In Chapter 1, Figure 1 depicts a control system as the fifth element of an international market entry strategy. Our intent here is to alert readers to the need for controlling entry strategies rather than describe control systems in any detail.

A management control system has three functions: (1) monitoring operations to identify variances between actual and planned performance, (2) diagnosing the causes of variances, with particular emphasis on negative variances, and (3) devising courses of action to eliminate or reduce variances. Managers exercise control, therefore, to make the results of operations conform to planning goals. Control is intimately involved with planning, because without control, planning becomes merely an intellectual exercise. Moreover, control may bring about remedial changes in a plan and, in any event, provides vital information for the ongoing planning process. On the other hand, control is meaningless without a planning process that creates standards against which performance can be measured by managers.9

1. Controlling the Constituent Entry Strategy

Control is an essential element of a constituent entry strategy focused on a single product and a single target country/market. The execution of an entry strategy requires translation of the international marketing plan into a tactical operating plan or budget, which usually covers the first year of the strategic plan. The budget, therefore, becomes the principal control instrument, with its goals and objectives serving as control standards. In establishing the budgets of country subsidiaries through interactive planning, it is the responsibility of corporate managers to make certain that those budgets are consistent with longer-term entry strategies; otherwise, the budgets of country subsidiaries are likely to be based on short-term objectives, and amount to little more than an extension of last year’s budgets. In sum, annual country budgets should be viewed as the current-period expression of the strategic entry plan.

International managers should control not only the performance of foreign subsidiaries but also the performance of licensees, agents, distributors, and other contractual parties in target markets. Admittedly, control cannot be as comprehensive for the latter as for the former, but some degree of control can always be achieved using reports about key performance variables, such as profitability, sales, and market share. However, our observations here apply particularly to controlling country subsidiaries.

To exercise control over the performance of country subsidiaries, corporate managers must overcome several difficulties peculiar to international business. Information for control purposes must cross many cultural, economic, political, legal, and other differences that create obstacles to effective communication between corporate and country managers. Another problem arises when corporate managers simply extend domestic control systems to cover foreign subsidiaries. When that happens, country managers are commonly burdened by reporting requirements that contribute little or nothing to control.

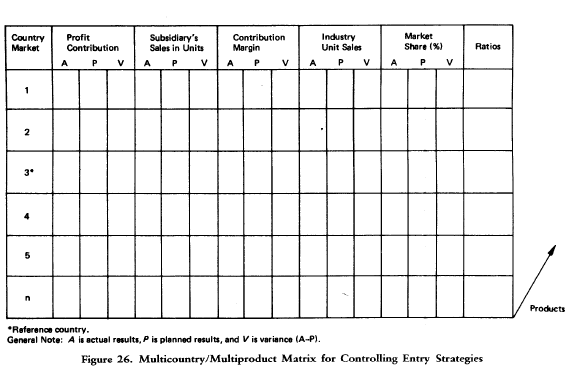

To illustrate the control process, figure 26 offers a product/country matrix to help corporate managers control constituent entry strategies as well as compare them across countries and products. Let us look first at a single row in Figure 26 that reports the operating results in the budget period for a particular product and country market.

The third-column entry is the variance in profit contribution. By itself this variance means little, but it can be allocated to a volume variance (the variance in the unit sales of the company’s product) and a price/cost variance (the variance in profit contribution per unit or contribution margin). This allocation may be expressed algebraically as follows:

![]()

where R represents profit contribution, S represents the subsidiary’s unit sales volume, C represents the contribution margin, and the subscripts a and p represent actual and planned results.10

The price/cost variance may be decomposed into a price variance and a cost variance according to the following equation:

![]()

where P represents price and K represents the unit variable cost. The cost variance may be further decomposed into specific cost variances.

The volume variance may be decomposed into a market-size variance (the variance in industry unit sales of the candidate-product type by all sellers) and a market-share variance. The market-size variance may be expressed as (Ma—Mp) EPCP, where M represents total industry sales in units, E, the subsidiary’s market share, and C, the contribution margin. The market-share variance becomes (Ea—Ep) M„MP.”

