1. Shareholders Want Managers to Maximize Market Value

Major corporations may have hundreds of thousands of shareholders. There is no way that these shareholders can be actively involved in management; it would be like trying to run New York City by town meetings. Authority has to be delegated to professional managers. But how can the company’s managers make decisions that satisfy all the shareholders? No two shareholders are exactly the same. Some may plan to cash in their investments next year; others may be investing for a distant old age. Some may be wary of taking much risk; others may be more venturesome. Delegating the operation of the firm to professional managers can work only if these shareholders have a common objective. Fortunately, there is a natural financial objective on which almost all shareholders agree: Maximize the current market value of shareholders’ investment in the firm.

A smart and effective manager makes decisions that increase the current value of the company’s shares and the wealth of its stockholders. This increased wealth can then be put to whatever purposes the shareholders want. They can give their money to charity or spend it in glitzy nightclubs; they can save it or spend it now. Whatever their personal tastes or objectives, they can all do more when their shares are worth more.

Maximizing shareholder wealth is a sensible goal when the shareholders have access to well-functioning financial markets.[1] Financial markets allow them to adjust risks and transport savings across time. Financial markets give them the flexibility to manage their own savings and investment plans, leaving the corporation’s financial managers with only one task: to increase market value.

A corporation’s roster of shareholders usually includes both risk-averse and risk-tolerant investors. You might expect the risk-averse to say, “Sure, maximize value, but don’t touch too many high-risk projects.” Instead, they say, “Risky projects are OK, provided that expected profits are more than enough to offset the risks. If this firm ends up too risky for my taste, I’ll adjust my investment portfolio to make it safer.” For example, the risk-averse shareholders can shift more of their investment to safer assets, such as U.S. government bonds. They can also just say good-bye, selling shares of the risky firm and buying shares in a safer one. If the risky investments increase market value, the departing shareholders are better off than if the risky investments were turned down.

2. A Fundamental Result

The goal of maximizing shareholder value is widely accepted in both theory and practice. It’s important to understand why. Let’s walk through the argument step by step, assuming that the financial manager should act in the interests of the firm’s owners, its stockholders.

- Each stockholder wants three things:

- To be as rich as possible, that is, to maximize his or her current wealth.

- To transform that wealth into the most desirable time pattern of consumption either by borrowing to spend now or investing to spend later.

- To manage the risk characteristics of that consumption plan.

- But stockholders do not need the financial manager’s help to achieve the best time pattern of consumption. They can do that on their own, provided they have free access to competitive financial markets. They can also choose the risk characteristics of their consumption plan by investing in more- or less-risky securities.

- How then can the financial manager help the firm’s stockholders? There is only one way: by increasing their wealth. That means increasing the market value of the firm and the current price of its shares.

Economists have proved this value-maximization principle with great rigor and generality. After you have absorbed this chapter, take a look at the Appendix, which contains a further example. The example, though simple, illustrates how the principle of value maximization follows from formal economic reasoning.

We have suggested that shareholders want to be richer rather than poorer. But sometimes you hear managers speak as if shareholders have different goals. For example, managers may say that their job is to “maximize profits.” That sounds reasonable. After all, don’t shareholders want their company to be profitable? But taken literally, profit maximization is not a well- defined financial objective for at least two reasons:

- Maximize profits? Which year’s profits? A corporation may be able to increase current profits by cutting back on outlays for maintenance or staff training, but that may result in lower profits in the future. Shareholders will not welcome higher short-term profits if long-term profits are damaged.

- A company may be able to increase future profits by cutting this year’s dividend and investing the freed-up cash in the firm. That is not in the shareholders’ best interest if the company earns only a modest return on the money.

