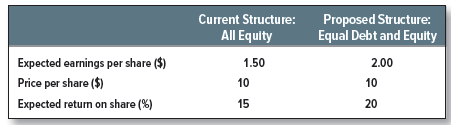

Consider now the implications of MM’s proposition 1 for the expected returns on Macbeth stock:

Leverage increases the expected stream of earnings per share but not the share price. The reason is that the change in the expected earnings stream is exactly offset by a change in the rate at which the earnings are discounted. The expected return on the share (which for a perpetuity is equal to the earnings-price ratio) increases from 15% to 20%. We now show how this comes about.

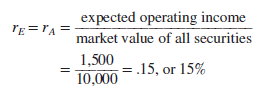

The expected return on Macbeth’s assets rA is equal to the expected operating income divided by the total market value of the firm’s securities:

![]()

We have seen that in perfect capital markets the company’s borrowing decision does not affect either the firm’s operating income or the total market value of its securities. Therefore, the borrowing decision also does not affect the expected return on the firm’s assets rA.

Suppose that an investor holds all of a company’s debt and all of its equity. This investor is entitled to all the firm’s operating income; therefore, the expected return on the portfolio is just rA.

The expected return on a portfolio is equal to a weighted average of the expected returns on the individual holdings. Therefore, the expected return on a portfolio consisting of all the firm’s securities is

This formula is, of course, an old friend from Chapter 9. The overall expected return rA is called the company cost of capital or the weighted-average cost of capital (WACC).

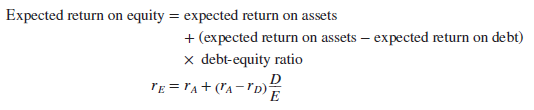

We can turn the formula around to solve for rE, the expected return to equity for a levered firm:

1. Proposition 2

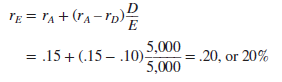

This is MM’s proposition 2: The expected rate of return on the common stock of a levered firm increases in proportion to the debt-equity ratio (D/E), expressed in market values; the rate of increase depends on the spread between rA, the expected rate of return on a portfolio of all the firm’s securities, and rD, the expected return on the debt. Note that rE = rA if the firm has no debt. We can check out this formula for Macbeth Spot Removers. Before the decision to borrow

If the firm goes ahead with its plan to borrow, the expected return on assets rA is still 15%, but the expected return on equity is

When the firm was unlevered, equity investors demanded a return of rA. When the firm is levered, they require a premium of (rA – rD)D/E to compensate for the extra risk.

MM’s proposition 1 says that financial leverage has no effect on shareholders’ wealth. Proposition 2 says that the rate of return they can expect to receive on their shares increases as the firm’s debt-equity ratio increases. How can shareholders be indifferent to increased leverage when it increases expected return? The answer is that any increase in expected return is exactly offset by an increase in financial risk and therefore in shareholders’ required rate of return.

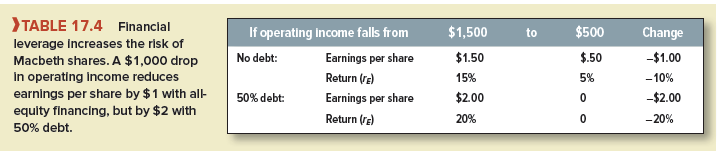

You can see financial risk at work in our Macbeth example. Compare the risk of earnings per share in Table 17.2 versus Table 17.1. Or look at Table 17.4, which shows how a shortfall in operating income affects the payoff to the shareholders. If the firm is all-equity-financed, a decline of $1,000 in the operating income reduces the return on the shares by 10 percentage points. If the firm issues risk-free debt with a fixed interest payment of $500 a year, then a decline of $1,000 in the operating income reduces the return on the shares by 20 percentage points. In other words, the effect of the proposed leverage is to double the amplitude of the swings in Macbeth’s shares. Whatever the beta of the firm’s shares before the refinancing, it would be twice as high afterward.

Now you can see why investors require higher returns on levered equity. The required return simply rises to match the increased financial risk.

2. Leverage and the Cost of Equity

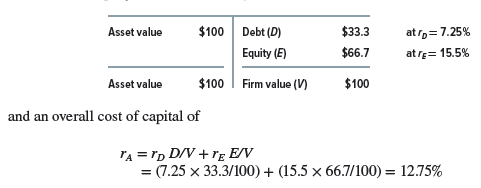

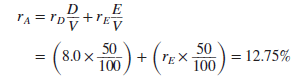

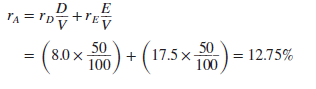

Consider a company with the following market-value balance sheet:

If the firm is considering a project that has the same risk as the firm’s existing business, the appropriate discount rate for the cash flows is 12.75%, the firm’s cost of capital.

