As discussed in Chapter 3, the adjusting entries are recorded in the journal at the end of the accounting period. For NetSolutions, the adjusting entries are shown in Exhibit 9 of Chapter 3.

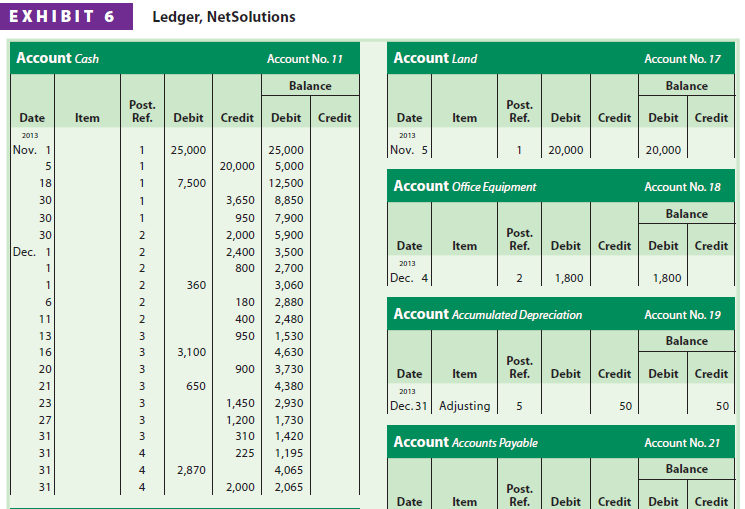

After the adjusting entries are posted to NetSolutions’ ledger, shown in Exhibit 6 (on pages 160-161), the ledger agrees with the data reported on the financial statements.

The balances of the accounts reported on the balance sheet are carried forward from year to year. Because they are relatively permanent, these accounts are called permanent accounts or real accounts. For example, Cash, Accounts Receivable, Equipment, Accumulated Depreciation, Accounts Payable, Capital Stock, and Retained Earnings are permanent accounts.

The balances of the accounts reported on the income statement are not carried forward from year to year. Also, the balance of the dividends account, which is reported on the retained earnings statement, is not carried forward. Because these accounts report amounts for only one period, they are called temporary accounts or nominal accounts. Temporary accounts are not carried forward because they relate only to one period. For example, the Fees Earned of $16,840 and Wages Expense of $4,525 for NetSolutions shown in Exhibit 2 are for the two months ending December 31, 2013, and should not be carried forward to 2014.

At the beginning of the next period, temporary accounts should have zero balances. To achieve this, temporary account balances are transferred to permanent accounts at the end of the accounting period. The entries that transfer these balances are called closing entries. The transfer process is called the closing process and is sometimes referred to as closing the books.

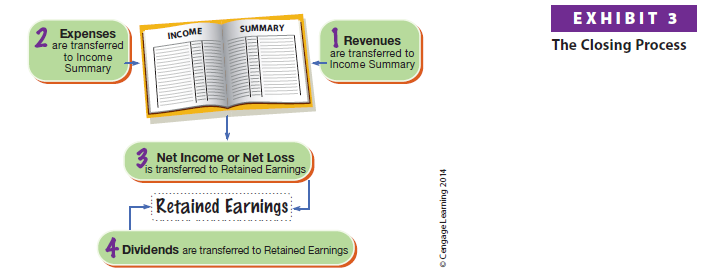

The closing process involves the following four steps:

- Revenue account balances are transferred to an account called Income Summary.

- Expense account balances are transferred to an account called Income Summary.

- The balance of Income Summary (net income or net loss) is transferred to the retained earnings account.

- The balance of the dividends account is transferred to the retained earnings account.

Exhibit 3 diagrams the closing process.

Income Summary is a temporary account that is only used during the closing process. At the beginning of the closing process, Income Summary has no balance. During the closing process, Income Summary will be debited and credited for various amounts. At the end of the closing process, Income Summary will again have no balance. Because Income Summary has the effect of clearing the revenue and expense accounts of their balances, it is sometimes called a clearing account. Other titles used for this account include Revenue and Expense Summary, Profit and Loss Summary, and Income and Expense Summary.

The four closing entries required in the closing process are as follows:

- Debit each revenue account for its balance and credit Income Summary for the total revenue.

- Credit each expense account for its balance and debit Income Summary for the total expenses.

- Debit Income Summary for its balance and credit the retained earnings account.

- Debit the retained earnings account for the balance of the dividends account and credit the dividends account.

In the case of a net loss, Income Summary will have a debit balance after the first two closing entries. In this case, credit Income Summary for the amount of its balance and debit the retained earnings account for the amount of the net loss.