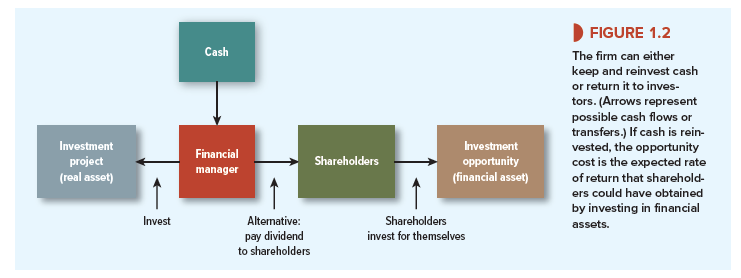

3. The Investment Trade-Off

OK, let’s take the objective as maximizing market value. But why do some investments increase market value, while others reduce it? The answer is given by Figure 1.2, which sets out the fundamental trade-off for corporate investment decisions. Suppose the corporation has a proposed investment in a real asset and enough cash on hand to finance the investment. If the corporation does not invest, it can instead pay out the cash to shareholders—say, as an extra dividend. How does the financial manager decide whether to go ahead with the project or to pay out the cash? (The investment and dividend arrows in Figure 1.2 are arrows 2 and 4b in Figure 1.1.)

Assume that the financial manager is acting in the interests of the corporation’s owners, its stockholders. What do these stockholders want the financial manager to do? The answer depends on the project’s rate of return and on the rate of return that the stockholders can earn by investing in financial markets. If the return offered by the investment project is higher than shareholders can get by investing on their own, then the shareholders would vote for the investment project. If the investment project offers a lower return than shareholders can achieve on their own, they would vote to cancel the project and take the cash instead.

Perhaps the investment project in Figure 1.2 is a proposal for Tesla to launch a new electric car. Suppose Tesla has set aside cash to launch the new model in 2020. It could go ahead with the launch, or it could choose to cancel the investment and instead pay the cash out to its stockholders. If it pays out the cash, the stockholders can then invest for themselves.

Suppose that Tesla’s new project is just about as risky as the U.S. stock market and that investment in the stock market offers a 10% expected rate of return. If the project offers a superior rate of return—say, 20%—then Tesla’s stockholders would be happy for the company to keep the cash and invest it in the new model. If the project offers only a 5% return, then the stockholders are better off with the cash and without the new model; in that case, the financial manager should turn down the project.

As long as a corporation’s proposed investments offer higher rates of return than its shareholders can earn for themselves in the stock market (or in other financial markets), its shareholders will applaud the investments, and its stock price will increase. But if the company earns an inferior return, shareholders boo, stock price falls, and stockholders demand their money back so that they can invest on their own.

In our example, the minimum acceptable rate of return on Tesla’s new car is 10%. This minimum rate of return is called a hurdle rate or cost of capital. It is really an opportunity cost of capital because it depends on the investment opportunities available to investors in financial markets. Whenever a corporation invests cash in a new project, its shareholders lose the opportunity to invest the cash on their own. Corporations increase value by accepting all investment projects that earn more than the opportunity cost of capital.

Notice that the opportunity cost of capital depends on the risk of the proposed investment project. Why? It’s not just because shareholders are risk-averse. It’s also because shareholders have to trade off risk against return when they invest on their own. The safest investments, such as U.S. government debt, offer low rates of return. Investments with higher expected rates of return—the stock market, for example—are riskier and sometimes deliver painful losses. (The U.S. stock market was down 38% in 2008, for example.) Other investments are riskier still. For example, high-tech growth stocks offer the prospect of higher rates of return but are even more volatile.

Also notice that the opportunity cost of capital is generally not the interest rate that the company pays on a loan from a bank. If the company is making a risky investment, the opportunity cost is the expected return that investors can achieve in financial markets at the same level of risk. The expected return on risky securities is well above the interest rate on a bank loan.

Managers look to the financial markets to measure the opportunity cost of capital for the firm’s investment projects. They can observe the opportunity cost of capital for safe investments by looking up current interest rates on safe debt securities. For risky investments, the opportunity cost of capital has to be estimated. We start to tackle this task in Chapter 7.

4. Should Managers Look After the Interests of Their Shareholders?

So far we have assumed that financial managers should act on behalf of shareholders by trying to maximize their wealth. But perhaps this begs the questions: Is it desirable for managers to act in the selfish interests of their shareholders? Does a focus on enriching the shareholders mean that managers must act as greedy mercenaries riding roughshod over the weak and helpless?

