Capital needs to start the business or to finance current operations or expansion can be obtained from different sources. Internal financing should be explored before resorting to external funding sources. This includes using one’s own resources for initial capital needs and then retaining more profits in the business or reducing accounts receivables and inventories to meet current obligations and to finance growth and expansion. Such reductions in receivables or inventories should be applied carefully so as not to lead to a loss of customers or goodwill, both of which are critical to the viability of the business.

External financing takes different forms, and businesses use one or a combination of the following:

- Debt or equity financing: Debt financing occurs when an export-import firm borrows money from a lender with a promise to repay (principal and interest) at some predetermined future date. Equity financing involves raising money from private investors in exchange for a percentage of ownership (and sometimes participation in management) of the business. The major disadvantage of equity financing is the owner’s potential loss of control over the business (Cheng, 2009).

- Short-term, intermediate, or long-term financing: Short-term financing involves a credit period of less than one year, while intermediate financing is credit extended for a period of one to five years. In long-term financing, the credit period ranges between five and twenty years.

- Investment, inventory, or working-capital financing: Investment financing is money used to start the business (e.g., computer, fax machine, telephone). Inventory capital is money raised to purchase products for resale. Working capital supports current operations such as rent, advertising, supplies, and wages. All three could be financed by debt or equity.

Several sources of funding are available to existing export-import businesses that have established track records. However, financing is quite limited for initial capital needs, and the entrepreneur has to use his or her own resources or borrow from family or friends. It is also important to evaluate funding sources not just in terms of availability (willingness to provide funding) but also with regard to the capital’s cost and its effect on business profits, as well as any restrictions imposed by the lenders on the operations of the business. Certain loan agreements, for example, prevent the sale of accounts receivable or equipment or require the representation of lenders in the firm’s management. The following is an overview of possible sources of capital for export/import businesses.

1. Internal Sources

This is the best source of financing for initial capital needs or expansion because there is no interest to be paid back or equity in the business to be surrendered. Start-up businesses have limited chances of obtaining loans, making self-funding the only alternative. Internal sources include the following:

- Money in saving accounts, certificates of deposit, and other personal accounts

- Money in stocks, bonds, and money market funds

2. External Sources

2.1. Family and Friends

This is the second-best option for raising capital for an export-import business. The money should be borrowed with a promissory note indicating the date of payment and the amount of principal and interest to be paid. As long as the business pays a market interest rate, it is entitled to a tax deduction, and the lender gets the interest income. In the event the business fails to repay the loan, the lender may be able to deduct the amount as a short-term capital loss. Such an arrangement protects the lender and also keeps the lender from acquiring equity in the business.

2.2. Banks and Other Commercial Lenders

The largest challenge to successful lending is the turnover rate of small businesses. In general, fewer than half of all small businesses survive beyond the third-year mark. However, the survival rate for export-import businesses is generally higher than that for other businesses. Due to the level of risk, banks and other commercial lenders tend to avoid start-up financing without collateral. A 1994 IBM consulting group survey of small businesses revealed that bank credit was the most popular primary source of capital in the United States, followed by internally generated funds. Credit cards were not a significant source of financing. Of the businesses studied, 58 percent maintained a working capital line of credit, and 42 percent had term loans. Only 3 percent of the businesses used Small Business Administration (SBA) loans (Anonymous, 1995).

Banks remain the cheapest source of borrowed capital for export-import firms as well as other small businesses. To persuade a bank to provide a loan, it is essential to prepare a business plan that sets clear financial goals, including how the loan will be repaid. Banks always review the ability of the borrower to service the debt, whether sufficient cash is invested in the business, and the nature of the collateral that is to be provided as a guarantee for the loan. Bankers always investigate the five Cs in making lending decisions: character (trustworthiness, reliability), capacity (ability and track record in meeting financial obligations), capital (significant equity in the business), collateral (security for the loan), and condition (the effect of overall economic conditions) (Hisrich, Peters, and Shepherd, 2009; Lorenz-Fife, 1997). Even though it is often difficult to obtain a commercial loan for start-up capital, a good business plan and a strong, experienced management team may entice lenders to make a decision in favor of providing the loan. The following are different types of financing.

