In June 2018, Amazon held $16.7 billion in cash and $8.3 billion in short-term securities. Short-term securities pay interest; cash doesn’t. So why do firms such as Amazon hold such large amounts of cash? Why don’t they arrange for the bank to “sweep” the cash at the end of the day into an interest-bearing investment, such as a money-market mutual fund?

There are at least two reasons. First, cash may be left in non-interest-bearing accounts to compensate banks for the services they provide. Second, large corporations may have literally hundreds of accounts with dozens of different banks. It is often better to leave idle cash in these accounts than to monitor every account every day in order to make daily transfers between them.

One major reason for this proliferation of bank accounts is decentralized management. You cannot give a subsidiary operating autonomy without giving its managers the right to spend and receive cash. Good cash management nevertheless implies some degree of centralization. It is impossible to maintain your desired cash inventory if all the subsidiaries in the group are responsible for their own private pools of cash. And you certainly want to avoid situations in which one subsidiary is investing its spare cash at 5% while another is borrowing at 8%. It is not surprising, therefore, that even in highly decentralized companies there is generally central control over cash balances and bank relations.

1. How Purchases Are Paid For

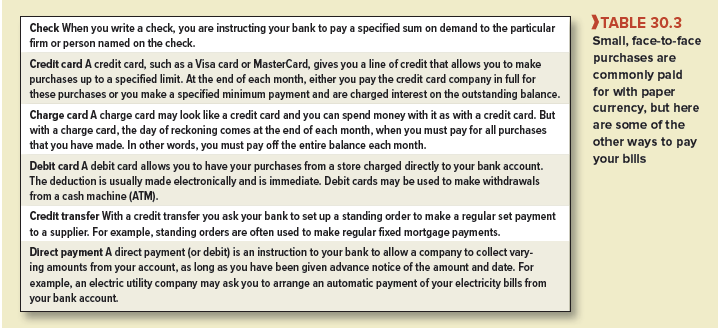

Many small, face-to-face purchases are made with paper currency. But you probably would not want to use cash to buy a new car, and you can’t use cash to make a purchase over the Internet. There are a variety of ways that you can pay for larger purchases or send payments to another location. Some of the more important ways are set out in Table 30.3.

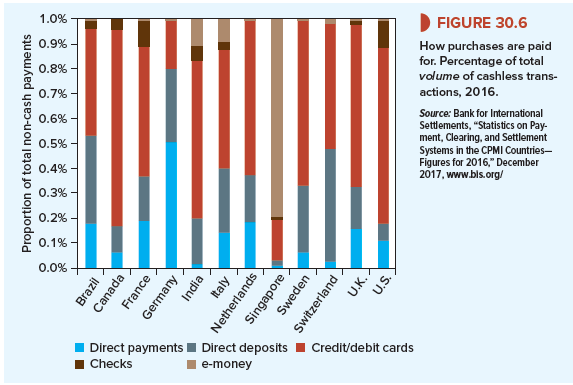

Look now at Figure 30.6. You can see that there are large differences in the ways that people around the world pay for their purchases. For example, checks are almost unknown in Germany, the Netherlands, and Sweden.[1] Most payments in these countries are by debit card or credit transfer. By contrast, Americans love to write checks. Each year individuals and firms in the United States write about 12 billion checks.

But throughout the world the use of checks is on the decline. For one-off purchases they are being replaced by credit or debit cards. In addition, mobile phone technology and the Internet are encouraging the development of new infant payment systems. For example,

- Electronic bill presentment and payment (or EBPP) allows companies to bill customers and receive payments via the Internet. EBPP is forecasted to grow rapidly.

- Stored-value cards (or e-money) let you transfer cash value to a card that can be used to buy a variety of goods and services. For example, Hong Kong’s Octopus card system, which was developed to pay for travel fares, has become a widely used electronic cash system throughout the territory.

There are three main ways that firms send and receive money electronically. These are direct payments, direct deposits, and wire transfers.

Recurring expenditures, such as utility bills, mortgage payments, and insurance premiums, are increasingly settled by direct payment (also called automatic debit or direct debit). In this case, the firm’s customers simply authorize it to debit their bank account for the amount due. The company provides its bank with a file showing details of each customer, the amount to be debited, and the date. The payment then travels electronically through the Automated Clearing House (ACH) system. The firm knows exactly when the cash is coming in and avoids the labor-intensive process of handling thousands of checks.

The ACH system also allows money to flow in the reverse direction. Thus while a direct payment transaction provides an automatic debit, a direct deposit constitutes an automatic credit. Direct deposits are used to make bulk payments such as wages or dividends. Again the company provides its bank with a file of instructions. The bank then debits the company’s account and transfers the cash via the ACH to the bank accounts of the firm’s employees or shareholders.

