To illustrate the principles of option valuation, we focused on the example of Amazon’s options. But financial managers turn to the Black-Scholes model to estimate the value of a variety of different options. Here are four examples.

1. Executive Stock Options

In fiscal year 2017, Larry Ellison, the CEO of Oracle Corporation, received a salary of $1, but he also pocketed $21 million in the form of options and other stock-related awards.

Executive stock options are often an important part of compensation. For many years, companies were able to avoid reporting the cost of these options in their annual statements. However, they must now treat options as an expense just like salaries and wages, so they need to estimate the value of all new options that they have granted. For example, Oracle’s financial statements show that in fiscal 2017, the company issued a total of 18 million options with an average life of 4.8 years. Oracle calculated that the average value of these options was $8.18. How did it come up with this figure? It just used the Black-Scholes model assuming a standard deviation of 23%.[1]

Some companies have disguised how much their management is paid by backdating the grant of an option. Suppose, for example, that a firm’s stock price has risen from $20 to $40. At that point, the firm awards its CEO options exercisable at $20. That is generous but not illegal. However, if the firm pretends that the options were actually awarded when the stock price was $20 and values them on that basis, it will substantially understate the CEO’s com- pensation.[2] The Beyond the Page app discusses the backdating scandal.

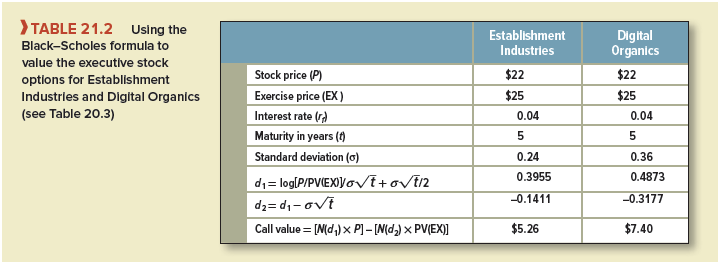

Speaking of executive stock options, we can now use the Black-Scholes formula to value the option packages you were offered in Section 20-3 (see Table 20.3). Table 21.2 calculates the value of the options from the safe-and-stodgy Establishment Industries at $5.26 each. The options from risky-and-glamorous Digital Organics are worth $7.40 each. Congratulations.

2. Warrants

When Owens Corning emerged from bankruptcy in 2006, the debtholders became the sole owners of the company. But the old stockholders were not left entirely empty-handed. They were given warrants to buy the new common stock at any point in the next seven years for $45.25 a share. Because the stock in the restructured firm was worth about $30 a share, the stock needed to appreciate by 50% before the warrants would be worth exercising. However, this option to buy Owens Corning stock was clearly valuable, and shortly after the warrants started trading, they were selling for $6 each. You can be sure that before shareholders were handed this bone, all the parties calculated the value of the warrants under different assumptions about the stock’s volatility. The Black-Scholes model is tailor-made for this purpose.

3. Portfolio Insurance

Your company’s pension fund owns an $800 million diversified portfolio of common stocks that moves closely in line with the market index. The pension fund is currently fully funded, but you are concerned that if it falls by more than 20%, it will start to be underfunded. Suppose that your bank offers to insure you for one year against this possibility. What would you be prepared to pay for this insurance? Think back to Section 20-2 (Figure 20.5), where we showed that you can shield against a fall in asset prices by buying a protective put option. In the present case, the bank would be selling you a one-year put option on U.S. stock prices with an exercise price 20% below their current level. You can get the value of that option in two steps. First use the Black-Scholes formula to value a call with the same exercise price and maturity. Then back out the put value from put-call parity. (You may have to adjust for dividends, but we’ll leave that to the next section.)

4. Calculating Implied Volatilities

So far, we have used our option pricing model to calculate the value of an option given the standard deviation of the asset’s returns. Sometimes it is useful to turn the problem around and ask what the option price is telling us about the asset’s volatility. For example, the Chicago Board Options Exchange trades options on several market indexes. As we write this, the Standard and Poor’s 500 Index is about 2375, while a seven-month at-the-money call on the index is priced at 89. If the Black-Scholes formula is correct, then an option value of 89 makes sense only if investors believe that the standard deviation of index returns is about 11.4% a year.[3]

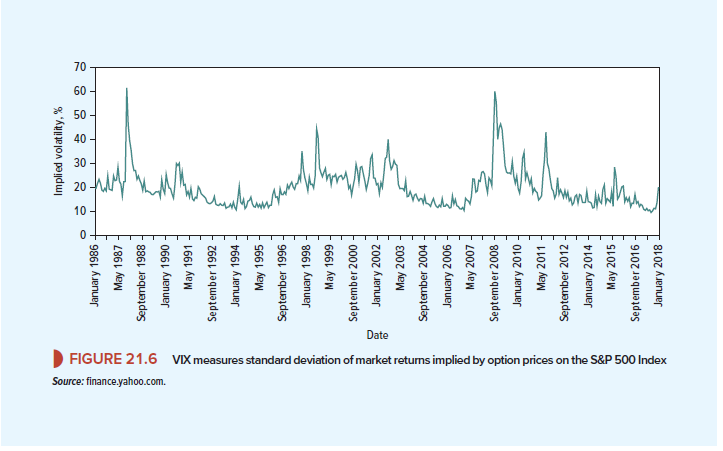

The Chicago Board Options Exchange regularly publishes the implied volatility on the Standard and Poor’s index, which it terms the VIX (see the nearby box on the “fear index”). There is an active market in the VIX. For example, suppose you feel that the implied volatility is implausibly low. Then you can “buy” the VIX at the current low price and hope to “sell” it at a profit when implied volatility has increased.

You may be interested to compare the current implied volatility that we calculated earlier with Figure 21.6, which shows past measures of implied volatility for the Standard and Poor’s index and for the Nasdaq index (VXN). Notice the sharp increase in investor uncertainty at the height of the credit crunch in 2008. This uncertainty showed up in the price that investors were prepared to pay for options.

I believe this site has some very wonderful information for everyone : D.