Asset-based financing: Banks and other commercial lenders provide loans secured byfixed assets, such as land, buildings, and machinery. For example, they will lend up to 80 percent of the value of one’s home minus the first mortgage. These are often long-term loans payable over a ten-year period. Business assets, such as accounts receivable, inventories, and personal assets (e.g., savings accounts, cars, jewelry) can be used as collateral for business loans. Commercial lenders usually lend up to 50 percent and 80 percent of their value of accounts receivable and inventories, respectively. Use of saving accounts as collateral could reduce interest payment on a loan. Suppose the interest on the savings account is 1 percent and the business loan is financed at 5 percent. The actual interest rate that is to be paid is reduced to 4 percent.

Lines of credit: These are short-term loans (for a period of one year) intended for purchases of inventory and payment of operating costs. They may sometimes be secured by collateral such as accounts receivable and the creditworthiness and reputation of the borrower. A certain amount of money (line of credit) is made available, and interest is often charged on the amount used. Certain lenders do not allow use of such lines of credit until the business’s checking account is depleted.

Personal and commercial loans: Owners with good credit standing could obtain personal loans that are backed by the mere signature and guarantee of the borrower. They are short-term loans and subject to relatively high interest rates. Commercial loans are also short-term loans that are often backed by stocks, bonds, and life insurance policies as collateral. The cash value of a life insurance policy can also be borrowed and repaid over a certain period of time (Hisrich et al., 2009).

Credit cards: Credit cards are generally not recommended for capital needs for new or existing export-import businesses because they are one of the costliest forms of business financing. They charge extremely high interest rates, and there is no limit on how much credit card issuers can charge for late fees and other penalties (Fraser, 1996). If financing options are limited, credit cards could be used if the probability of the business succeeding is very high (e.g., if you have made definite arrangements with foreign buyers). One should shop for the lowest available rates and plan for bank or credit union financing at a later date if the debt cannot be retired within a short time period, possibly with an account receivable or inventory as collateral. A survey of small and medium-size businesses, by Arthur Anderson and Company, in 1994, showed that 29 percent of businesses use credit cards for capital needs (Field, Korn, and Middleton, 1995).

2.3. Small Business Administration (SBA)

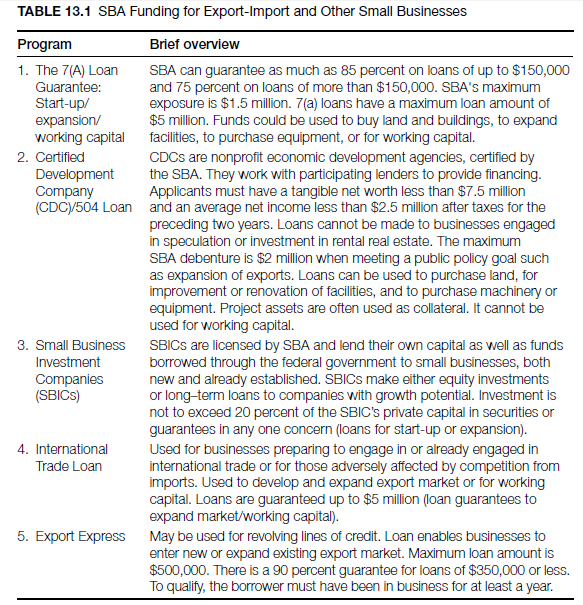

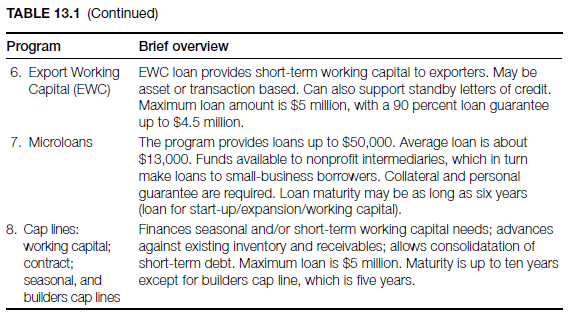

The SBA has several facilities for lending that can be used by export-import businesses for capital needs at different stages of their growth cycle (see Table 13.1).

