In 1979, the United States adopted the customs valuation system that was the result of the Tokyo Round negotiations of the GATT. Valuation of a product is important because most imported products are subject to tariffs based on the percentage of the value of the import (ad valorem rate). It also helps countries to maintain accurate and comparable records of their international trade transactions (International Perspective 18.3).

Imported merchandise is appraised on the basis and in the order of the following:

- Transaction value

- Deductive value

- Computed value

1. The Transaction Value

Transaction value is the invoice price of the goods as they enter the United States. In determining transaction value, the price actually paid or payable will be considered without regard to its method of derivation. The value includes various costs that enhance the good’s value to the importer (i.e. packing costs, sales commissions, and royalties). It also includes any direct or indirect items provided by the buyer free of charge or at a reduced cost for use in the production or sale of merchandise for export to the United States. In short, the transaction value is the price actually paid or payable for imported merchandise, excluding international freight, insurance and other CIF charges. Transaction value cannot be used in the following situations:

- In cases in which the transaction value cannot be determined (e.g., proceeds of subsequent sales) or is not acceptable (related-party transactions)

- In cases involving restrictions on the sale or use of the product.

Example 1: A foreign shipper sold merchandise at $1,500 to a U.S. buyer. The seller subsequently increased the price to $1,650. The invoice price is $1,500 because that was the price agreed to and actually paid by the importer. The merchandise should be appraised at $1,500 because that was the price actually paid by the buyer—the transaction value.

Example 2: DM, Inc., a firm located in Miami, Florida, purchased 10,000 barrels of crude oil from a Venezuelan oil company, Soto, Inc., for $250,000. The price consists of $200,000 for the oil and $50,000 for ocean freight and insurance. Soto would have charged $210,000 for the oil. However, since it owes DM $10,000, Soto charged DM only $200,000 for the oil. The transaction value is $210,000, that is, the sum of ($200,000 + $10,000), excluding CIF charges of $50,000 for ocean freight and insurance.

If the transaction value cannot be determined, the transaction value of an identical product or, in the absence of the latter, the transaction value of a similar product (commercially interchangeable) will be used. The transaction value of identical and similar merchandise (ISM) will be used under the following circumstances:

- The products (ISM) must have been sold for export to the United States at or about the same time as the merchandise being appraised.

- Value must be based on sales of ISM at the same commercial level and in substantially the same quantity as the sale of the merchandise being appraised.

- The ISM must be produced in the same country and by the same person (if not available, by a different person) as the merchandise being appraised.

- In cases involving two or more transaction values for ISM, the lowest value will be used as the appraised value of the imported merchandise.

2. Deductive Value

This method is used when the transaction value cannot be determined, such as sales between related parties. However, if the importer designates computed value as the preferred method of appraisement, the latter can be used as the next basis of determining value. Deductive value is essentially the resale price of an imported product, with deductions for commissions, profit, and general expenses; transportation and insurance costs (from the country of export to the United States); import duties and taxes; and any cost of further processing after importation. The deductive value is generally calculated by starting with the unit price and making additions to (such as packing costs) and deductions from that price (see International Perspective 18.3).

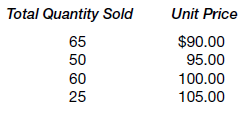

Example 1: Merchandise is sold to an unrelated person from a price list that provides favorable unit prices for purchases in larger quantities:

In this example, the unit price used in determining deductive value is $90, since the greatest quantity is sold at that price.

Example 2: A foreign parent company sells parts to its U.S. subsidiary in Texas. The product is not sold to unrelated parties, and there is no similar or identical merchandise from the country of production. The U.S. subsidiary further

processes the product and sells it to an unrelated buyer in Florida within 180 days after importation.

In this example, the merchandise should be appraised under deductive value, with allowances for profit and general expenses, freight and insurance, duties and taxes, and the cost of processing.

3. Computed Value

The computed value starts with the costs of the materials, labor, and overhead in producing the imported goods. Customs then adds profits and general expenses incurred by the producer (based on average estimates for similar goods in the same country), as well as the prorated value of any materials supplied by the buyer free of charge or at reduced price and packing costs (U.S. Department of Commerce, 2003).

Example: Suppose that under Example 2 the U.S. importer requested that the shipment be appraised under computed value. The merchandise is appraised using the company’s profit and general expenses if not inconsistent with sales of merchandise of the same class or kind.

If none of the previous methods can be used to appraise the imported merchandise, the customs value is based on a value derived from one of these methods, reasonably adjusted or administered flexibly. If an identical or similar product, for example, is not available in the exporting country, customs could appraise an identical or similar product from a third country to determine value.

Source: Seyoum Belay (2014), Export-import theory, practices, and procedures, Routledge; 3rd edition.

After study a few of the blog posts on your website now, and I truly like your way of blogging. I bookmarked it to my bookmark website list and will be checking back soon. Pls check out my web site as well and let me know what you think.

Good write-up, I’m normal visitor of one’s blog, maintain up the excellent operate, and It is going to be a regular visitor for a long time.