Most of this book is devoted to financial policies that increase value. None of these policies requires gallops over the weak and helpless. In most instances, little conflict arises between doing well (maximizing value) and doing good. Profitable firms are those with satisfied customers and loyal employees; firms with dissatisfied customers and a disgruntled workforce will probably end up with declining profits and a low stock price.

Most established corporations can add value by building long-term relationships with their customers and establishing a reputation for fair dealing and financial integrity. When something happens to undermine that reputation, the costs can be enormous.

So, when we say that the objective of the firm is to maximize shareholder wealth, we do not mean that anything goes. The law deters managers from making blatantly dishonest decisions, but most managers should not be simply concerned with observing the letter of the law or with keeping to written contracts. In business and finance, as in other day-to-day affairs, there are unwritten rules of behavior. These rules make routine financial transactions feasible because each party to the transaction has to trust the other to keep to his or her side of the bargain.[2]

When something happens to damage that trust, the costs can be enormous. Volkswagen (VW) is a case in point. VW had installed secret software that cut back pollution from its diesel cars, but only when the cars were tested. Discovery of the software in 2015 caused a tidal wave of opprobrium. VW’s stock price dropped by 35%. Its CEO was fired. VW diesel vehicles piled up unsold in car dealers’ lots. In the United States alone, the scandal is likely to cost the company more than $20 billion in fines and compensation payments.

Charlatans and swindlers are often able to hide behind booming markets. It is only “when the tide goes out that you learn who’s been swimming naked.”7 The tide went out in 2008, and a number of frauds were exposed. One notorious example was the Ponzi scheme run by the New York financier Bernard Madoff.8 Individuals and institutions put about $65 billion in the scheme before it collapsed in 2008. (It’s not clear what Madoff did with all this money, but much of it was apparently paid out to early investors in the scheme to create an impression of superior investment performance.) With hindsight, the investors should not have trusted Madoff or the financial advisers who steered money to Madoff.

Madoff’s Ponzi scheme was (we hope) a once-in-a-lifetime event.9 It was astonishingly unethical, illegal, and bound to end in tears. That much is obvious. The difficult ethical problems for financial managers lurk in the grey areas. Look, for example, at the nearby Finance in Practice box that presents three ethical problems. Think about where you stand on these issues and where you would draw the ethical red line.

What is the underlying source of unethical business behavior? Sometimes it is simply because an employee is dishonest. But frequently the behavior stems from a culture in the firm that encourages high-pressure selling or unscrupulous dealing. In this case, the root of the problem lies with top management that promotes such values. (Click on the nearby Beyond the Page feature for an interesting demonstration of this in the banking industry.)

5. Agency Problems and Corporate Governance

We have emphasized the separation of ownership and control in public corporations. The owners (shareholders) cannot control what the managers do, except indirectly through the board of directors. This separation is necessary but also dangerous. You can see the risks. Managers may be tempted to buy sumptuous corporate jets or to schedule business meetings at tony resorts. They may shy away from attractive but risky projects because they are worried more about the safety of their jobs than about maximizing shareholder value. They may work just to maximize their own bonuses, and therefore redouble their efforts to make and resell flawed subprime mortgages.

Conflicts between shareholders’ and managers’ objectives create agency problems. Agency problems arise when agents work for principals. The shareholders are the principals; the managers are their agents. Agency costs are incurred when (1) managers do not attempt to maximize firm value and (2) shareholders incur costs to monitor the managers and constrain their actions.

Agency problems can sometimes lead to outrageous behavior. For example, when Dennis Kozlowski, the CEO of Tyco, threw a $2 million 40th birthday bash for his wife, he charged half of the cost to the company. This of course was an extreme conflict of interest, as well as illegal. But more subtle and moderate agency problems arise whenever managers think just a little less hard about spending money when it is not their own.

Later in the book we will look at how good systems of governance ensure that shareholders’ pockets are close to the managers’ hearts. This means well-designed incentives for managers, standards for accounting and disclosure to investors, requirements for boards of directors, and legal sanctions for self-dealing by management. When scandals happen, we say that corporate governance has broken down. When corporations compete effectively and ethically to deliver value to shareholders, we are comforted that governance is working properly.

25 Jun 2021

24 Jun 2021

25 Jun 2021

24 Jun 2021

24 Jun 2021

24 Jun 2021