When a firm borrows money, it promises to make a series of interest payments and then to repay the amount that it has borrowed. If profits rise, the debtholders continue to receive only the fixed interest payment, so all the gains go to the shareholders. Of course, the reverse happens if profits fall. In this case, shareholders bear the greater part of the pain. If times are sufficiently hard, a firm that has borrowed heavily may not be able to pay its debts. The firm is then bankrupt, and shareholders lose most or all of their investment.

Because debt increases the returns to shareholders in good times and reduces them in bad times, it is said to create financial leverage. Leverage ratios measure how much financial leverage the firm has taken on. CFOs keep an eye on leverage ratios to ensure that lenders are happy to continue to take on the firm’s debt.

This means that 94 cents of every dollar of long-term capital is in the form of debt. Leverage is also measured by the debt-equity ratio. For Home Depot,

![]()

This means that 94 cents of every dollar of long-term capital is in the form of debt.

Leverage is also measured by the debt–equity ratio. For Home Depot,

![]()

Home Depot’s long-term debt ratio is very high for U.S. nonfinancial companies, but the CFO could fairly point out that the book value of the equity substantially understates its market value. Home Depot’s long-term debt is less than 2% of Home Depot’s market capitalization.

Some companies deliberately operate at very high debt levels. For example, in Chapter 32, we look at leveraged buyouts (LBOs). Firms that are acquired in a leveraged buyout usually issue large amounts of debt. When LBOs first became popular in the 1990s, these companies had average debt ratios of about 90%. Many of them flourished and paid back their debtholders in full; others were not so fortunate.

Notice that our measure of leverage ignores short-term debt. That probably makes sense if the short-term debt is temporary or is matched by similar holdings of cash, but if the company is a regular short-term borrower, it may be preferable to widen the definition of debt to include all liabilities. In this case,

![]()

Therefore, Home Depot is financed 97% with long- and short-term liabilities and 3% with equity.[1] We could also say that its ratio of total debt to equity is 43,075/1,454 = 29.6.

Managers sometimes refer loosely to a company’s leverage, but we have just seen that leverage may be measured in different ways. This is not the first time we have come across several ways to define a financial ratio. There is no law stating how a ratio should be defined. So be warned: Do not use a ratio without understanding how it has been calculated.

Times-Interest-Earned Ratio Another measure of financial leverage is the extent to which interest obligations are covered by earnings. Banks prefer to lend to firms whose earnings cover interest payments with room to spare. Interest coverage is measured by the ratio of earnings before interest and taxes (EBIT) to interest payments. For Home Depot,

![]()

The company enjoys a comfortable interest coverage or times-interest-earned ratio. Sometimes lenders are content with coverage ratios as low as 2 or 3.

The regular interest payment is a hurdle that companies must keep jumping if they are to avoid default. Times-interest-earned measures how much clear air there is between hurdle and hurdler. The ratio is only part of the story, however. For example, it doesn’t tell us whether Home Depot is generating enough cash to repay its debt as it comes due.

Cash Coverage Ratio In Chapter 26, we pointed out that depreciation is deducted when calculating the firm’s earnings, even though no cash goes out the door. Suppose we add back depreciation to EBIT to calculate operating cash flow.[3] We can then calculate a cash coverage ratio. For Home Depot,

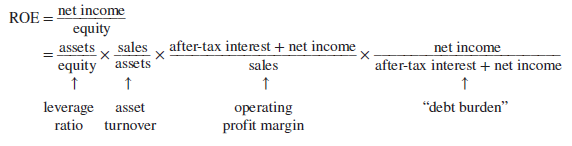

1. Leverage and the Return on Equity

When the firm raises cash by borrowing, it must make interest payments to its lenders. This reduces net profits. On the other hand, if a firm borrows instead of issuing equity, it has fewer equityholders to share the remaining profits. Which effect dominates? An extended version of the Du Pont formula helps us answer this question. It breaks down the return on equity (ROE) into four parts:

Notice that the product of the two middle terms is the return on assets. It depends on the firm’s production and marketing skills and is unaffected by the firm’s financing mix. However, the first and fourth terms do depend on the debt-equity mix. The first term, assets/equity, which we call the leverage ratio, can be expressed as (equity + liabilities)/equity, which equals 1 + total-debt-to-equity ratio. The last term, which we call the “debt burden,” measures the proportion by which interest expense reduces net income.

Suppose that the firm is financed entirely by equity. In this case, both the leverage ratio and the debt burden are equal to 1, and the return on equity is identical to the return on assets. If the firm borrows, however, the leverage ratio is greater than 1 (assets are greater than equity) and the debt burden is less than 1 (part of the profits is absorbed by interest). Thus, leverage can either increase or reduce return on equity. You will usually find, however, that leverage increases ROE when the firm is performing well and ROA exceeds the interest rate.

I’d perpetually want to be update on new posts on this site, saved to fav! .