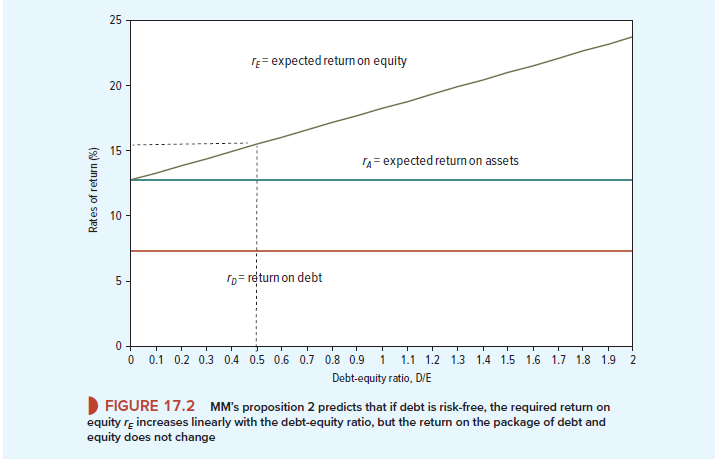

Suppose the firm changes its capital structure by issuing more debt and using the proceeds to repurchase stock. The implications of MM’s Proposition 2 are shown in Figure 17.2. The required return on equity increases with the debt-equity ratio (D/E).[1] Yet, no matter how much the firm borrows, the required return on the package of debt and equity, rA, remains constant at 12.75%. How is it possible for the required return on the package to stay constant when the required return on the individual securities is changing? Answer: Because the proportions of debt and equity in the package are also changing. More debt means that the cost of equity increases but at the same time the proportion of equity declines.

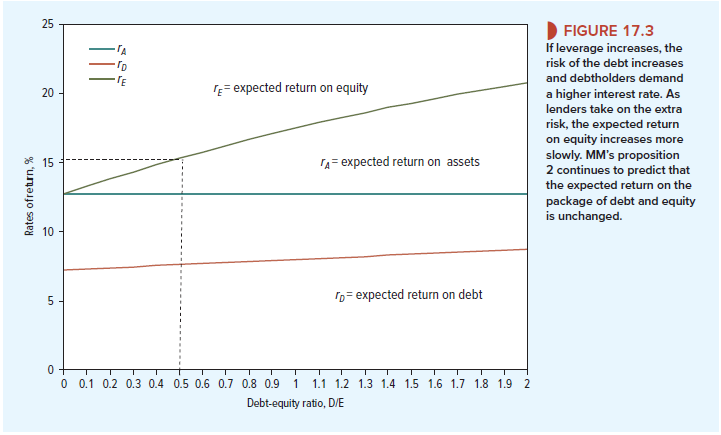

In Figure 17.2, we have drawn the rate of interest on the debt as constant no matter how much the firm borrows. This is not wholly realistic. It is true that most large, conservative companies could borrow a little more or less without noticeably affecting the interest rate that they pay. But at higher debt levels, lenders become concerned that they may not get their money back, and they demand higher rates of interest to compensate. Figure 17.3 modifies Figure 17.2 to account for this. You can see that as the firm borrows more, the risk of the debt slowly increases. Proposition 2 continues to predict that the expected return on the package of debt and equity does not change. However, the slope of the rE line now tapers off as D/E increases. Why? Essentially because holders of risky debt begin to bear part of the firm’s operating risk. As the firm borrows more, more of that risk is transferred from stockholders to bondholders.

Let’s assume that the firm issues an additional $16.7 of debt and uses the cash to repurchase $16.7 of its equity. The revised market-value balance sheet has debt of $50 rather than $33.3:

The change in financial structure does not affect the amount or risk of the cash flows on the total package of debt and equity. Therefore, if investors required a return of 12.75% on the total package before the refinancing, they must require a 12.75% return on the firm’s assets afterward.

Although the required return on the package of debt and equity is unaffected, the change in financial structure does affect the required return on the individual securities. Because the company has more debt than before, the debtholders are likely to demand a higher interest rate. Suppose that the expected return on the debt rises to 8%. Now you can write down the basic equation for the return on assets:

Increasing the amount of debt increased debtholder risk and led to a rise in the return that debtholders required (rD rose from 7.25% to 8.0%). The higher leverage also made the equity riskier and increased the return that shareholders required (rE rose from 15.5% to 17.5%). However, the weighted-average return on debt and equity was unchanged at 12.75%:

Suppose that the company decided instead to repay all its debt and to replace it with equity. In that case, all the cash flows would go to the equityholders. The company cost of capital, rA, would stay at 12.75%, and rE would also be 12.75%.

