Standards of sales performance facilitate the measurement of progress made towards departmental objectives. Specific objectives vary with changes in the company’s marketing situation, but are reconcilable with the general objectives of volume, profit, and growth. For instance, a general objective might be to add $10 million to sales volume, a figure in itself of little assistance for operating purposes. But using this objective as a point of departure, management chalks out plans to expand sales volume by $10 million. Through analysis of market factors, management may conclude that $10 million in additional sales can be made if two hundred new accounts are secured. Experience may indicate that 1,000 calls on prospects must be made to add 200 new accounts. Thus, in successive steps, the general sales volume objective is broken down into specific operating objectives. Performance standards are then established for the business as a whole and, ultimately, for each salesperson. These standards are used to gauge the extent of achievement of general and related specific objectives.

The first quantitative standard that any firm should select is one that permits comparisons of sales volume performance with sales volume potential. From the sales department’s standpoint, the volume objective is the most crucial and takes precedence over the profit and growth objectives. Before profits can be earned and growth achieved, it is necessary to reach a certain sales volume level. It is entirely logical for sales management first to develop a standard to gauge sales volume performance.

Quantitative performance standards can also be used to measure success in achieving profit objectives. Profits result from complex interactions of many factors, so the modicum of control over profits provided through the standard for sales volume is not enough. Standards should be set to bring some or all factors affecting profit under sales management’s control should. Performance standards, then, are needed for such factors as selling expense, the sales mixture, the call frequency rate, the cost per call, and the size of order.

Setting quantitative performance standards to gauge progress made toward growth objectives is even more complex. Growth objectives are met to some extent through the natural momentum picked up as a company approaches maturity, but performances by sales personnel impact upon growth. In an expanding economy, where the gross national product each year is larger than that in the year before, it is reasonable to expect individual sales personnel to show annual sales increases. However, this assumes that marketing management keeps products, prices, promotion, and other marketing policies in tune with market demand and that sales management’s efficiency is continuously improved. If these are logical assumptions, then the standards needed for individual sales personnel (besides successively higher sales volume and profit quotas each year) relate to such factors as increased sales to old accounts, sales to new accounts, calls on new prospects, sales of new products, and improvements in sales coverage effectiveness.

1. Quantitative Performance Standards

Most companies use quantitative performance standards. The particular combination of standards chosen varies with the company and its marketing situation. Quantitative standards, in effect, define both the nature and desired levels of performance. Indeed, quantitative standards are used for stimulating good performance as well as for measuring it.

Quantitative standards provide descriptions of what management expects. Each person on the sales force should have definitions of the performance aspects being measured and the measurement units. These definitions help sales personnel make their activities more purposeful. Sales personnel with well-defined objectives waste little time or effort in pursuing activities that do not contribute to reaching those objectives.

A single quantitative standard, such as one for sales volume attainment, provides an inadequate basis for appraising an individual’s total performance. In the past, the performances of individual sales personnel were measured solely in terms of sales volume. Today’s sales managers realize that it is possible to make unprofitable sales, and to make sales at the expense of future sales. In some fields—for example, industrial goods of high unit price—sales happen only after extended periods of preliminary work, and it is not only unfair but misleading to appraise performance over short intervals solely on the basis of sales volume.

Sales personnel have little control over many factors affecting sales volume. They should not be held accountable for “uncontrollables” such as differences in the strength of competition, the amount of promotional support given to the sales force, the potential territorial sales volume, the relative importance of sales to national or “house” accounts, and the amount of “windfall” business secured. Ample reason exists for setting other quantitative performance standards besides that for sales volume.

Each company selects that combination of quantitative performance standards that fits its marketing situation and selling objectives. If necessary, it develops its own unique standards designed best to serve those objectives. The standards discussed here are representative of the many types in use.

Quotas. A quota is a quantitative objective expressed in absolute terms and assigned to a specific marketing unit. The terms may be dollars, or units of product; the marketing unit may be a salesperson or a territory. As the most widely used quantitative standards, quotas specify desired levels of accomplishment for sales volume, gross margin, net profit, expenses, performance of nonselling activities, or a combination of these and similar items. When sales personnel are assigned quotas, management is answering the important question: How much for what period? The assumption is that management knows which objectives, both general and specific, are realistic and attainable. The validity of this assumption depends upon the market knowledge management has and utilizes in setting quotas. For instance, the first step in setting sales volume quotas is to estimate future demand for the company’s products in each sales territory—hence, sales volume quotas can be no better than the sales forecast underlying them. When sales volume quotas are based upon sound sales forecasts, in which the probable strength of demand has been fully considered, they are valuable performance standards. But when sales volume quotas represent little more than guesses, or when they have been chosen chiefly for inspirational effect, their value as control devices is dissipated.

