Budgeting outlines a retailer’s planned expenditures for a given time based on expected performance. Costs are linked to satisfying target market, employee, and management goals. What should labor costs be to attain a certain level of customer service? What compensation will motivate salespeople? What operating expenses will reach intended revenue and profit goals?

There are several benefits from a retailer’s meticulously preparing a budget:

- Expenditures are clearly related to expected performance, and costs can be adjusted as goals are revised. This enhances productivity.

- Resources are allocated to the right departments, product categories, and so on.

- Spending for various departments, product categories, and so on is coordinated.

- Because planning is structured and integrated, the goal of efficiency is prominent.

- Cost standards are set, such as advertising equals 5 percent of sales.

- A firm prepares for the future rather than reacts to it.

- Expenditures are monitored during a budget cycle. If a firm allots $50,000 to buy new merchandise, and it has spent $33,000 halfway through a cycle, it has $17,000 remaining.

- A firm can analyze planned budgets versus actual budgets.

- Costs and performance can be compared with industry averages.

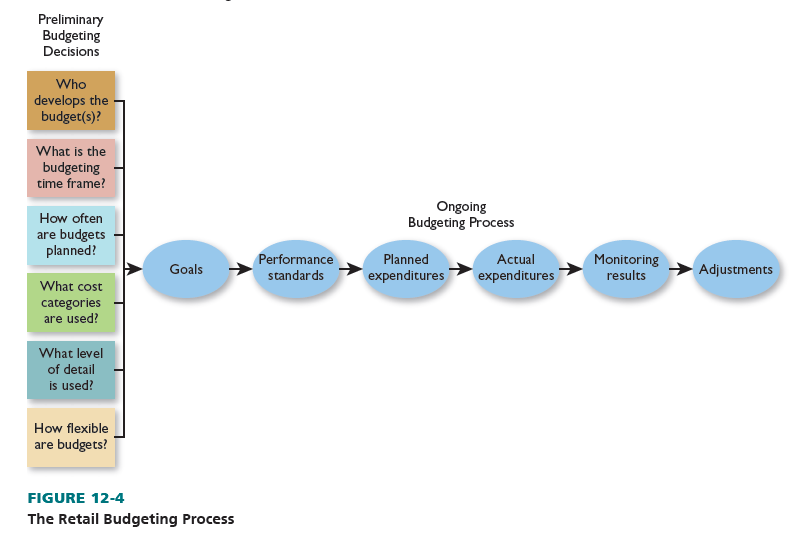

A retailer should be aware of the effort involved in the budgeting process, recognize that forecasts may not be fully accurate (due to unexpected demand, competitors’ tactics, and so on), and modify plans as needed. The process should not be too conservative (or inflexible) or simply add a percentage to each expense category to arrive at the next budget, such as increasing spending by 3 percent across the board based on anticipated sales growth of 3 percent. The budgeting process is shown in Figure 12-4 and described next.

1. Preliminary Budgeting Decisions

There are six preliminary decisions. First, budgeting authority is specified. In top-down budgeting, senior executives make centralized financial decisions and communicate them down the line to succeeding levels of managers. In bottom-up budgeting, lower-level executives develop departmental budget requests; these requests are assembled and a company budget is designed. Bottom-up budgeting includes varied perspectives, holds managers more accountable, and enhances employee morale. Many firms combine aspects of the two approaches.

Second, the time frame is defined. Most firms have budgets with yearly, quarterly, and monthly components. Annual spending is planned, and costs and performance are regularly reviewed. This responds to seasonal or other fluctuations. Sometimes, the time frame is longer than a year; other times it’s shorter than a month. When a firm opens new stores over a 5-year period, it sets construction costs for the entire period. When a supermarket orders perishables, it has weekly budgets for each item.

Third, budgeting frequency is determined. Many firms review budgets on an ongoing basis, but most plan them yearly. In some firms, several months may be set aside each year for the budgeting process; this lets all participants have time to gather data and facilitates taking the budgets through several drafts.

Fourth, cost categories are established:

- Capital expenditures are long-term investments in land, buildings, fixtures, and equipment. Operating expenditures are the short-term expenses of running a business.

- Fixed costs, such as store security, remain constant for the budget period regardless of the retailer’s performance. Variable costs, such as sales commissions, are based on performance. If performance is good, these expenses often rise. Figure 12-5 shows that the clock is always ticking with regard to the timing of costs.

- Direct costs are incurred by specific departments, product categories, and so on, such as the earnings of department-based salespeople. Indirect costs, such as centralized cashiers, are shared by multiple departments, product categories, and so on.

- Natural account expenses are reported by the names of the costs, such as salaries, and not assigned by purpose. Functional account expenses are classified on the basis of the purpose or activity for which expenditures are made, such as cashier salaries.

Fifth, the level of detail is set. Should spending be assigned by department (produce), product category (fresh fruit), product subcategory (apples), and/or product item (McIntosh apples)? With a very detailed budget, every expense subcategory must be adequately covered.

Sixth, budget flexibility is prescribed. A budget should be strict enough to guide planned spending and link costs to goals. Yet, a budget that is too inflexible may not let a retailer adapt to changing market conditions, capitalize on new opportunities, or modify a poor strategy (if further spending is needed to improve matters). Budget flexibility is often expressed in quantitative terms, such as allowing a buyer to increase a quarterly budget by a certain maximum percentage if demand is higher than anticipated.

