An accounting issue arises when identical units of merchandise are acquired at different unit costs during a period. In such cases, when an item is sold, it is necessary to determine its cost using a cost flow assumption and related inventory costing method. Three common cost flow assumptions and related inventory costing methods are shown below.

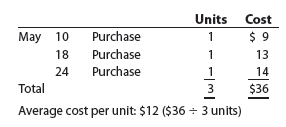

To illustrate, assume that three identical units of merchandise are purchased during May, as follows:

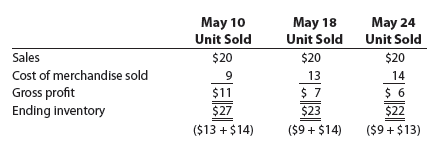

Assume that one unit is sold on May 30 for $20. Depending upon which unit was sold, the gross profit varies from $11 to $6 as shown below.

Under the specific identification inventory cost flow method, the unit sold is identified with a specific purchase. The ending inventory is made up of the remaining units on hand. Thus, the gross profit, cost of merchandise sold, and ending inventory can vary as shown above. For example, if the May 18 unit was sold, the cost of merchandise sold is $13, the gross profit is $7, and the ending inventory is $23.

The specific identification method is not practical unless each inventory unit can be separately identified. For example, an automobile dealer may use the specific identification method since each automobile has a unique serial number. However, most businesses cannot identify each inventory unit separately. In such cases, one of the following three inventory cost flow methods is used.

Under the first-in, first-out (FIFO) inventory cost flow method, the first units purchased are assumed to be sold and the ending inventory is made up of the most recent purchases. In the preceding example, the May 10 unit would be assumed to have been sold. Thus, the gross profit would be $11, and the ending inventory would be $27 ($13 + $14).

Under the last-in, first-out (LIFO) inventory cost flow method, the last units purchased are assumed to be sold and the ending inventory is made up of the first purchases. In the preceding example, the May 24 unit would be assumed to have been sold. Thus, the gross profit would be $6, and the ending inventory would be $22 ($9 + $13).

Under the weighted average inventory cost flow method, sometimes called the average cost flow method, the cost of the units sold and in ending inventory is a weighted average of the purchase costs. The purchase costs are weighted by the quantities purchased at each cost, thus the term weighted average. In the preceding example, the cost of the unit sold would be $12 ($36 f 3 units), the gross profit would be $8 ($20 – $12), and the ending inventory would be $24 ($12 x 2 units). In this example, the purchase costs are weighted equally, since the same quantity (one) was purchased at each cost.

The three inventory cost flow methods, FIFO, LIFO, and weighted average, are shown in Exhibit 1. The frequency with which the FIFO, LIFO, and weighted average methods are used is shown in Exhibit 2.

Source: Warren Carl S., Reeve James M., Duchac Jonathan (2013), Corporate Financial Accounting, South-Western College Pub; 12th edition.

1 Jul 2021

1 Jul 2021

30 Jun 2021

1 Jul 2021

1 Jul 2021

1 Jul 2021