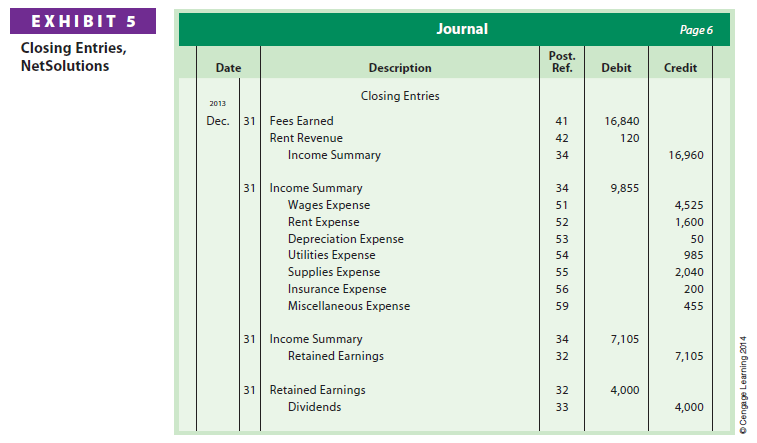

Closing entries are recorded in the journal and are dated as of the last day of the accounting period. In the journal, closing entries are recorded immediately following the adjusting entries. The caption, Closing Entries, is often inserted above the closing entries to separate them from the adjusting entries.

It is possible to close the temporary revenue and expense accounts without using a clearing account such as Income Summary. In this case, the balances of the revenue and expense accounts are closed directly to the retained earnings account.

2. Journalizing and Posting Closing Entries

A flowchart of the four closing entries for NetSolutions is shown in Exhibit 4. The balances in the accounts are those shown in the Adjusted Trial Balance columns of the end-of-period spreadsheet shown in Exhibit 1.

The closing entries for NetSolutions are shown in Exhibit 5. The account titles and balances for these entries may be obtained from the end-of-period spreadsheet, the adjusted trial balance, the income statement, the retained earnings statement, or the ledger.

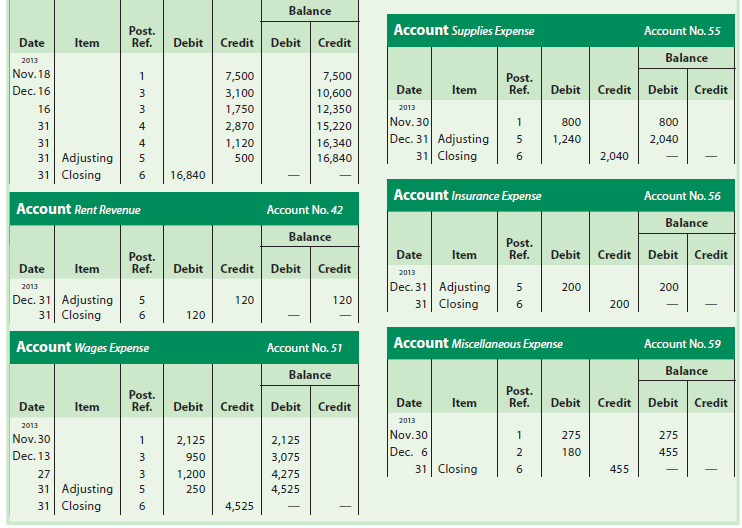

The closing entries are posted to NetSolutions’ ledger as shown in Exhibit 6 (pages 160-161). Income Summary has been added to NetSolutions’ ledger in Exhibit 6 as account number 34. After the closing entries are posted, NetSolutions’ ledger has the following characteristics:

- The balance of Retained Earnings of $3,105 agrees with the amount reported on the retained earnings statement and the balance sheet.

- The revenue, expense, and dividends accounts will have zero balances.

As shown in Exhibit 6, the closing entries are normally identified in the ledger as “Closing.” In addition, a line is often inserted in both balance columns after a closing entry is posted. This separates next period’s revenue, expense, and dividend transactions from those of the current period. Next period’s transactions will be posted directly below the closing entry.

3. Post-Closing Trial Balance

A post-closing trial balance is prepared after the closing entries have been posted. The purpose of the post-closing (after closing) trial balance is to verify that the ledger is in balance at the beginning of the next period. The accounts and amounts should agree exactly with the accounts and amounts listed on the balance sheet at the end of the period. The post-closing trial balance for NetSolutions is shown in Exhibit 7.

Source: Warren Carl S., Reeve James M., Duchac Jonathan (2013), Corporate Financial Accounting, South-Western College Pub; 12th edition.

Hi! This is my first visit to your blog! We are a collection of volunteers and starting a new

project in a community in the same niche. Your blog provided us useful information to work on. You have done a outstanding

job!

I am really grateful to the owner of this website who has shared this fantastic piece of writing at

at this time.

It’s really a great and helpful piece of information. I’m glad that

you just shared this useful info with us.

Please stay us informed like this. Thanks for sharing.