Dow always ignored a movement of one average which was not confirmed by the other, and experience since his death has shown the wisdom of that method of checking the reading of the averages. His theory was that a downward movement of secondary, and perhaps ultimately primary importance, was established when the new lows for both averages were under the low points of the preceding reaction. (June 25, 1928, in Rhea, 1932; pg. 238)

In line with the economic rationale for the use of the industrial and railroad averages as proxies for the economy and state of business, Dow Theory introduced a concept that also is important today, namely the concept of confirmation. Confirmation has taken new directions, which this book covers later, but in Rhea’s time, confirmation was the consideration of the industrial and railroad averages together. “Conclusions based upon the movement of one average, unconfirmed by the other, are almost certain to prove misleading” (Rhea.. 1932).

Confirmation in the Dow Theory comes when both the industrial and railroad averages reach new highs or new lows together on a daily closing basis. These new levels do not necessarily have to be reached at exactly the same time, but for a primary reversal, it is necessary that each average reverses direction and reaches new levels before the primary reversal can be recognized (see Figure 6.3). Confirmation, therefore, is the necessary means for recognizing in what direction the primary trend is headed. Failure to reach new levels during a secondary reaction is a warning that the primary trend may be reversing. For example, when there is a primary bull market, the failure of the averages to reach new highs during a secondary advance alerts the analyst that the primary trend may be reversing to a bear market. These are called nonconfirmations. In addition, if lower levels are reached during the secondary bear trend, it is an indication that the primary trend has changed from an upward bull trend to a downward bear trend. Thus, more extreme levels occurring during a secondary retracement in the opposite direction of the primary trend are evidence that the primary trend has changed direction. When confirmed by the other average, the technical analyst then has proof that the primary trend has reversed and can act accordingly.

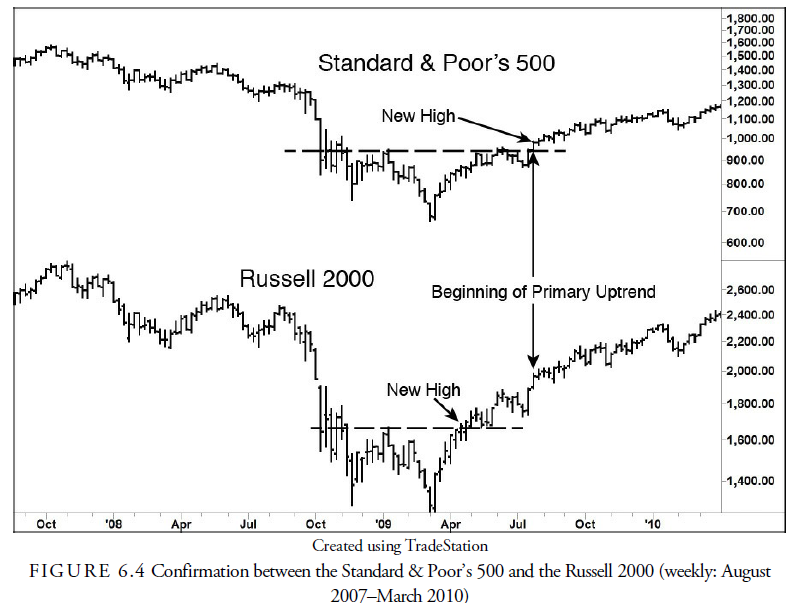

Today, because the makeup of the economy is so different than in Dow’s and Hamilton’s time, with the advent of a wider base of industrial stocks and technology stocks, the usual method of confirming a primary trend is to use confirmation between the two indexes: Standard & Poor’s 500 and the Russell 2000. The economic rationale is that the Standard & Poor’s 500 represents the largest, most highly capitalized companies in the United States, and the Russell 2000 represents smaller companies with higher growth and usually a technological base. When these two indexes confirm each other, the primary trend is confirmed. Figure 6.4 shows the more modern application of Dow’s theory of confirmation.

Importance of Volume

Various meanings are ascribed to reductions in the volume of trading. One of the platitudes most constantly quoted in Wall Street is to the effect that one should never sell a dull market short. That advice is probably right oftener than it is wrong, but it is always wrong in an extended bear swing. In such a swing… the tendency is to become dull on rallies and active on declines. (Hamilton, May 21, 1909, as quoted in Rhea, 1932)

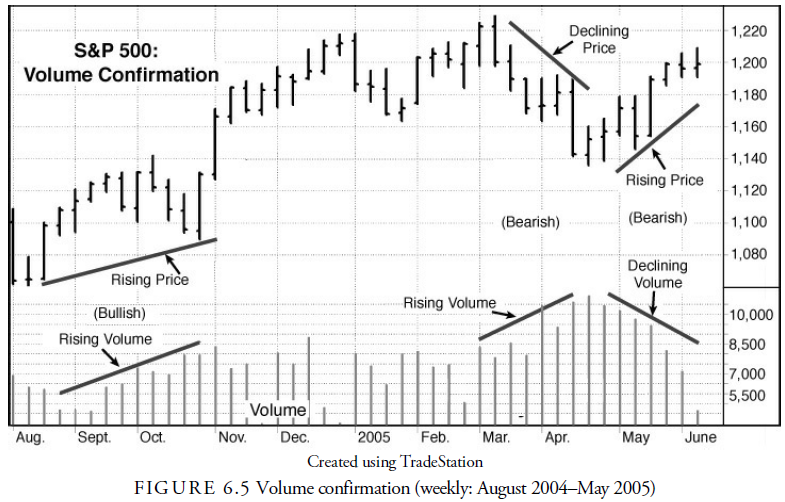

Although volume of transactions cannot signal a trend reversal, it is important as a secondary confirmation of trend. Excessively high market prices that are accompanied by less volume on rallies and more activity on declines usually suggest an overbought market (see Figure 6.5). Conversely, extremely low prices with dull declines and increased volume on rallies suggest an oversold market. “Bull markets terminate in a period of excessive activity and begin with comparatively light transactions” (Rhea, 1932).

The originators of Dow Theory were quick, however, not to overstate the importance of volume. Although volume was considered, it was not a primary consideration. Price trend and confirmation overrode any consideration of volume.

The volume is much less significant than is generally supposed. It is purely relative, and what would be a large volume in one state of the market supply might well be negligible in a greatly active market. (Hamilton, 1922, p. 177)

Source: Kirkpatrick II Charles D., Dahlquist Julie R. (2015), Technical Analysis: The Complete Resource for Financial Market Technicians, FT Press; 3rd edition.

I really appreciate this post. I?¦ve been looking all over for this! Thank goodness I found it on Bing. You’ve made my day! Thank you again