest in the firm if the remaining founders are interested.11 In most cases, the agreement also specifies the formula for computing the dollar value to be paid. The presence of a buyback clause is important for at least two reasons. First, if a founder leaves the firm, the remaining founders may need the shares to offer to a replacement per- son. Second, if founders leave because they are disgruntled, the buyback clause provides the remaining founders a mechanism to keep the shares of the firm in the hands of people who are fully committed to a positive future for the venture.

Vesting ownership in company stock is another topic most founders’ agree- ments address. The idea behind vesting is that when a firm is launched, in- stead of issuing stock outright to the founder or founders, it is distributed over a period of time, typically three to four years, as the founder or founders “earn” the stock. Not only does vesting keep employees motivated and engaged, but it also solves a host of potential problems that can result if employees are given their stock all at once. More on the concept of vesting ownership in company stock is provided in the “Savvy Entrepreneurial Firm” feature.

3. Avoiding legal disputes

Most legal disputes are the result of misunderstandings, sloppiness, or a simple lack of knowledge of the law. Getting bogged down in legal disputes is something that an entrepreneur should work hard to avoid. It is important early in the life of a new business to establish practices and procedures to help avoid legal disputes. Legal snafus, particularly if they are coupled with man- agement mistakes, can be extremely damaging to a new firm.

There are several steps entrepreneurs can take to avoid legal disputes and complications, as discussed next.

Meet all Contractual Obligations It is important to meet all contractual obligations on time. This includes paying vendors, contractors, and employees as agreed and delivering goods or services as promised. If an obligation cannot be met on time, the problem should be communicated to the affected parties as soon as possible. It is irritating for vendors, for example, when they are not paid on time; largely because of the other problems the lack of prompt payments cre- ates. The following comments dealing with construction companies demonstrate this situation: “Not getting paid on time can be devastating to construction companies that have costs to (their) vendors and employees that sometimes re- quire payment weekly. Cash flow problems can send a company into a hole from which they will often not recover.”12 Being forthright with vendors or creditors if an obligation cannot be met and providing the affected party or parties a re- alistic plan for repaying the money is an appropriate path to take and tends to maintain productive relationships between suppliers and vendors.

Avoid undercapitalization If a new business is starved for money, it is much more likely to experience financial problems that will lead to litigation.13

A new business should raise the money it needs to effectively conduct busi- ness or should stem its growth to conserve cash. Many entrepreneurs face a dilemma regarding this issue. Most entrepreneurs have a goal of retaining as much of the equity in their firms as possible, but equity must often be shared with investors to obtain sufficient investment capital to support the firm’s growth. This issue is discussed in more detail in Chapter 10.

Get everything in Writing Many business disputes arise because of the lack of a written agreement or because poorly prepared written agreements do not anticipate potential areas of dispute.14 Although it is tempting to try to show business partners or employees that they are “trusted” by downplaying the need for a written agreement, this approach is usually a mistake. Disputes are much easier to resolve if the rights and obligations of the parties involved are in writing. For example, what if a new business agreed to pay a Web design firm $5,000 to design its website? The new business should know what it’s getting for its money, and the Web design firm should know when the project is due and when it will receive payment for its services. In this case, a dispute could easily arise if the parties simply shook hands on the deal and the Web design firm promised to have a “good-looking website” done “as soon as pos- sible.” The two parties could easily later disagree over the quality and function- ality of the finished website and the project’s completion date.