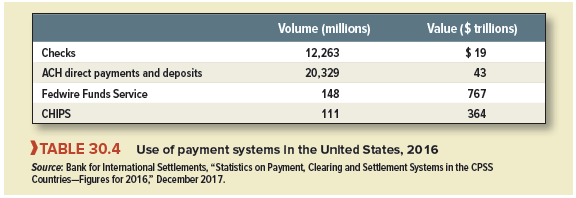

The volume of direct payments and deposits has increased rapidly. You can see from Table 30.4 that the total value of these transactions is over double that of checks.

Large-value payments between companies are usually made electronically through Fed- wire or CHIPS. Fedwire is operated by the Federal Reserve system and connects more than 6,000 financial institutions to the Fed and, thereby, to each other.[5] CHIPS is a bank-owned system. It mainly handles eurodollar payments and foreign exchange transactions and is used for more than 95% of cross-border payments in dollars. Table 30.4 shows that the number of payments by Fedwire and CHIPS is relatively small, but the sums involved are huge.

2. Speeding Up Check Collections

Although checks are rarely used for large-value payments, they continue to be widely used for smaller nonrecurring transactions. Check handling is a cumbersome and labor-intensive task. However, changes to legislation in the United States at the beginning of the century have helped to reduce costs and speed up collections. The Check Clearing for the 21st Century Act, usually known as Check 21, allows banks to send digital images of checks to one another rather than sending the checks themselves. Thus, cargo planes no longer crisscross the country taking bundles of checks from one bank to another. Instead, almost all check clearing is now digital. The cost of processing checks is also being reduced by a technological innovation known as check conversion. In this case, when you write a check, the details of your bank account and the amount of the payment are automatically captured at the point of sale, your check is handed back to you, and your bank account is immediately debited.

Firms that receive a large volume of checks have devised a number of ways to ensure that the cash becomes available as quickly as possible. For example, a retail chain may arrange for each branch to deposit receipts in a collection account at a local bank. Surplus funds are then periodically transferred electronically to a concentration account at one of the company’s principal banks. There are two reasons that concentration banking allows the company to gain quicker use of its funds. First, because the store is nearer to the bank, transfer times are reduced. Second, because the customer’s check is likely to be drawn on a local bank, the time taken to clear the check is also reduced.

Concentration banking is often combined with a lockbox system. In this case, the firm’s customers are instructed to send their payments to a regional post-office box. The local bank then takes on the administrative chore of emptying the box and depositing the checks in the company’s local deposit account.

3. International Cash Management

Cash management in domestic firms is child’s play compared with cash management in large multinational corporations operating in dozens of countries, each with its own currency, banking system, and legal structure.

A single centralized cash management system is an unattainable ideal for these companies, although they are edging toward it. For example, suppose that you are treasurer of a large multinational company with operations throughout Europe. You could allow the separate businesses to manage their own cash, but that would be costly and would almost certainly result in each one accumulating little hoards of cash. The solution is to set up a regional system. In this case the company establishes a local concentration account with a bank in each country. Any surplus cash is swept daily into a central multicurrency account in London or another European banking center. This cash is then invested in marketable securities or used to finance any plants or subsidiaries that have a cash shortage.

Payments can also be made out of the regional center. For example, to pay wages in each European country, the company just needs to send its principal bank a computer file of the payments to be made. The bank then finds the least costly way to transfer the cash from the company’s central accounts and arranges for the cash to be credited on the correct day to the employees in each country.

Rather than actually moving cash between local bank accounts and a regional concentration account, the company may employ a multinational bank with branches in each country and then arrange for the bank to pool all the cash surpluses and shortages. In this case no money is transferred between accounts. Instead, the bank just adds together the credit and debit balances, and pays the firm interest on any surplus.

When a company’s international branches trade with each other, the number of cross-border transactions can multiply rapidly. Rather than having payments flowing in all directions, the company can set up a netting system. Each branch can then calculate its net position and undertake a single transaction with the netting center. Several industries have set up netting systems for their members. For example, more than 200 airlines have come together to establish a netting system for the foreign currency payments that they must make to each other.

4. Paying for Bank Services

Much of the work of cash management—processing checks, transferring funds, running lockboxes, helping keep track of the company’s accounts—is done by banks. And banks provide many other services not so directly linked to cash management, such as handling payments and receipts in foreign currency, or acting as custodian for securities.

All these services need to be paid for. Usually payment is in the form of a monthly fee, but banks may agree to waive the fee as long as the firm maintains a minimum average balance in an interest-free deposit. Banks are prepared to do this because, after setting aside a portion of the money in a reserve account with the Fed, they can relend the money to earn interest. Demand deposits earmarked to pay for bank services are termed compensating balances. They used to be a very common way to pay for bank services, but since banks have been permitted to pay interest on demand deposits, there has been a steady trend away from using compensating balances and toward direct fees.

well article