A company may invest in the preferred or common stock of another company. The company investing in another company’s stock is the investor. The company whose stock is purchased is the investee.

The percent of the investee’s outstanding stock purchased by the investor determines the degree of control that the investor has over the investee. This, in turn, determines the accounting method used to record the stock investment, as shown in Exhibit 2.

1. Less Than 20% Ownership

If the investor purchases less than 20% of the outstanding stock of the investee, the investor is considered to have no control over the investee. In this case, it is assumed that the investor purchased the stock primarily to earn dividends or to realize gains on price increases of the stock.

Investments of less than 20% of the investee’s outstanding stock are accounted for using the cost method. Under the cost method, entries are recorded for the following transactions:

- Purchase of stock

- Receipt of dividends

- Sale of stock

Purchase of Stock The purchase of stock is recorded at its cost. Any brokerage commissions are included as part of the cost.

To illustrate, assume that on May 1, Bart Company purchases 2,000 shares of Lisa Company common stock at $49.90 per share plus a brokerage fee of $200. The entry to record the purchase of the stock is as follows:

Receipt of Dividends On July 31, Bart Company receives a dividend of $0.40 per share from Lisa Company. The entry to record the receipt of the dividend is as follows:

Dividend revenue is reported as part of Other income on Bart Company’s income statement.

Sale of Stock The sale of a stock investment normally results in a gain or loss. A gain is recorded if the proceeds from the sale exceed the book value (cost) of the stock. A loss is recorded if the proceeds from the sale are less than the book value (cost).

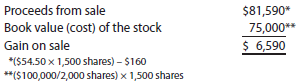

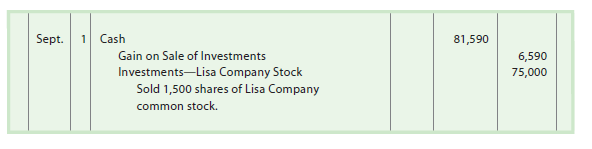

To illustrate, on September 1, Bart Company sells 1,500 shares of Lisa Company stock for $54.50 per share, less a $160 commission. The sale results in a gain of $6,590, as shown below.

The entry to record the sale is as follows:

The gain on the sale of investments is reported as part of Other income on Bart Company’s income statement.

2. Between 20%-50% Ownership

If the investor purchases between 20% and 50% of the outstanding stock of the investee, the investor is considered to have a significant influence over the investee. In this case, it is assumed that the investor purchased the stock primarily for strategic reasons, such as developing a supplier relationship.

Investments of between 20% and 50% of the investee’s outstanding stock are accounted for using the equity method. Under the equity method, the stock is recorded initially at its cost, including any brokerage commissions. This is the same as under the cost method.

Under the equity method, the investment account is adjusted for the investor’s share of the net income and dividends of the investee. These adjustments are as follows:

- Net Income: The investor records its share of the net income of the investee as an increase in the investment account. Its share of any net loss is recorded as a decrease in the investment account.

- Dividends: The investor’s share of cash dividends received from the investee decreases the investment account.

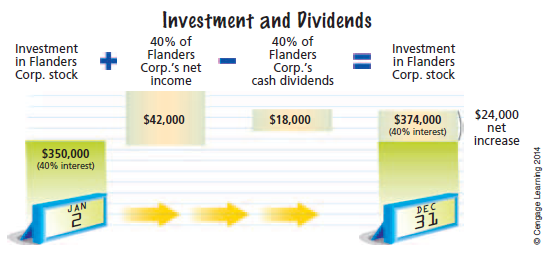

Purchase of Stock To illustrate, assume that Simpson Inc. purchased its 40% interest in Flanders Corporation’s common stock on January 2, 2014, for $350,000. The entry to record the purchase is as follows:

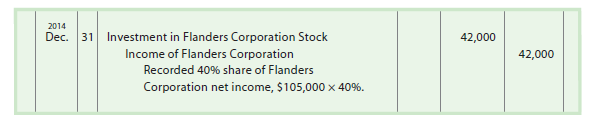

Recording Investee Net Income For the year ended December 31, 2014, Flanders Corporation reported net income of $105,000. Under the equity method, Simpson Inc. (the investor) records its share of Flanders net income, as shown on the next page.

Income of Flanders Corporation is reported on Simpson Inc.’s income statement. Depending on its significance, it may be reported separately or as part of Other income. If Flanders Corporation had a loss during the period, then the journal entry would be a debit to Loss of Flanders Corporation and a credit to the investment account.

Recording Investee Dividends During the year, Flanders declared and paid cash dividends of $45,000. Under the equity method, Simpson Inc. (the investor) records its share of Flanders dividends as follows:

The effect of recording 40% of Flanders Corporation’s net income and dividends is to increase the investment account by $24,000 ($42,000 – $18,000). Thus, Investment in Flanders Corporation Stock increases from $350,000 to $374,000, as shown below.

Under the equity method, the investment account reflects the investor’s proportional changes in the net book value of the investee. For example, Flanders Corporation’s net book value increased by $60,000 (net income of $105,000 less dividends of $45,000) during the year. As a result, Simpson’s share of Flanders’ net book value increased by $24,000 ($60,000 × 40%). Investments accounted for under the equity method are classified on the balance sheet as noncurrent assets.

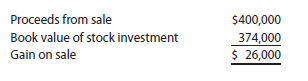

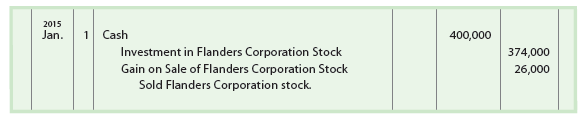

Sale of Stock Under the equity method, a gain or loss is normally recorded from the sale of an investment. A gain is recorded if the proceeds exceed the book value of the investment. A loss is recorded if the proceeds are less than the book value of the investment. To illlustrate, if Simpson Inc. sold Flanders Corporation’s stock on January 1, 2015, for $400,000, a gain of $26,000 would be reported, as shown below.

The entry to record the sale is as follows:

3. More Than 50% Ownership

If the investor purchases more than 50% of the outstanding stock of the investee, the investor is considered to have control over the investee. In this case, it is assumed that the investor purchased the stock of the investee primarily for strategic reasons.

The purchase of more than 50% ownership of the investee’s stock is termed a business combination. Companies may combine in order to produce more efficiently, diversify product lines, expand geographically, or acquire know-how.

A corporation owning all or a majority of the voting stock of another corporation is called a parent company. The corporation that is controlled is called the subsidiary company.

Parent and subsidiary corporations often continue to maintain separate accounting records and prepare their own financial statements. In such cases, at the end of the year, the financial statements of the parent and subsidiary are combined and reported as a single company. These combined financial statements are called consolidated financial statements. Such statements are normally identified by adding and Subsidiary(ies) to the name of the parent corporation or by adding Consolidated to the statement title.

To the external stakeholders of the parent company, consolidated financial statements are more meaningful than separate statements for each corporation. This is because the parent company, in substance, controls the subsidiaries. The accounting for business combinations, including preparing consolidated financial statements, is described and illustrated in advanced accounting courses and textbooks.

Source: Warren Carl S., Reeve James M., Duchac Jonathan (2013), Corporate Financial Accounting, South-Western College Pub; 12th edition.

Saved as a favorite, I really like your blog!