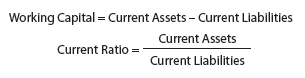

Current position analysis helps creditors evaluate a company’s ability to pay its current liabilities. This analysis is based on the following three measures:

- Working capital

- Current ratio

- Quick ratio

Working capital and the current ratio were discussed in Chapter 4 and are computed as follows:

While these two measures can be used to evaluate a company’s ability to pay its current liabilities, they do not provide insight into the company’s ability to pay these liabilities within a short period of time. This is because some current assets, such as inventory, cannot be converted into cash as quickly as other current assets, such as cash and accounts receivable.

The quick ratio overcomes this limitation by measuring the “instant” debt-paying ability of a company and is computed as follows:

![]()

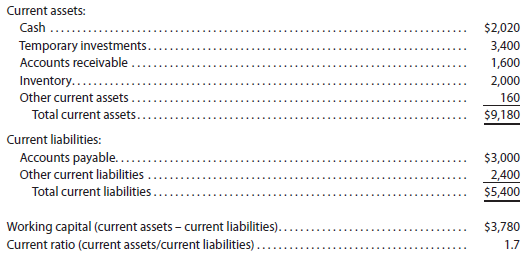

Quick assets are cash and other current assets that can be easily converted to cash. This normally includes cash, temporary investments, and accounts receivable. To illustrate, consider the following data for TechSolutions, Inc., at the end of 2013:

The quick ratio for TechSolutions, Inc., is computed as follows:

![]()

The quick ratio of 1.3 indicates that the company has more than enough quick assets to pay its current liabilities in a short period of time. A quick ratio below 1.0 would indicate that the company does not have enough quick assets to cover its current liabilities.

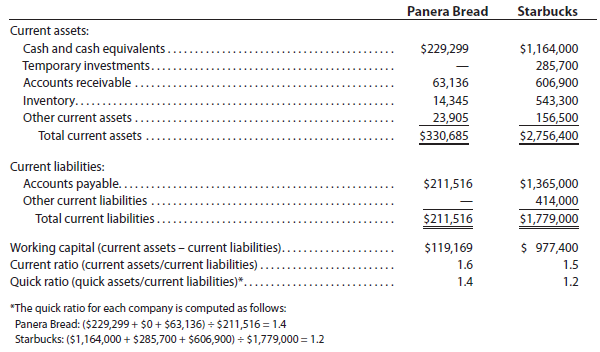

Like the current ratio, the quick ratio is particularly useful in making comparisons across companies. To illustrate, the following selected balance sheet data (excluding ratios) were taken from recent financial statements of Panera Bread Company and Starbucks Corporation (in thousands):

Starbucks is larger than Panera Bread and has over eight times the amount of working capital. Such size differences make working capital comparisons between companies difficult. In contrast, the current and quick ratios provide better comparisons across companies. In this example, Panera Bread has a slightly higher current ratio than Starbucks. However, Starbucks’ 1.2 quick ratio reveals that it has just enough quick assets to cover its current liabilities, while Panera Bread’s quick ratio of 1.4 indicates that the company has more than enough quick assets to meet its current liabilities.

Source: Warren Carl S., Reeve James M., Duchac Jonathan (2013), Corporate Financial Accounting, South-Western College Pub; 12th edition.

1 Jul 2021

1 Jul 2021

4 Feb 2018

1 Jul 2021

1 Jul 2021

1 Jul 2021