A different cost flow is assumed for the FIFO, LIFO, and weighted average inventory cost flow methods. As a result, the three methods normally yield different amounts for the following:

- Cost of merchandise sold

- Gross profit

- Net income

- Ending merchandise inventory

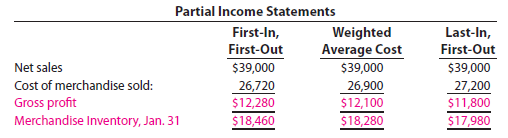

Using the perpetual inventory system illustration with sales of $39,000 (1,300 units x $30), these differences are illustrated below.

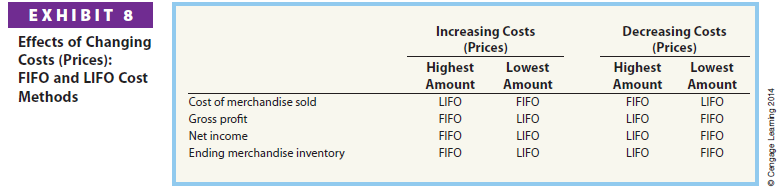

The preceding differences show the effect of increasing costs (prices). If costs (prices) remain the same, all three methods would yield the same results. However, costs (prices) normally do change. The effects of changing costs (prices) on the FIFO and LIFO methods are summarized in Exhibit 8. The weighted average cost method will always yield results between those of FIFO and LIFO.

FIFO reports higher gross profit and net income than the LIFO method when costs (prices) are increasing, as shown in Exhibit 8. However, in periods of rapidly rising costs, the inventory that is sold must be replaced at increasingly higher costs. In such cases, the larger FIFO gross profit and net income are sometimes called inventory profits or illusory profits.

During a period of increasing costs, LIFO matches more recent costs against sales on the income statement. Thus, it can be argued that the LIFO method more nearly matches current costs with current revenues. LIFO also offers an income tax savings during periods of increasing costs. This is because LIFO reports the lowest amount of gross profit and, thus, taxable net income.[2] However, under LIFO, the ending inventory on the balance sheet may be quite different from its current replacement cost. In such cases, the financial statements normally include a note that estimates what the inventory would have been if FIFO had been used.

The weighted average cost method is, in a sense, a compromise between FIFO and LIFO. The effect of cost (price) trends is averaged in determining the cost of merchandise sold and the ending inventory.

Source: Warren Carl S., Reeve James M., Duchac Jonathan (2013), Corporate Financial Accounting, South-Western College Pub; 12th edition.

It’s hard to find knowledgeable people on this topic, but you sound like you know what you’re talking about! Thanks