Selling expense ratio. Sales managers use this standard to control the relation of selling expenses to sales volume. Many factors, some controllable by sales personnel and some not, cause selling expenses to vary with the territory, so target selling expense ratios should be set individually for each person on the sales force. Selling expense ratios are determined after analysis of expense conditions and sales volume potentials in each territory. An attractive feature of the selling expense ratio is that the salesperson can affect it both by controlling expenses and by making sales.

The selling expense ratio has several shortcomings. It does not take into account variations in the profitability of different products—so a salesperson who has a favorable selling expense ratio may be responsible for disproportionately low profits. Then, too, this performance standard may cause the salesperson to overeconomize on selling expenses to the point where sales volume suffers. Finally, in times of declining general business, selling expense ratios inhibit sales personnel from exerting efforts to bolster sales volume.

Practice differs as to what is counted as selling expenses. If national advertising, home office sales department expense, and branch managers’ and supervisors’ salaries and other indirect expenses are included and allocated to each territory, then sales personnel are accountable for expenses over which they have no control. But some sales executives argue that sales personnel influence the relation of indirect expenses to sales simply by putting forth some level of selling effort. In most companies, only expenses incurred directly by sales personnel, and controllable by them, are considered selling expenses. About one-half of all companies using this standard include the salesperson’s salary and/or incentive compensation in the computation; the rest consider only selling expenses incurred directly by sales personnel in performing their jobs. In firms in which sales personnel pay their own traveling expenses, the selling expense ratio is calculated by simply dividing the salesperson’s compensation by sales volume.

Selling expense ratio standards are used more by industrial-product companies than by consumer-product companies. The explanation traces to differences in the selling job. Industrial-product firms place the greater emphasis on personal selling and entertainment of customers; consequently, their sales personnel incur higher costs for travel and subsistence.

Territorial net profit or gross margin ratio. Target ratios of net profit or gross margin to sales for each territory focus sales personnel’s attention on the needs for selling a balanced line and for considering relative profitability (of different products, individual customers, and the like). Managements using either ratio as a quantitative performance standard, in effect, regard each sales territory as a separate organizational unit that should make a profit contribution. Sales personnel influence the net profit ratios by selling more volume and by reducing selling expenses. They may emphasize more profitable products and devote more time and effort to the accounts and prospects that are potentially the most profitable. The net profit ratio controls sales volume and expenses as well as net profit. The gross margin ratio controls sales volume and the relative profitability of the sales mixture (that is, sales of different products and to different customers), but it does not control the expenses of obtaining and filling orders.

Net profit and gross margin ratios have certain shortcomings. When either is a performance standard, sales personnel may “high-spot” their territories, neglect the solicitation of new accounts, and overemphasize sales of high-profit or high-margin products while underemphasizing new products that may be more profitable in the long run. Both ratios are influenced by factors beyond the salesperson’s control. For instance, pricing policy affects both net profit and gross margin, and delivery costs, which also affect both net profit and gross margin, and delivery costs, which also affect both net profit and gross margin, not only vary in different territories but are beyond the salesperson’s control. Neither ratio should be used without recognition of its shortcomings.

The net ratio profit presents computational problems. Since allocations of indirect selling expenses to territories are arbitrary, the practice is to use contribution to profit, which takes into account only direct selling expenses identifiable with particular territories. Similarly, questions arise as to whether sales salaries and commissions should be included in calculating territorial net profit.

Territorial market share. This standard controls market share on a territory-by-territory basis. Management sets target market share percentages for each territory. Management later compares company sales to industry sales in each territory and measures the effectiveness of sales personnel in obtaining market share. Closer control over the individual salesperson’s sales mixture is obtained by setting target market share percentages for each product and each class of customer or even for individual customers.

Sales coverage effectiveness index. This standard controls the thoroughness with which a salesperson works the assigned territory. The index consists of the ratio of the number of customers to the total prospects in a territory. For better apportion of the salesperson’s efforts among different classifications of prospects, individual standards for sales coverage effectiveness are set up for each class and size of customer.

Call-frequency ratio. A call-frequency ratio is calculated by dividing the number of sales calls on a particular class of customers by the number of customers in that class. By establishing different call-frequency ratios for different classes of customers, management directs selling effort to those accounts most likely to produce profitable orders. Management should assure that the interval between calls is proper—neither so short that unprofitably small orders are secured nor so long that sales are lost to competitors. Sales personnel who plan their own route and call schedules find target call frequencies helpful much as these standards provide information essential to this type of planning.

Calls per day. In consumer-product fields, where sales personnel contact large numbers of customers, it is desirable to set a standard for the number of calls per day. Otherwise, some sales personnel make too few calls per day and need help in planning their routes, in setting up appointments before making calls (in order to reduce waiting time or the number of cases where buyers are “unavailable”), or simply in starting their calls early enough in the morning and staying on the job late enough in the day. Other sales personnel make too many calls per day and need training in how to service accounts. Standards for calls per day are set individually for different territories, taking into account territorial differences as to customer density, road and traffic conditions, and competitors’ practices.

