Under the direct write-off method, Bad Debt Expense is not recorded until the customer’s account is determined to be worthless. At that time, the customer’s account receivable is written off.

To illustrate, assume that on May 10 a $4,200 account receivable from D. L. Ross has been determined to be uncollectible. The entry to write off the account is as follows:

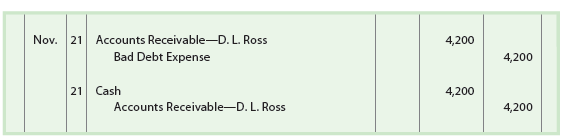

An account receivable that has been written off may be collected later. In such cases, the account is reinstated by an entry that reverses the write-off entry. The cash received in payment is then recorded as a receipt on account.

To illustrate, assume that the D. L. Ross account of $4,200 written off on May 10 is later collected on November 21. The reinstatement and receipt of cash is recorded as follows:

The direct write-off method is used by businesses that sell most of their goods or services for cash or through the acceptance of MasterCard or VISA, which are recorded as cash sales. In such cases, receivables are a small part of the current assets and any bad debt expense is small. Examples of such businesses are a restaurant, a convenience store, and a small retail store.

Source: Warren Carl S., Reeve James M., Duchac Jonathan (2013), Corporate Financial Accounting, South-Western College Pub; 12th edition.

Whats Taking place i am new to this, I stumbled upon this I’ve discovered It positively useful and it has aided me out loads. I hope to give a contribution & assist other users like its aided me. Great job.

I am not sure where you’re getting your info, but great topic. I needs to spend some time learning more or understanding more. Thanks for wonderful information I was looking for this information for my mission.