To illustrate some of the problems involved in predicting economic rents, let us leap forward several years and look at the decision by Marvin Enterprises to exploit a new technology.[1]

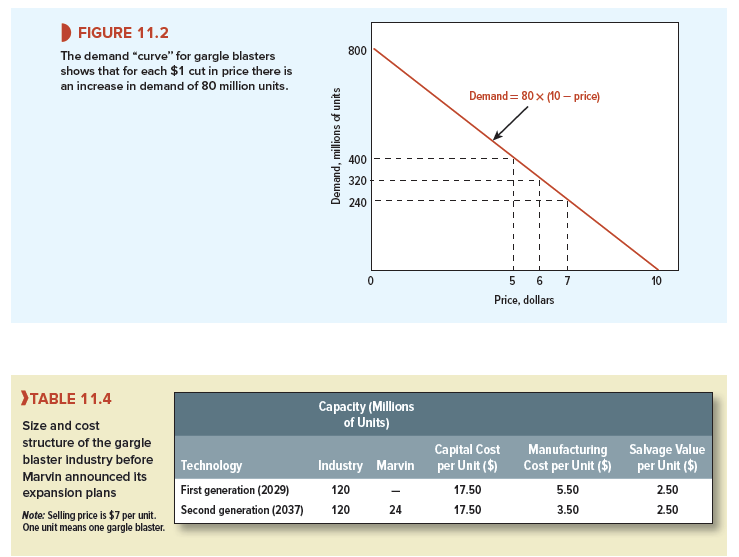

One of the most unexpected developments of these years was the remarkable growth of a completely new industry. By 2041, annual sales of gargle blasters totaled $1.68 billion, or 240 million units. Although it controlled only 10% of the market, Marvin Enterprises was among the most exciting growth companies of the decade. Marvin had come late into the business, but it had pioneered the use of implanted microcircuits to control the genetic engineering processes used to manufacture gargle blasters. This development had enabled producers to cut the price of gargle blasters from $9 to $7 and had thereby contributed to the dramatic growth in the size of the market. The estimated demand curve in Figure 11.2 shows just how responsive demand is to such price reductions.

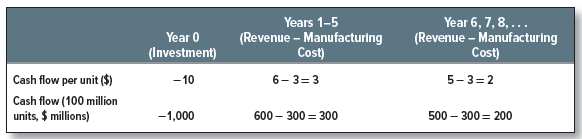

Table 11.4 summarizes the cost structure of the old and new technologies. While companies with the new technology were earning 20% on their initial investment, those with first- generation equipment had been hit by the successive price cuts. Since all Marvin’s investment was in the 2037 technology, it had been particularly well placed during this period.

Rumors of new developments at Marvin had been circulating for some time, and the total market value of Marvin’s stock had risen to $460 million by January 2042. At that point, Marvin called a press conference to announce another technological breakthrough. Management claimed that its new third-generation process involving mutant neurons enabled the firm to reduce capital costs to $10 and manufacturing costs to $3 per unit. Marvin proposed to capitalize on this invention by embarking on a huge $1 billion expansion program that would add 100 million units to capacity. The company expected to be in full operation within 12 months.

Before deciding to go ahead with this development, Marvin had undertaken extensive calculations on the effect of the new investment. The basic assumptions were as follows:

- The cost of capital was 20%.

- The production facilities had an indefinite physical life.

- The demand curve and the costs of each technology would not change.

- There was no chance of a fourth-generation technology in the foreseeable future.

- The corporate income tax, which had been abolished in 2032, was not likely to be reintroduced.

Marvin’s competitors greeted the news with varying degrees of concern. There was general agreement that it would be five years before any of them would have access to the new technology. On the other hand, many consoled themselves with the reflection that Marvin’s new plant could not compete with an existing plant that had been fully depreciated.

Suppose that you were Marvin’s financial manager. Would you have agreed with the decision to expand? Do you think it would have been better to go for a larger or smaller expansion? How do you think Marvin’s announcement is likely to affect the price of its stock?

You have a choice. You can go on immediately to read our solution to these questions. But you will learn much more if you stop and work out your own answer first. Try it.

1. Forecasting Prices of Gargle Blasters

Up to this point in any capital budgeting problem, we have always given you the set of cashflow forecasts. In the present case, you have to derive those forecasts.