After corporate managers have allocated the profit-contribution variance to variances in price, cost, market size, and market share, they are prepared to raise “why” questions—to ask about the causes of these variances. Ultimately, managers must decide whether negative variances air attributable to poor planning or to poor performance.’1 Was the entry strategy for this country faulty in one or more of its elements, or was its execution inadequate, or both? There is no easy quantitative answer to this question. Somehow corporate managers must evaluate the performance of a country manager in the light of ex post information, some of which is quantitative and some of which is qualitative. That is to say, they must answer the question: What should this manager have accomplished in the actual circumstances of the budget period? Any remaining variance is traceable to the strategy itself. Corporate managers must distinguish between planning variance and performance variance if they are to undertake the proper remedial action.

2. Controlling Entry Strategies Across Countries and Products

The primary focus of a control system is on the individual country program for a candidate product. But in a global enterprise, comparisons of programs across countries for the same product and comparisons across products within countries are also part of the international control system. Just as systematic comparisons of market and sales potentials are needed to choose the most attractive target markets, so are systematic comparisons across countries and products needed for effective control. By spotting country and product variations in the several performance measures, control comparisons can raise important questions with respect to market and sales potentials, weaknesses and strengths in country/product performance, new opportunities, the design of entry strategies, and other issues. Such comparisons offer corporate managers another way to apply experience in one country or product to another country or product. It may also be argued that a comparative control standard is more objective than a standard confined to a single country market or product. But for comparisons to be meaningful, the corporate control system should be standardized across countries and products.

Comparative performance assessments should not be misused by corporate managers in rewarding or punishing country managers. Country managers are inclined to resent any form of country comparisons, but they will surely sabotage a control system that generates unfair comparisons. Hence corporate managers need to be objective in distinguishing performance variances from planning variances. For that reason, comparisons between countries belonging to the same secondary group with similar marketing mix profiles are most defensible as well as most meaningful.

Returning to Figure 26, comparisons down the columns reveal differences in results among country subsidiaries. Comparisons may be facilitated by using one country’s program as a reference program or, alternatively, by using “average” results. Ratio comparisons among country programs that relate specific inputs to marketing results can be particularly useful, because discrepancies trigger further inquiry.13 Why is advertising for the candidate product 1.5 percent of sales in one country while it is no higher than 1 percent in other countries? Are we spending too much on advertising in that country or too little in other countries? Or is there another explanation? Enlightening comparisons may also be made across different products, as indicated by the arrow marked “products” in Figure 26.

3. Redesigning Entry Strategies

Once corporate managers have correctly diagnosed the cause or causes of variances in a foreign subsidiary’s performance, they must decide on remedial action. Performance variances call for improvement in local management; planning variances call for a revision of entry strategy.

Any or all of the elements of entry strategy (the target product/market, objectives, entry mode, or the marketing plan) may be the source of planning variances. Accordingly, remedial action may lead to a revision of any or all of these elements. For example, if the source of negative variance is a lower industry market potential than the one assumed in the entry plan, remedies may range from abandoning the market entirely to simply lowering sales objectives in a revised strategy. Or again, if the negative variance proceeds from market share, remedies may include a step-up in total marketing effort and/or a shift in the composition of the marketing mix, say, a drop in price together with a lower advertising expenditure. If the cause of a negative variance is new import or investment restrictions, the appearance of a strong competitor, or political instability, then remedial action may include a change in the entry mode, such as moving from export to investment entry or from investment entry to export or licensing entry.

Corporate managers should respond to positive variances as well as negative variances. A positive planning variance carries an opportunity cost, because it means that corporate planners have not taken full advantage of market opportunity in a target country: they underestimated the overall market size, the market share, or the contribution margin. Persistent positive variances are almost a sure sign of poor planning.

The revision of entry strategies to eliminate variances is necessary but not sufficient to achieve good strategies. As pointed out in Chapter 1, entry planning is a continuous process: entry strategies should be periodically reviewed to take account of changes both external and internal to the global enterprise. Such reviews keep entry strategies more closely attuned to new circumstances and thereby minimize future planning variances. Only in this way can international companies design cost-effective strategies in a turbulent world.

Source: Root Franklin R. (1998), Entry Strategies for International Markets, Jossey-Bass; 2nd edition.

Magnificent beat ! I wish to apprentice at the same time as

you amend your site, how could i subscribe for a weblog web site?

The account helped me a acceptable deal. I were a little bit acquainted of this your broadcast provided brilliant clear

idea

What’s up, I would like to subscribe for this blog to get newest updates, thus

where can i do it please assist.

I want looking through and I conceive this website got some truly useful stuff on it! .