Order call ratio. This ratio measures the effectiveness of sales personnel in securing orders. Sometimes called a “batting average,” it is calculated by dividing the number of orders secured by the number of calls made. Order call ratio standards are set for each class of account. When a salesperson’s order call ratio for a particular class of account varies from the standard, the salesperson needs help in working with the class of account. It is common for sales personnel to vary in their effectiveness in selling to different kinds of accounts—one person may be effective in selling to small buyers and poor in selling to large buyers, another may have just the opposite performance pattern.

Average cost per call. To emphasize the importance of making profitable calls, a target for average cost per call is set. When considerable variation exists in cost of calling on different sizes or classes of accounts, standards are set for each category of account. Target average cost per call standards also are used to reduce the call frequency on accounts responsible for small orders.

Average order size. Average order size standards control the frequency of calls on different accounts. The usual practice is to set different standards for different sizes and classes of customers. Using average order size standards along with average cost per call standards, management controls the sales person’s allocation of effort among different accounts and increases order size obtained. Accomplishing this objective may require sales personnel to reduce the frequency of calls on some accounts.

Nonselling activities. Some companies establish quantitative performance standards for such nonselling activities as obtaining dealer displays and cooperative advertising contracts, training distributors’ personnel, and goodwill calls on distributors’ customers. Whenever nonselling activities become critical features of the sales job, appropriate standards should be set. Quantitative standards for nonselling activities are expressed in absolute terms, and hence, they are, in reality, quotas.

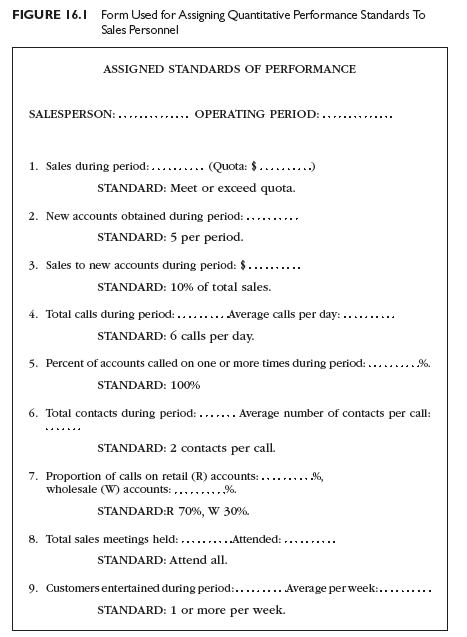

Multiple quantitative performance standards. It is widespread practice to assign multiple quantitative performance standards. Figure 16.1 shows a form used by a company whose sales personnel are assigned nine different quantitative standards per operating period.

2. Qualitative Performance Criteria

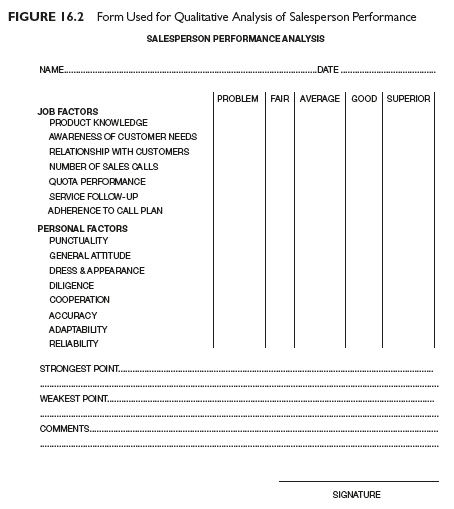

Certain aspects of job performance, such as personal effectiveness in handling customer relations problems, do not lend themselves to precise measurement, so the use of some qualitative criteria is unavoidable. Qualitative criteria are used for appraising performance characteristics that affect sales results, especially over the long run, but whose degree of excellence can be evaluated only subjectively. Qualitative criteria defy exact definition. Many sales executives, perhaps most, do not define the desired qualitative characteristics with any exactitude; instead, they arrive at informal conclusions regarding the extent to which each salesperson possesses them. Other executives consider the qualitative factors formally—one method being to rate sales personnel against a detailed checklist of subjective factors such as that shown in Figure 16.2.

Companies with merit-rating systems differ on the desirability of using numerical ratings. Most numerical scoring systems are in companies that rate sales personnel primarily for detecting needed adjustments in compensation. Companies that use merit rating primarily to improve and develop individual salespersons usually do not use numerical scoring systems.

Executive judgment plays the major role in the qualitative performance appraisal. Updated and accurate written job descriptions are the logical points of departure. Each firm develops its own set of qualitative criteria, based upon the job descriptions; the manner in which these criteria are applied depends upon the needs of management.

Source: Richard R. Still, Edward W. Cundliff, Normal A. P Govoni, Sandeep Puri (2017), Sales and Distribution Management: Decisions, Strategies, and Cases, Pearson; Sixth edition.

Those are yours alright! . We at least need to get these people stealing images to start blogging! They probably just did a image search and grabbed them. They look good though!