The first problem is to decide what is going to happen to the price of gargle blasters. Marvin’s new venture will increase industry capacity to 340 million units. From the demand curve in Figure 11.2, you can see that the industry can sell this number of gargle blasters only if the price declines to $5.75:

If the price falls to $5.75, what will happen to companies with the 2029 technology? They also have to make an investment decision: Should they stay in business, or should they sell their equipment for its salvage value of $2.50 per unit? With a 20% opportunity cost of capital, the NPV of staying in business is

Smart companies with 2029 equipment will, therefore, see that it is better to sell off capacity. No matter what their equipment originally cost or how far it is depreciated, it is more profitable to sell the equipment for $2.50 per unit than to operate it and lose $1.25 per unit.

As capacity is sold off, the supply of gargle blasters will decline and the price will rise. An equilibrium is reached when the price gets to $6. At this point 2029 equipment has a zero NPV:

![]()

How much capacity will have to be sold off before the price reaches $6? You can check that by going back to the demand curve:

Therefore Marvin’s expansion will cause the price to settle down at $6 a unit and will induce first-generation producers to withdraw 20 million units of capacity.

But after five years, Marvin’s competitors will also be in a position to build third-generation plants. As long as these plants have positive NPVs, companies will increase their capacity and force prices down once again. A new equilibrium will be reached when the price reaches $5. At this point, the NPV of new third-generation plants is zero, and there is no incentive for companies to expand further:

![]()

Looking back once more at our demand curve, you can see that with a price of $5 the industry can sell a total of 400 million gargle blasters:

Demand = 80 X (10 – price) = 80 X (10 – 5) = 400 million units

The effect of the third-generation technology is, therefore, to cause industry sales to expand from 240 million units in 2041 to 400 million five years later. But that rapid growth is no protection against failure. By the end of five years, any company that has only first-generation equipment will no longer be able to cover its manufacturing costs and will be forced out of business.

2. The Value of Marvin’s New Expansion

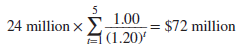

We have shown that the introduction of third-generation technology is likely to cause gargle blaster prices to decline to $6 for the next five years and to $5 thereafter. We can now set down the expected cash flows from Marvin’s new plant:

Discounting these cash flows at 20% gives us

It looks as if Marvin’s decision to go ahead was correct. But there is something we have forgotten. When we evaluate an investment, we must consider all incremental cash flows. One effect of Marvin’s decision to expand is to reduce the value of its existing 2037 plant. If Marvin decided not to go ahead with the new technology, the $7 price of gargle blasters would hold until Marvin’s competitors started to cut prices in five years’ time. Marvin’s decision, therefore, leads to an immediate $1 cut in price. This reduces the present value of its 2037 equipment by

Considered in isolation, Marvin’s decision has an NPV of $299 million. But it also reduces the value of existing plant by $72 million. The net present value of Marvin’s venture is, therefore, 299 – 72 = $227 million.

3. Alternative Expansion Plans

Marvin’s expansion has a positive NPV, but perhaps Marvin would do better to build a larger or smaller plant. You can check that by going through the same calculations as above. First you need to estimate how the additional capacity will affect gargle blaster prices. Then you can calculate the net present value of the new plant and the change in the present value of the existing plant. The total NPV of Marvin’s expansion plan is

Total NPV = NPV of new plant + change in PV of existing plant

We have undertaken these calculations and plotted the results in Figure 11.3. You can see how total NPV would be affected by a smaller or larger expansion.

When the new technology becomes generally available in 2047, firms will construct a total of 280 million units of new capacity.[2] But Figure 11.3 shows that it would be foolish for Marvin to go that far. If Marvin added 280 million units of new capacity in 2042, the discounted value of the cash flows from the new plant would be zero and the company would have reduced the value of its old plant by $144 million. To maximize NPV, Marvin should construct 200 million units of new capacity and set the price just below $6 to drive out the 2029 manufacturers. Output is, therefore, less and price is higher than either would be under free competition.

