Almost all top executives of firms with publicly traded shares have compensation packages that depend in part on their firms’ stock price performance. But their compensation also includes a bonus that depends on increases in earnings or on other accounting measures of performance. For lower-level managers, compensation packages usually depend more on accounting measures and less on stock returns.

Accounting measures of performance have two advantages:

- They are based on absolute performance, rather than on performance relative to investors’ expectations.

- They make it possible to measure the performance of junior managers whose responsibility extends to only a single division or plant.

Tying compensation to accounting profits also creates some obvious problems. For example, managers whose pay or promotion depends on short-term profits may cut back on training, advertising, or R&D. This is not a recipe for adding value because these outlays are investments that should pay off in later years. Nevertheless, the outlays are treated as current expenses and deducted from current income. Thus, an ambitious manager is tempted to cut back, thereby increasing current income, leaving longer-run problems to his or her successor.

In addition, accounting earnings and rates of return can be severely biased measures of true profitability. We ignore this problem for now, but return to it in the next section.

Finally, growth in earnings does not necessarily mean that shareholders are better off. Any investment with a positive rate of return (1% or 2% will do) will eventually increase earnings. Therefore, if managers are told to maximize growth in earnings, they will dutifully invest in projects offering 1% or 2% rates of return—projects that destroy value. But shareholders do not want growth in earnings for its own sake, and they are not content with 1% or 2% returns. They want positive-NPV investments, and only positive-NPV investments. They want the company to invest only if the expected rate of return exceeds the cost of capital.

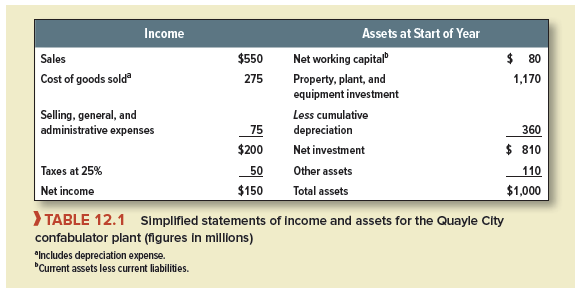

Look at Table 12.1, which contains a simplified income statement and balance sheet for your company’s Quayle City confabulator plant. There are two methods for judging whether the plant’s returns are higher than the cost of capital.

Book return on investment (ROI) is just the ratio of after-tax operating income to the net (depreciated) book value of assets.[1] In Chapter 5, we rejected book ROI as a capital investment criterion, and in fact, few companies now use it for that purpose. However, managers frequently assess the performance of a division or a plant by comparing its ROI with the cost of capital.

Suppose you need to assess the performance of the Quayle City plant. As you can see from Table 12.1, the corporation has $1,000 million invested in the plant, which is generating earnings of $150 million. Therefore, the plant is earning an ROI of 150/1,000 = .15, or 15%.23 If the cost of capital is (say) 10%, then the plant’s activities are adding to shareholder value. The net return is 15 – 10 = 5%. If the cost of capital is (say) 20%, then shareholders would have been better off investing $1 billion somewhere else. In this case the net return is negative, at 15 – 20 = -5%.

1. Residual Income or Economic Value Added (EVA®)24

When firms calculate income, they start with revenues and then deduct costs, such as wages, raw material costs, overhead, and taxes. But there is one cost that they do not commonly deduct: the cost of capital. True, they allow for depreciation, but investors are not content with a return of their investment; they also demand a return on that investment. As we pointed out in Chapter 10, a business that breaks even in terms of accounting profits is really making a loss; it is failing to cover the cost of capital.

To judge the net contribution to value, we need to deduct the cost of capital contributed to the plant by the parent company and its stockholders. Suppose again that the cost of capital is 10%. Then the dollar cost of capital for the Quayle City plant is .10 X $1,000 = $100 million.

The net gain is therefore $150 – 100 = $50 million. This is the addition to shareholder wealth due to management’s hard work (or good luck).

Net income after deducting the dollar return required by investors is called residual income or economic value added (EVA). The formula is

EVA = residual income = income earned – income required = income earned – cost of capital X investment

For our example, the calculation is

EVA = residual income = 150 – (.10 X 1,000) = +$50 million

But if the cost of capital were 20%, EVA would be negative by $50 million.

Net return on investment and EVA are focusing on the same question. When return on investment equals the cost of capital, net return and EVA are both zero. But the net return is a percentage and ignores the scale of the company. EVA recognizes the amount of capital employed and the number of dollars of additional wealth created.

EVA sometimes pops up with different labels. Other consulting firms have their own versions of residual income. McKinsey & Company uses economic profit (EP), defined as capital invested multiplied by the spread between return on investment and the cost of capital. This is another way to measure residual income. For the Quayle City plant, with a 10% cost of capital, economic profit is the same as EVA:

In Chapter 28, we take a look at EVAs calculated for some well-known companies. But EVA’s most valuable contributions happen inside companies. EVA encourages managers and employees to concentrate on increasing value, not just on increasing earnings.

2. Pros and Cons of EVA

Let us start with the pros. EVA, economic profit, and other residual income measures are clearly better than earnings or earnings growth for measuring performance. A plant that is generating lots of EVA should generate accolades for its managers as well as value for shareholders. EVA may also highlight parts of the business that are not performing up to scratch. If a division is failing to earn a positive EVA, its management is likely to face some pointed questions about whether the division’s assets could be better employed elsewhere.

EVA sends a message to managers: Invest if and only if the increase in earnings is enough to cover the cost of capital. This is an easy message to grasp. Therefore, EVA can be used down deep in the organization as an incentive compensation system. It is a substitute for explicit monitoring by top management. Instead of telling plant and divisional managers not to waste capital and then trying to figure out whether they are complying, EVA rewards them for careful investment decisions. Of course, if you tie junior managers’ compensation to their economic value added, you must also give them power over those decisions that affect EVA. Thus, the use of EVA implies delegated decision making.

EVA makes the cost of capital visible to operating managers. A plant manager can improve EVA by (1) increasing earnings or (2) reducing capital employed. Therefore, underutilized assets tend to be flushed out and disposed of.

Introduction of residual income measures often leads to surprising reductions in assets employed—not from one or two big capital disinvestment decisions, but from many small ones. Ehrbar quotes a sewing machine operator at Herman Miller Corporation:

[EVA] lets you realize that even assets have a cost. . . . We used to have these stacks of fabric sitting here on the tables until we needed them. . . . We were going to use the fabric anyway, so who cares that we’re buying it and stacking it up there? Now no one has excess fabric. They only have the stuff we’re working on today. And it’s changed the way we connect with suppliers, and we’re having [them] deliver fabric more often.25

If you propose to tie a manager’s remuneration to her business’s profitability, it is clearly better to use EVA than accounting income, which takes no account of the cost of the capital employed. But what are the limitations of EVA? Here we return to the same question that bedevils stock-based measures of performance. How can you judge whether a low EVA is a consequence of bad management or of factors outside the manager’s control? The deeper you go in the organization, the less independence that managers have and therefore the greater the problem in measuring their contribution.

The second limitation with any accounting measure of performance lies in the data on which it is based. We explore this issue in the next section.

I’ve recently started a website, the information you provide on this website has helped me tremendously. Thanks for all of your time & work.