2. Ongoing Budgeting Process

After making preliminary budgeting decisions, the retailer engages in the ongoing budgeting process shown in Figure 12-4:

- Goals are set based on customer, employee, and management needs.

- Performance standards are specified, including customer-service levels, the compensation needed to motivate employees, and the sales and profits needed to satisfy management. Typically, the budget is related to a sales forecast, which projects revenues for the next period. Forecasts are usually broken down by department or product category.

- Expenditures are planned in terms of performance goals. In zero-based budgeting, a firm starts each new budget from scratch and outlines the expenditures needed to reach that period’s goals.

- All costs are justified each time a budget is done. With incremental budgeting, a firm uses current and past budgets as guides and adds to or subtracts from them to arrive at the coming period’s spending. Most firms use incremental budgeting; it is easier, less time-consuming, and not as risky. Actual expenditures are made. The retailer pays rent and employee salaries, buys merchandise, places ads, and so on.

- Results are monitored: (1) Actual expenditures are compared with planned spending for each expense category, and reasons for any deviations are reviewed. (2) The firm learns if performance standards have been met and tries to explain deviations.

- The budget is adjusted. Revisions are major or minor, depending on how closely a firm has come to reaching its goals. The funds allotted to some expense categories may be reduced, while greater funds may be provided to other categories.

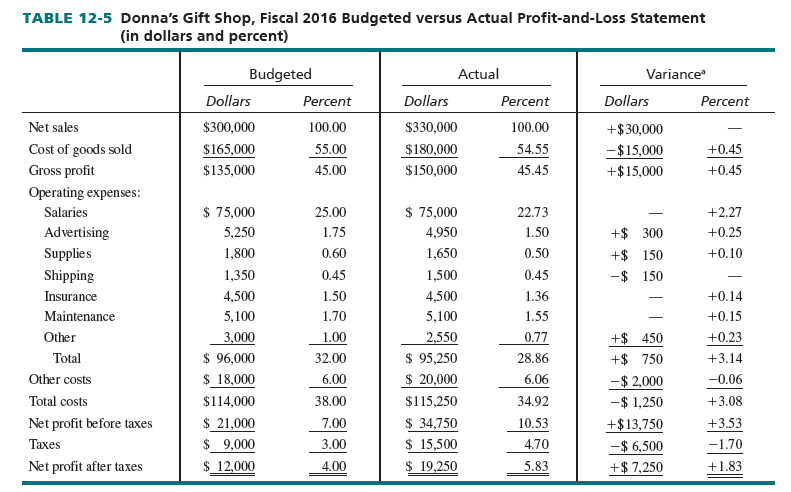

Table 12-5 compares budgeted and actual revenues, expenses, and profits for Donna’s Gift Shop during fiscal 2016. The actual data come from Table 12-1. The variance figures compare expected and actual results for each profit-and-loss item. Variances are positive if performance is better than expected and negative if it is worse.

As Table 12-5 indicates, in dollar terms, net profit after taxes was $7,250 higher than budgeted. Sales were $30,000 higher than expected; thus, the cost of goods sold was $15,000 higher. Actual operating expenses were $750 lower than expected, while other costs were $2,000 higher. Table 12-5 also shows results in percentage terms. This lets a firm evaluate budgeted versus actual performance on a percent-of-sales basis. In Donna’s case, actual net profit after taxes was 5.83 percent of sales—better than planned. The higher net profit was mostly due to the actual operating costs percentage being lower than planned.

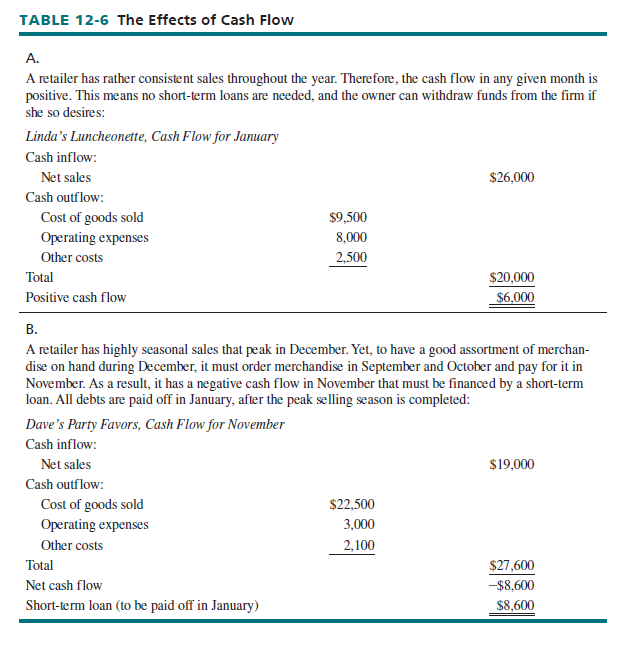

A firm must closely monitor cash flow, which relates the amount and timing of revenues received to the amount and timing of expenditures for a specific time. In cash flow management, the usual goal is to make sure revenues are received before expenditures are paid.20 Otherwise, short-term loans may be needed or profits may be tied up in inventory and other expenses. For seasonal retailers, this may be unavoidable. Underestimating costs and overestimating revenues, both of which affect cash flow, are leading causes of new business failures. Table 12-6 has cash flow examples.

Source: Barry Berman, Joel R Evans, Patrali Chatterjee (2017), Retail Management: A Strategic Approach, Pearson; 13th edition.

I am impressed with this internet site, really I am a big fan .