3. How Changing Capital Structure Affects Beta

We have looked at how changes in financial structure affect expected return. Let us now look at the effect on beta.

The stockholders and debtholders both receive a share of the firm’s cash flows, and both bear part of the risk. For example, if the firm’s assets turn out to be worthless, there will be no cash to pay stockholders or debtholders. But debtholders usually bear much less risk than stockholders. Debt betas of large firms are typically in the range of 0 to .2.[2]

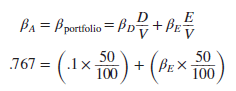

If you owned a portfolio of all the firm’s securities, you wouldn’t share the cash flows with anyone. You wouldn’t share the risks with anyone either; you would bear them all. Thus, the firm’s asset beta is equal to the beta of a portfolio of all the firm’s debt and its equity.

The beta of this hypothetical portfolio is just a weighted average of the debt and equity betas:

![]()

Think back to our example. If the debt before the refinancing has a beta of .1 and the equity has a beta of 1.1, then

![]()

What happens after the refinancing? The risk of the total package is unaffected, but both the debt and the equity are now more risky. Suppose that the debt beta stays at .1. We can work out the new equity beta:

Solve for the formula for pE. You will see that it parallels MM’s proposition 2 exactly:

![]()

Our example shows how borrowing creates financial leverage or gearing. Financial leverage does not affect the risk or the expected return on the firm’s assets, but it does push up the risk of the common stock. Shareholders demand a correspondingly higher return because of this financial risk.

You can use our formulas to unlever betas—that is, to go from an observed pE to pA. You have the equity beta of 1.43. You also need the debt beta, here .1, and the relative market values of debt (D/V) and equity (E/V). If debt accounts for 50% of overall value V, then the unlevered beta is

![]()

This runs the previous example in reverse. Just remember the basic relationship:

![]()

4. Watch Out for Hidden Leverage

MM did not say that borrowing is a bad thing. But they insisted that financial managers stay on the lookout for the financial risk created by borrowing. That risk can be especially dangerous when the borrowing is not in plain sight. For example, most long-term leases are debt-equivalent obligations, so leases can hide debt. Long-term contracts with suppliers can also be debts in disguise when prices and quantities are fixed. For many firms pension liabilities and liabilities for employees’ post-retirement health care are massive off-balance-sheet, debt-equivalent obligations.

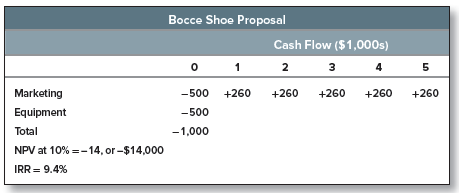

EXAMPLE 17.2 ● Reeby Sports’ Bocce Project

Here is an example of how hidden leverage can fool a company into poor decisions. Reeby Sports is considering launch of a carbon-fiber Bocce shoe. The product will require investment of $500,000 in up-front marketing expenses and $500,000 for new equipment. George Reeby prepares a simple spreadsheet for the new product’s expected five-year life and discounts at Reeby Sports’ normal 10% cost of capital.[3]

George notes the negative NPV, then calls the equipment salesperson to cancel Reeby Sports’ order. The salesperson, anxious to keep her sale, offers to let Reeby Sports buy the equipment now and pay later. She asks whether George will commit to five fixed payments of $122,000 per year. She argues that this will reduce the up-front investment and improve profitability. George revises his spreadsheet:

Now George is inclined to go ahead—the NPV and IRR look much better—but Jenny, his investment-banker daughter, points out that the manufacturer is really just lending $500,000 to Reeby Sports at the same 7% interest rate that Reeby Sports would pay to a bank. She explains that the manufacturer would advance $500,000 now in exchange for later fixed payments totaling 5 X 122,000 = $610,000 undiscounted. The payments are obligatory, just like debt service on a bank loan. The effective interest rate is 7%. (You can check that the IRR to the manufacturer from agreeing to payment by installments is 7%.)

Jenny chides her father for mixing up investment and financing decisions. She upbraids him for forgetting about the financial risk created by a debt-financed equipment purchase. She berates him for discounting the cash flows of $138,000 per year (after installment payments) at the 10% cost of capital, which is designed to value unlevered cash flows.“Go back to your first spreadsheet, Dad,” she instructs.8 George, fearing chastisement, reproach, and remonstra- tion, agrees.

The hidden leverage in this example is, of course, only thinly disguised. The leverage would be harder to see if, for example, it were wrapped up in a financial lease transaction. See Chapter 25 and the mini-case at the end of this chapter.

I definitely knew about most of this, but having said that, I still found it helpful. Nice work!

Lovely site! I am loving it!! Will be back later to read some more. I am bookmarking your feeds also.