Unit control systems deal with quantities of merchandise in units rather than in dollars. Information typically reveals:

- Items selling well and those selling poorly

- Opportunities and problems in terms of price, color, style, size, and so on

- The quantity of goods on hand (if book inventory is used); minimizes overstocking and understocking

- An indication of inventory age, highlighting candidates for markdowns or promotions

- The optimal time to reorder merchandise

- Experiences with alternative sources (vendors) when problems arise

- The level of inventory and sales for each item in every store branch (This improves the transfer of goods between branches and alerts salespeople as to which branches have desired products. Also, less stock can be held in individual stores, reducing costs.)

1. Physical Inventory Systems

A physical inventory unit control system is similar to a physical inventory dollar control system. However, the latter is concerned with the financial value of inventory, whereas a unit control system looks at the number of units by item classification. With unit control, inventory levels are monitored either by visual inspection or actual count. See Figure 16-4.

In a visual inspection system, merchandise is placed on pegboard (or similar) displays, with each item numbered on the back or on a stock card. Minimum inventory quantities are noted, and sales personnel reorder when inventory reaches the minimum level. This is accurate only if items are placed in numerical order on displays (and sold accordingly). The system is used in the housewares and hardware displays of various discount and hardware stores. Although easy to maintain and inexpensive, it does not provide data on the rate of sales of individual items. And minimum stock quantities may be arbitrarily defined and not drawn from in-depth analysis.

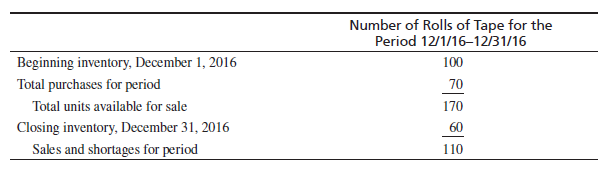

The other physical inventory system, actual counting, means regularly compiling the number of units on hand. This approach records—in units—inventory on hand, purchases, sales volume, and shortages for specified periods. A stock-counting system requires more clerical work but lets a firm obtain sales data for given periods and stock-to-sales relationships as of the time of each count. A physical system is not as sophisticated as a book system. It is more useful with low-value items having predictable sales. Handy Hardware could use the system for its insulation tape:

2. Perpetual Inventory Systems

A perpetual inventory unit control system keeps a running total of the number of units handled by a retailer through record keeping entries that adjust for sales, returns, transfers to other departments or stores, receipt of shipments, and other transactions. All additions to and subtractions from beginning inventory are recorded. Such a system can be applied manually, use merchandise tags processed by computers, or rely on point-of-sale devices such as optical scanners.

Point-of-sale systems—which are widely used today, even by many small retailers—feed data from merchandise tags or product labels directly to in-store computers for immediate data processing. Computer-based systems are quicker, more accurate, and of higher quality than manual ones. A manual system requires employees to gather data by examining sales checks, merchandise receipts, transfer requests, and other documents. Data are then coded and tabulated. A merchandise tagging system relies on pre-printed tags with data by department, classification, vendor, style, date of receipt, color, and/or material. When an item is sold, a copy of the tag is removed and sent to a tabulating facility for computer analysis. Since pre-printed tags are processed in batches, they can be used by smaller retailers that subscribe to service bureaus and by branches of chains (with data processed at a central location).

Current POS systems are easy to network; they have battery backup capabilities and run with standard PCs and software. Many of these systems use optical scanners to transfer data from products to computers by wands or other devices that pass over sensitized strips on the items. Figure 16-5 shows how barcoding works. As noted earlier, the UPC is the dominant format for coding data onto merchandise. This is how to interpret a barcode:

- The numbering systemcontains two (or possibly three) digits to identify the nation (or region) that assigns the manufacturer codes in that geographic area. In the typical UPC code, the initial number digit is 0—which is not shown on a label.

- The manufacturer codeis a series of distinctive numbers assigned to specific manufacturers by the coding authority of the nation or region. All of a given company’s products get the same manufacturer code—which is usually five numbers.

- The product codeis determined by each manufacturer—which can assign any five-digit product codes that it wants to designate different products by that company.

- The check digitis an additional number that helps verify that a specific barcode is scanned accurately. It is based on the other digits of a barcode.6

Many retailers combine perpetual and physical systems, whereby items accounting for a high proportion of sales are controlled by a perpetual system and other items are controlled by a physical inventory system. Attention is properly placed on the retailer’s most important products.

3. Unit Control Systems in Practice

Conducting a physical inventory is extremely time consuming and labor-intensive. It is also crucial: Having too much stock, or too little, is costly. The consulting firm, First Insight, has found that each year U.S. retailers lose about $280 billion due to holding excessive inventory.7 And the costs of not having sufficient inventory on hand are estimated to be more than $50 billion annually.

Retailers need to determine the “real” cost of excess, unsold inventory—which means considering not just the invoice and freight costs but also the cost of capital (the funds invested in unsold inventory), inventory-carrying costs (insurance and the cost of occupied space in warehouses or selling areas), handling costs, theft rates, product obsolescence if items are not sold quickly, and the opportunity cost of lost sales. Together, these inventory-related costs can mount up and have a big impact on profits. Having too much inventory can be as big a problem (or worse) than running out of merchandise, due to both the costs and the markdowns that might be necessary to move inventory. In some product categories, the marked-down inventory can cannibalize sales of full-price products.8 When all additional costs are taken into account, the total cost can be 25 to 30 percent more than the unit-cost value of the excess inventory.9

Source: Barry Berman, Joel R Evans, Patrali Chatterjee (2017), Retail Management: A Strategic Approach, Pearson; 13th edition.

28 May 2021

28 May 2021

28 May 2021

28 May 2021

28 May 2021

28 May 2021