The Eximbank was created in 1934 and established under its present law in 1945, with the aim of assisting in the financing of U.S. export trade. It was originally established to finance exports to Europe after World War II. Eximbank’s role in promoting U.S. exports is likely to be more significant now than in the past few decades because (1) the U.S. economy is more internationalized, and exports constitute a growing share of the GNP, and (2) there has been a substantial increase in the volume of international trade, and competition for export markets is quite intense.

Eximbank is intended to supplement but not compete with private capital. It has historically been active in areas in which the private sector has been reluctant to provide export financing. Eximbank has three main functions: (1) provide guarantees and export credit insurance so that exporters and their bankers give credit to foreign buyers; (2) provide competitive financing to foreign buyers; and (3) negotiate with other countries to reduce the level of subsidy in export credits (U.S. Export-Import Bank, 2012).

Over the past few years, Eximbank has focused on a broad range of critical areas, such as provision of greater support to small businesses, promotion of exports to developing nations, and promotion of exports of environmentally beneficial goods and services. It has also been engaged in expanding project finance capabilities as well as in reducing trade subsidies of other governments through bilateral or multilateral negotiations.

In its more than seventy years of operations, the Bank has supported more than $550 billion of U.S. exports (U.S. Export-Import Bank, 2012a). It has assisted U.S. exporters to win export sales in many countries and undertakes risks the private sector is unwilling or unable to take. The Bank also attempts to neutralize financing provided by foreign governments to their exporters when they are in competition for export sales with U.S. exporters. However, the Bank does require reasonable assurance of repayment for the transactions it authorizes and closely monitors credit and other risks in its portfolio.

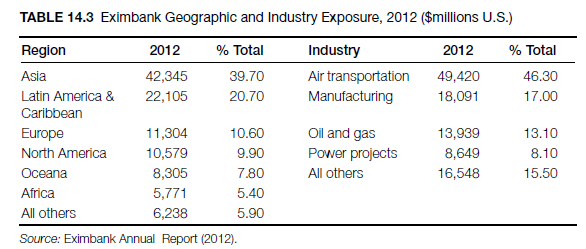

Annual authorizations have ranged from $14 billion (2008) to $36 billion in 2012 (see Tables 14.3 and 14.4). The largest share of the Bank portfolio involves financing infrastructure projects such as transportation, power generation, oil and gas production, and mining. The highest geographic exposure is in Asia, with almost 40 percent of the total. Eximbank also has enhanced financing available for certain categories of exports: environmentally beneficial goods and services, medical equipment, and transportation security equipment.

The Bank provides assistance to U.S. exporters of goods and/or services provided the exports include a minimum of 50 percent U.S. (local) content and are not military related. Its financing decision is based, inter alia, upon an assessment of the borrower’s capability to repay the loan. There are four major export financing programs provided by Eximbank (U.S. Export-Import Bank, 2012a; Reynolds, 2003):

- Working capital loan guarantees for U.S. exporters

- Credit insurance

- Guarantees of commercial loans to foreign buyers

- Direct loans to foreign purchasers.

U.S. government support for the Bank has been the subject of criticism from various groups:

- The environmental community contends that the Bank provides loans and loan guarantees for projects that harm the environment. These groups raise concerns about the harmful effects of an Eximbank-assisted oil drilling and pipeline project in Chad and Cameroon, a coal-fired power plant in Indonesia, and the loan guarantees for the sale of nuclear fuel to the Czech Republic.

- It is often stated that the Bank’s assistance is largely provided to a small number of large U.S. firms such as Boeing, Bechtel, GE, and Halliburton, as well as to countries that do not need financial support in the form of loans, loan guarantees, or insurance. In view of the fact that Eximbank supports about 1 percent of U.S. exports, critics suggest that it has a marginal impact on overall U.S. exports or its trade balance.

- Some of Eximbank’s loans to foreign companies have contributed to harm to domestic industries. It is alleged that the $18 million loan to the Chinese iron and steel industry, for example, adversely affected the competitiveness of local industries (U.S. Export- Import Bank, 2012d)Working Capital Guarantee Program.

1. Working Capital Guarantee Program

The availability of adequate working capital is critical for the maintenance and expansion of a viable export-import business. Banks are often reluctant to make financing available because the businesses either have reached the borrowing limits set by their banks or do not have the necessary collateral. The working capital guarantee program is intended to encourage commercial lenders to make loans for various exports-related activities (see Figure 14.1). Such loans may be used for the purchase of raw materials and finished products for export, to pay for overhead, or to cover standby letters of credit, such as bid bonds, performance bonds, or payment guarantees (U.S. Export-Import Bank, 2012c).