4. The Value of Marvin Stock

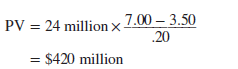

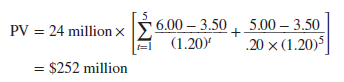

Let us think about the effect of Marvin’s announcement on the value of its common stock. Marvin has 24 million units of second-generation capacity. In the absence of any third- generation technology, gargle blaster prices would hold at $7 and Marvin’s existing plant would be worth

Marvin’s new technology reduces the price of gargle blasters initially to $6 and after five years to $5. Therefore the value of existing plant declines to

But the new plant makes a net addition to shareholders’ wealth of $299 million. So after Marvin’s announcement its stock will be worth

![]()

Now here is an illustration of something we talked about in Chapter 4: Before the announcement, Marvin’s stock was valued in the market at $460 million. The difference between this figure and the value of the existing plant represented the present value of Marvin’s growth opportunities (PVGO). The market valued Marvin’s ability to stay ahead of the game at $40 million even before the announcement. After the announcement PVGO rose to $299 million.[5]

5. The Lessons of Marvin Enterprises

Marvin Enterprises may be just a piece of science fiction, but the problems that it confronts are very real. Whenever Intel considers developing a new microprocessor or Pfizer considers developing a new drug, these firms must face up to exactly the same issues as Marvin. We have tried to illustrate the kind of questions that you should be asking when presented with a set of cash-flow forecasts. Of course, no economic model is going to predict the future with

accuracy. Perhaps Marvin can hold the price above $6. Perhaps competitors will not appreciate the rich pickings to be had in the year 2047. In that case, Marvin’s expansion would be even more profitable. But would you want to bet $1 billion on such possibilities? We don’t think so.

Investments often turn out to earn far more than the cost of capital because of a favorable surprise. This surprise may in turn create a temporary opportunity for further investments earning more than the cost of capital. But anticipated and more prolonged rents will naturally lead to the entry of rival producers. That is why you should be suspicious of any investment proposal that predicts a stream of economic rents into the indefinite future. Try to estimate when competition will drive the NPV down to zero, and think what that implies for the price of your product.

Many companies try to identify the major growth areas in the economy and then concentrate their investment in these areas. But the sad fate of first-generation gargle blaster manufacturers illustrates how rapidly existing plants can be made obsolete by changes in technology. It is fun being in a growth industry when you are at the forefront of the new technology, but a growth industry has no mercy on technological laggards.

Therefore, do not simply follow the herd of investors stampeding into high-growth sectors of the economy. Think of the fate of the dot-com companies in the “new economy” of the late 1990s. Optimists argued that the information revolution was opening up opportunities for companies to grow at unprecedented rates. The pessimists pointed out that competition in e-commerce was likely to be intense and that competition would ensure that the benefits of the information revolution would go largely to consumers. The Finance in Practice box emphasizes that rapid growth is no guarantee of superior profits.

We do not wish to imply that good investment opportunities don’t exist. For example, good opportunities frequently arise because the firm has invested money in the past, which gives it the option to expand cheaply in the future. Perhaps the firm can increase its output just by adding an extra production line, whereas its rivals would need to construct an entirely new factory.

Marvin also reminds us to include a project’s impact on the rest of the firm when estimating incremental cash flows. By introducing the new technology immediately, Marvin reduced the value of its existing plant by $72 million.

Sometimes the losses on existing plants may completely offset the gains from a new technology. That is why we may see established, technologically advanced companies deliberately slowing down the rate at which they introduce new products. But this can be a dangerous game to play if it opens up opportunities for competitors. For example, for many years Bausch & Lomb was the dominant producer of contact lenses and earned large profits from glass contact lenses that needed to be sterilized every night. Because its existing business generated high returns, the company was slow to introduce disposable lenses. This delay opened up an opportunity for competitors and enabled Johnson & Johnson to introduce disposable lenses.

Marvin’s economic rents were equal to the difference between its costs and those of the marginal producer. The costs of the marginal 2029-generation plant consisted of the manufacturing costs plus the opportunity cost of not selling the equipment. Therefore, if the salvage value of the 2029 equipment were higher, Marvin’s competitors would incur higher costs and Marvin could earn higher rents. We took the salvage value as given, but it in turn depends on the cost savings from substituting outdated gargle blaster equipment for some other asset. In a well-functioning economy, assets will be used so as to minimize the total cost of producing the chosen set of outputs. The economic rents earned by any asset are equal to the total extra costs that would be incurred if that asset were withdrawn.

When Marvin announced its expansion plans, many owners of first-generation equipment took comfort in the belief that Marvin could not compete with their fully depreciated plant. Their comfort was misplaced. Regardless of past depreciation policy, it paid to scrap first- generation equipment rather than keep it in production. Do not expect that numbers in your balance sheet can protect you from harsh economic reality.

Absolutely pent written content, Really enjoyed looking at.

Very efficiently written information. It will be beneficial to anybody who employess it, as well as myself. Keep doing what you are doing – for sure i will check out more posts.