Small business investment companies (SBICs): SBICs are private companies funded by the SBA that were established to provide loan (sometimes equity) capital to small businesses. Even though they prefer to finance existing small businesses with a track record, they also consider loans for start-up capital. Members of a minority group could also consider a similar lending agency funded by the SBA that is intended to finance minority start-ups or existing businesses.

The SBA (7(a) Loan Guarantee Program: An SBA guarantee permits a lending institution to provide long-term loans to start-up or existing small businesses. Export-import businesses can use the money for their working capital needs, for example, to purchase inventory and help carry a receivable until it is paid, to purchase real estate to house the business, or for acquisition of furniture and fixtures. The SBA guarantee is available only after the business has failed to obtain financing on reasonable terms from other private sources. It is considered to be a lender of last resort.

The Certified Development Company: The Certified Development Company (CDC 504) program assists in the development and expansion of small firms and the creation of jobs. This program is designed to provide fixed-asset financing and cannot be used for working capital or inventory, consolidating or repaying debt. (For an overview of SBA loans, see International Perspective 13.1)

3. Finance Companies

The following are different ways of raising capital from finance companies to start or expand an export-import business.

Loans from insurance companies and pension funds: Life insurance policies can be used as collateral to borrow money for capital needs. Pension funds also provide loans to businesses with attractive growth prospects. Pension funds and insurance company loans are intermediate- and long-term credits (five to fifteen years). Banks often introduce such lending agencies to their clients when the funds are needed for longer than the banks’ maximum maturity period.

Commercial finance companies: These companies grant short-term loans using accounts receivable, inventories, or equipment as collateral. They can also factor (buy) accounts receivable at a discount and provide the export-import firm the necessary capital for growth and expansion. Factoring is a way of turning a firm’s accounts receivable into immediate cash without creating new debt. The factoring company will collect the accounts receivable (A/R), assume credit risks associated with the A/R, conduct investigations on the firm’s existing and prospective accounts, and do the bookkeeping with respect to the credit. In most cases, a factoring company will advance 50 to 90 percent of the face value of the receivables and later pay the balance less the factor’s discount (4 to 7 percent of face value of receivables) once the receivables are collected. An export-import firm could easily factor its receivables so long as it sells to government clients or to major companies that have good credit. The disadvantage with this method is that it is expensive and could absorb a good part of the firm’s profits.

4. Equity Sources

For many export-import businesses, the ability to raise equity finance is quite limited. Although such funding provides the owner with initial capital needs, money for expansion, or working capital, it means some dilution of ownership and control. Finding compatible business partners and shareholders is always difficult. There are three sources for equity funding:

- Family and friends

- Business angels (invisible venture capitalists): Business angels provide start-up or expansion capital and are the biggest providers of equity capital for small businesses. They can be found through networking advertisements or newspapers or the World Wide Web. This segment is estimated to represent about 2,000 individuals or businesses investing between $10 billion and $20 billion each year in more than 30,000 businesses (Lorenz-Fife, 1997).

- Venture capitalists: Venture capitalists provide equity capital to businesses that are already established and need working or expansion capital. The Small Business Administration (SBA) estimates that 500 venture capital firms are currently investing about $4 billion a year in some 3,000 ventures. They may not be suitable for small export- import firms because:

- Their minimum investment is about $50,000 to 100,000.

- They seldom provide funding for start-up capital because they are interested in companies with a proven track record and market position.

- They expect high returns (10 to 15 percent) on their investments over a relatively short period of time.

Source: Seyoum Belay (2014), Export-import theory, practices, and procedures, Routledge; 3rd edition.

Howdy! This post could not be written any better! Reading this post reminds me of my old room mate! He always kept chatting about this. I will forward this post to him. Fairly certain he will have a good read. Thanks for sharing!