Exporters may apply to the Eximbank for a preliminary commitment for a guarantee. The lender also may apply directly for a final authorization. In the case of preliminary commitment, the Eximbank will outline the general terms and conditions under which it will provide the guarantee to the exporter, and this can be used to approach various lenders to secure the most attractive loan package.

The lender must apply for the final commitment. An exporter may also apply through a lender that has been granted a guarantee by the Eximbank. Such lenders have been granted preapproved credit authority (delegated authority) to process working capital loans under established criteria without preapproval from Eximbank. For small-business exporters, the Small Business Administration (SBA) can guarantee a working capital loan up to $1.1 million or up to $2.0 million under a co-guaranty agreement with the Eximbank. Guarantees may be approved for a single loan or for a revolving line of credit.

The major features of the working capital guarantee program are as follows:

Qualified Exports

Eligible exports must be shipped from the United States and have at least 50 percent U.S. content. If the export has less than 50 percent U.S. content, the bank will support only up to the percentage of the U.S. content. Military items as well as sales to military buyers are generally not eligible.

Guarantee Coverage and Term of the Loan

In the event of default by the exporter, Eximbank will cover 90 percent of the principal of the loan and interest, up to the date of claim for payment, provided the lender has met all the terms and conditions of the guarantee agreement. Guaranteed loans generally have maturities of twelve months and are renewable.

Collateral and Borrowing Capacity

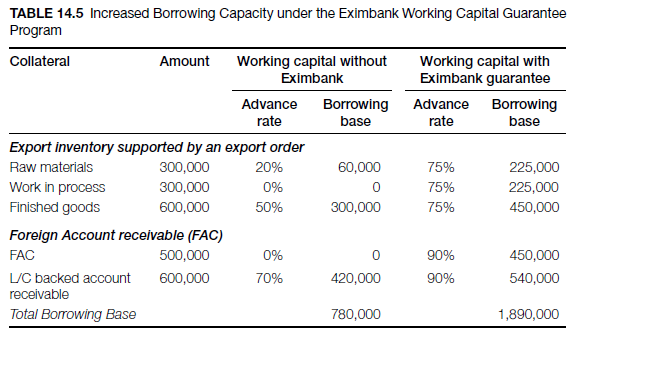

Guaranteed loans are to be secured by a collateral. Acceptable collateral may include export- related inventory, export-related accounts receivables, or other assets. Inventory and accounts receivable include goods purchased or sales generated by use of the guaranteed loan. For service companies, costs such as engineering, design, or allocable overhead may be treated as collateral. In the case of letters of credit issued under the guaranteed loan, collateral is required for only 25 percent of the value of the letter of credit.

Exporters can borrow up to 75 percent of their inventory, including work-in-process, and up to 90 percent of their foreign account receivable, thus increasing their borrowing capacity. Table 14.5 illustrates borrowing capacity with and without the working capital facility.

Qualified Exporters and Lenders

Exporters must be domiciled in the United States (regardless of domestic/foreign ownership requirements), show a successful track record of past performance, including an operating history of at least one year, and have a positive net worth. Financial statements must show sufficient strength to accommodate the requested debt.

Any public or private lender may apply under the program. Eligibility is determined on the basis of many factors, including the lender’s financial condition, knowledge of trade finance, and ability to manage asset-based loans. Lenders may be approved as priority lenders or delegated authority lenders. Approved lenders under the priority lender program submit final commitment applications to Eximbank and receive a decision within ten business days. The lender, prior to submission to Eximbank, must approve the loan application. However, approved delegated authority lenders are allowed to approve loans and receive a guarantee from Eximbank without having to submit individual applications for approval.

Example: In 2011, Eximbank approved a request from Geothermal Development Associates (GDA) to support the sale of geothermal equipment to Kenya. GDA needed working capital to fulfill the order, and World Trade Finance provided an Eximbank-guaranteed loan to GDA.