The experiences and perspectives of Maxine Clark, the founder of Build-A- Bear Workshop, provide a solid illustration of the practical benefits of putting things in writing, even when dealing with a trusted partner:

While I prefer only the necessary contracts (and certainly as few pages as possible), once you find a good partner you can trust, written up-front agreements are often a clean way to be sure all discussed terms are acceptable to all parties. It’s also a good idea after a meeting to be sure someone records the facts and agree-to points, and distributes them to all participants in writing. E-mail is a good method for do- ing this. Steps like this will make your life easier. After all, the bigger a business gets, the harder it is to remember all details about every vendor, contract, and meeting. Written records give you good notes for doing follow-up, too.15

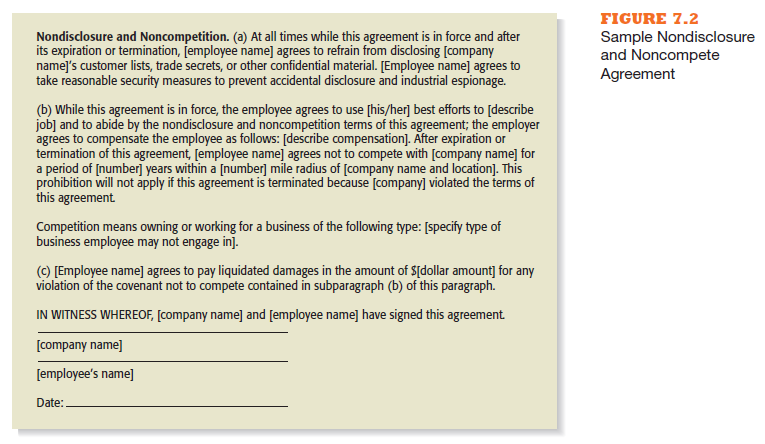

There are also two important written agreements that the majority of firms ask their employees to sign. A nondisclosure agreement binds an employee or another party (such as a supplier) to not disclose a company’s trade secrets. A noncompete agreement prevents an individual from competing against a former employer for a specific period of time. A sample nondisclosure and non- compete agreement is shown in Figure 7.2.

Set Standards Organizations should also set standards that govern employ- ees’ behavior beyond what can be expressed via a code of conduct. For example, four of the most common ethical problem areas that occur in an organization are human resource ethical problems, conflicts of interest, customer confi- dence, and inappropriate use of corporate resources. Policies and procedures should be established to deal with these issues. In addition, as reflected in the “Partnering for Success” boxed features throughout this book, firms are in- creasingly partnering with others to achieve their objectives. Because of this, entrepreneurial ventures should be vigilant when selecting their alliance part- ners. A firm falls short in terms of establishing high ethical standards if it is willing to partner with firms that behave in a contrary manner. This chapter’s “Partnering for Success” feature illustrates how two firms, Patagonia and Build- A-Bear Workshop, deal with this issue.

When legal disputes do occur, they can often be settled through nego- tiation or mediation, rather than more expensive and potentially damaging litigation. Mediation is a process in which an impartial third party (usually a professional mediator) helps those involved in a dispute reach an agreement.

At times, legal disputes can also be avoided by a simple apology and a sin- cere pledge on the part of the offending party to make amends. Yale profes- sor Constance E. Bagley illustrates this point.16 Specifically, in regard to the role a simple apology plays in resolving legal disputes, Professor Bagley refers to a Wall Street Journal article in which the writer commented about a jury awarding $2.7 million to a woman who spilled scalding hot McDonald’s cof- fee on her lap. The Wall Street Journal writer noted that “A jury awarded $2.7 million to a woman who spilled scalding hot McDonald’s coffee on her lap. Although this case is often cited as an example of a tort (legal) system run amok, the Wall Street Journal faulted McDonald’s for not only failing to re- spond to prior scalding incidents but also for mishandling the injured woman’s complaints by not apologizing.”17

A final issue important in promoting business ethics involves the man- ner in which entrepreneurs and managers demonstrate accountability to their investors and shareholders. This issue, which we discuss in greater detail in Chapter 10, is particularly important in light of the corporate scandals observed during the early 2000s, as well as scandals that may surface in future years.

Source: Barringer Bruce R, Ireland R Duane (2015), Entrepreneurship: successfully launching new ventures, Pearson; 5th edition.

Some really prime content on this web site, saved to fav.