Financial ratios are usually easy to calculate. That’s the good news. The bad news is that there are so many of them. To make it worse, the ratios are often presented in long lists that seem to require memorization rather than understanding.

We can mitigate the bad news by taking a moment to preview what the ratios are measuring and how they connect to the ultimate objective of value added for shareholders.

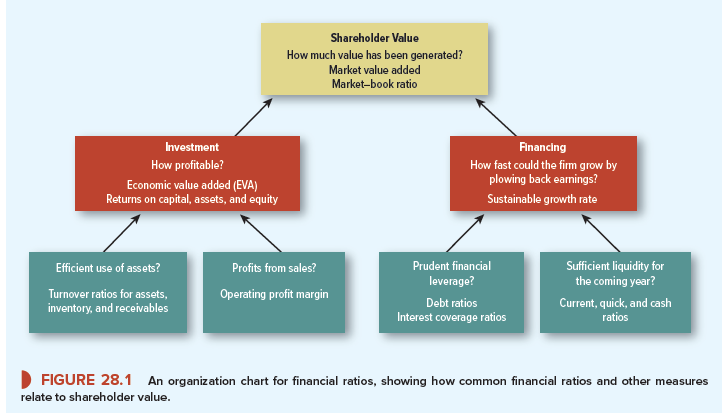

Shareholder value depends on good investment decisions. The financial manager evaluates investment decisions by asking several questions, including these: How profitable are the investments relative to the cost of capital? How should profitability be measured? What does profitability depend on? (We will see that it depends on efficient use of assets and on the profits on each dollar of sales.)

Shareholder value also depends on good financing decisions. Again, there are obvious questions: Is the available financing sufficient? The firm cannot grow unless financing is available. Is the financing strategy prudent? The financial manager should not put the firm’s assets and operations at risk by operating at a dangerously high debt ratio. Does the firm have sufficient liquidity (a cushion of cash or assets that can be readily sold for cash)? The firm has to be able to pay its bills and respond to unexpected setbacks.

Figure 28.1 summarizes these questions in more detail. The boxes on the left are for investment, those on the right for financing. In each box, we have posed a question and given examples of financial ratios or other measures that can help to answer it. For example, the bottom box on the far left asks about efficient use of assets. Three ratios that measure asset efficiency are turnover ratios for assets, inventory, and accounts receivable. The two bottom boxes on the right ask whether financial leverage is prudent and whether the firm has sufficient liquidity for the coming year. The ratios for tracking financial leverage include various debt ratios; the ratios for liquidity are the current, quick, and cash ratios.

Figure 28.1 serves as a road map for this chapter. We will show how to calculate these and other common financial ratios and explain how they relate to the objective of shareholder value.

Fantastic beat ! I would like to apprentice while you amend your site, how could i subscribe for a blog website?

The account aided me a applicable deal. I had been a

little bit familiar of this your broadcast offered shiny

transparent concept

wonderful publish, very informative. I ponder why the opposite specialists of this sector don’t notice this.

You must continue your writing. I am confident, you’ve a huge readers’ base already!

Tremendous things here. I am very glad to see your post.

Thank you so much and I’m having a look ahead to contact

you. Will you kindly drop me a mail?

As I website owner I conceive the written content here is rattling great, thanks for your efforts.