2. Export Credit Insurance Program (ECIP)

The purpose of the ECIP is to promote U.S. sales abroad by protecting exporters against loss in the event of default by a foreign buyer or debt arising from commercial or political risks. The policy also enables exporters to obtain financing more easily because, with prior Eximbank approval, the proceeds of the policy can be readily assigned to a financial institution as collateral. Eximbank offers a wide range of policies to accommodate many different insurance needs of exporters and financial institutions. For example, insurance policies may apply to shipments to one buyer or many buyers, cover short-term (180 days or less) or intermediate-term (generally one to five years) credit, and provide comprehensive coverage for commercial as well as specific or all political risks. There are also policies specifically geared to small businesses that are beginning to export their goods or services (Small Business Policies). Some export credit insurance policies include the following:

- Exporter policies (short-term): single-buyer/multibuyer policies, small business policies;

- Lender policies (short-term): letter-of-credit policies, financial institution buyer/supplier credit policies;

- Policies for exporters and lenders: documentary and nondocumentary policies;

- Other policies: includes leasing policies for operating and finance leases.

The policies insure both the stream of lease payments and the fair market value of the leased product (Table 14.6 and Figure 14.2).

Examples: In April 2012, Eximbank announced a three-year renewal of the Bank’s Short-Term Africa Initiative (STAI), which provides export-credit insurance for U.S. exporters selling to eighteen countries in sub-Saharan Africa, up to a program limit of $100 million. The initiative is renewed through March 31, 2015. Currently, Eximbank’s insurance on all short-term STAI country transactions is available only under the Bank’s single-buyer insurance policy, which is a select-risk authorization. Existing Eximbank multi-buyer policyholders with a diverse spread of country and buyer risk are also eligible but must submit separate single-buyer policy applications for each STAI country buyer.

In October 2012, Eximbank renewed a twelve-month export credit insurance policy for Wells Fargo to enable the export of American cotton to a large textile firm in Turkey. The instrument renewed in this transaction was a Financial Institution Buyer Credit (FIBC), allowing Wells Fargo Bank to extend revolving credit to the Turkish textile manufacturer so that it can import American cotton.

3. Guarantees

Eximbank guarantees provide repayment protection for private-sector loans to creditworthy buyers of U.S. exports (see Figure 14.3). The program covers 100 percent of the commercial and political risks (85 percent of the U.S. contract amount). The foreign buyer is required to make at least a 15 percent cash payment. Exports supported under this program are capital equipment, services, and projects, and the loan guarantees are offered for intermediate- and long-term sales. Guarantees of $20 million or less do not require shipment on U.S.-registered vessels. The credit may be for any amount. The guarantee is unconditional and transferable.

Example: In May 2012, Eximbank approved a guarantee of a $350 million loan facility to provide the funds to assist Textron Inc. in financing exports by two of its companies, Cessna Aircraft Company and Bell Helicopter Textron. The guaranteed lender is PNC Bank in Pittsburgh, Pennsylvania. The Eximbank- guaranteed loan facility will enable Textron’s finance segment to provide financing to international customers that take delivery of new Cessna aircraft and Bell commercial helicopters. The repayment term is twelve years.

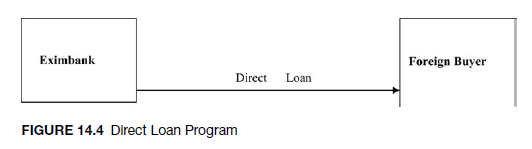

4. Direct Loans Program

Under this program, Eximbank provides fixed-rate loans directly to creditworthy foreign buyers for the purchase of U.S. capital equipment, projects, and related services. The loan covers up to 85 percent of the U.S. export value. The buyer is, however, required to make a cash payment for the difference, that is, 15 percent of the value. The loan is often used by buyers when the financed portion exceeds $10 million (Figure 14.4). A loan agreement as well as shipment on U.S. registered vessels is required. The program supports intermediate- and long-term sales. Transactions normally range from five to ten years, depending on the export value, the product, the importing country, and the terms offered by the competition.

All direct loans are subject to U.S.-flag shipping requirements. There is no limit on transaction size.

Example: In December 2012, Eximbank approved a $1.03 billion loan to Global- foundries to finance the export of American-made semiconductor manufacturing equipment to Germany. Eximbank’s credit will support the expansion of the Globalfoundries silicon-wafer-fabrication facility in Dresden, Germany.

Source: Seyoum Belay (2014), Export-import theory, practices, and procedures, Routledge; 3rd edition.

Would love to perpetually get updated outstanding weblog! .

Keep up the great piece of work, I read few blog posts on this internet site and I believe that your weblog is rattling interesting and contains circles of fantastic information.