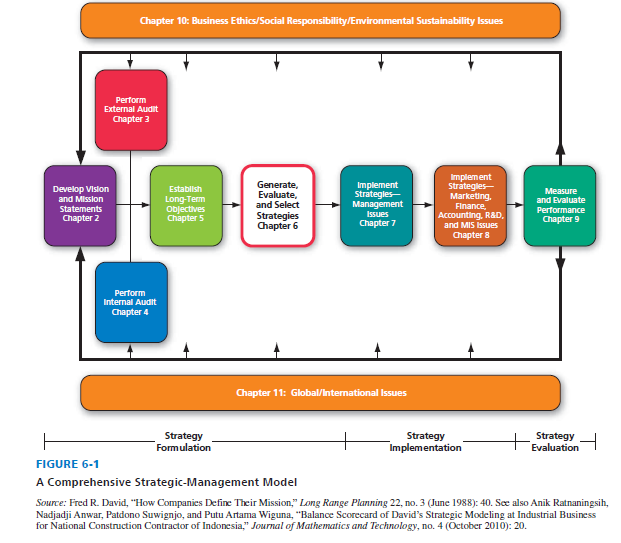

As indicated by Figure 6-1 with white shading, this chapter focuses on generating and evaluating alternative strategies, as well as selecting strategies to pursue. Strategy analysis and choice seek to determine alternative courses of action that could best enable the firm to achieve its mission and objectives. The firm’s present strategies, objectives, vision, and mission, coupled with the external and internal audit information, provide a basis for generating and evaluating feasible alternative strategies. This systematic approach is the best way to avoid an organizational crisis. Rudin’s Law states, “When a crisis forces choosing among alternatives, most people choose the worst possible one.” Unless a desperate situation confronts the firm, alternative strategies will likely represent incremental steps that move the firm from its present position to a desired future position. Alternative strategies do not come out of the wild blue yonder; they are derived from the firm’s vision, mission, objectives, external audit, and internal audit; they are consistent with, or build on, past strategies that have worked well.

1. The Process of Generating and Selecting Strategies

Strategists never consider all feasible alternatives that could benefit the firm because there are an infinite number of possible actions and an infinite number of ways to implement those actions. Therefore, a manageable set of the most attractive alternative strategies must be developed, examined, prioritized, and selected. The advantages, disadvantages, trade-offs, costs, and benefits of these strategies should be determined. This section discusses the process that many firms use to determine an appropriate set of alternative strategies. Recommendations (strategies selected to pursue) come from alternative strategies formulated.

Identifying and evaluating alternative strategies should involve many of the managers and employees who previously assembled the organizational vision and mission statements, performed the external audit, and conducted the internal audit. Representatives from each department and division of the firm should be included in this process, as was the case in previous strategy-formulation activities. Involvement provides the best opportunity for managers and employees to gain an understanding of what the firm is doing and why and to become committed to helping the firm accomplish its objectives.

All participants in the strategy analysis and choice activity should have the firm’s external and internal audit information available. This information, coupled with the firm’s vision and mission statements, will help participants crystallize in their own minds particular strategies that they believe could benefit the firm most. Creativity should be encouraged in this thought process.

Alternative strategies proposed by participants should be considered and discussed in a meeting or series of meetings. Proposed strategies should be listed in writing. When all feasible strategies identified by participants are given and understood, the strategies should be individually ranked in order of attractiveness by each participant, with 1 = should not be implemented, 2 = possibly should be implemented, 3 = probably should be implemented, and 4 = definitely should be implemented. Then, collect the participants’ ranking sheets and sum the ratings given for each strategy. Strategies with the highest sums are deemed the best, so this process results in a prioritized list of best strategies that reflects the collective wisdom of the group.

Source: David Fred, David Forest (2016), Strategic Management: A Competitive Advantage Approach, Concepts and Cases, Pearson (16th Edition).

Thanks for the sensible critique. Me & my neighbor were just preparing to do a little research on this. We got a grab a book from our area library but I think I learned more clear from this post. I’m very glad to see such great info being shared freely out there.