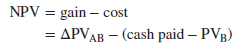

Suppose that you are the financial manager of firm A and you want to analyze the possible purchase of firm B. The first thing to think about is whether there is an economic gain from the merger. There is an economic gain only if the two firms are worth more together than apart. For example, if you think that the combined firm would be worth PVAB and that the separate firms are worth PVA and PVB, then

![]()

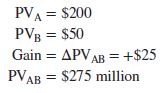

If this gain is positive, there is an economic justification for merger. But you also have to think about the cost of acquiring firm B. Take the easy case in which payment is made in cash. Then the cost of acquiring B is equal to the cash payment minus B’s value as a separate entity. Thus,

![]()

The net present value to A of a merger with B is measured by the difference between the gain and the cost. Therefore, you should go ahead with the merger if its net present value, defined as

We like to write the merger criterion in this way because it focuses attention on two distinct questions. When you estimate the benefit, you concentrate on whether there are any gains to be made from the merger. When you estimate cost, you are concerned with the division of these gains between the two companies.

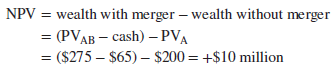

An example may help make this clear. Firm A has a value of $200 million, and B has a value of $50 million. Merging the two would allow cost savings with a present value of $25 million. This is the gain from the merger. Thus,

Suppose that B is bought for cash—say, for $65 million. The cost of the merger is

![]()

Note that the stockholders of firm B—the people on the other side of the transaction—are ahead by $15 million. Their gain is your cost. They have captured $15 million of the $25 million merger gain. Thus when we write down the NPV of the merger from A’s viewpoint, we are really calculating the part of the gain that A’s stockholders get to keep. The NPV to A’s stockholders equals the overall gain from the merger less that part of the gain captured by B’s stockholders:

NPV = 25 – 15 = +$10 million

Just as a check, let’s confirm that A’s stockholders really come out $10 million ahead. They start with a firm worth PVA = $200 million. They end up with a firm worth $275 million and then have to pay out $65 million to B’s stockholders.[1] Thus their net gain is

Suppose investors do not anticipate the merger between A and B. The announcement will cause the value of B’s stock to rise from $50 million to $65 million, a 30% increase. If investors share management’s assessment of the merger gains, the market value of A’s stock will increase by $10 million, only a 5% increase.

It makes sense to keep an eye on what investors think the gains from merging are. If A’s stock price falls when the deal is announced, then investors are sending the message that the merger benefits are doubtful or that A is paying too much for them.

1. Right and Wrong Ways to Estimate the Benefits of Mergers

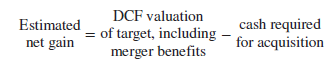

Some companies begin their merger analyses with a forecast of the target firm’s future cash flows. Any revenue increases or cost reductions attributable to the merger are included in the forecasts, which are then discounted back to the present and compared with the purchase price:

This is a dangerous procedure. Even the brightest and best-trained analyst can make large errors in valuing a business. The estimated net gain may come up positive not because the merger makes sense but simply because the analyst’s cash-flow forecasts are too optimistic. On the other hand, a good merger may not be pursued if the analyst fails to recognize the target’s potential as a stand-alone business.

Our procedure starts with the target’s stand-alone market value (PVB) and concentrates on the changes in cash flow that would result from the merger. Ask yourself why the two firms should be worth more together than apart.

The same advice holds when you are contemplating the sale of part of your business. There is no point in saying to yourself, “This is an unprofitable business and should be sold.” Unless the buyer can run the business better than you can, the price you receive will reflect the poor prospects.

Sometimes you may come across managers who believe that there are simple rules for identifying good acquisitions. They may say, for example, that they always try to buy into growth industries or that they have a policy of acquiring companies that are selling below book value. But our comments in Chapter 11 about the characteristics of a good investment decision also hold true when you are buying a whole company. You add value only if you can generate additional economic rents—some competitive edge that other firms can’t match and the target firm’s managers can’t achieve on their own.

One final piece of horse sense: Often, two companies bid against each other to acquire the same target firm. In effect, the target firm puts itself up for auction. In such cases, ask yourself whether the target is worth more to you than to the other bidder. If the answer is no, you should be cautious about getting into a bidding contest. Winning such a contest may be more expensive than losing it. If you lose, you have simply wasted your time; if you win, you have probably paid too much.

2. More on Estimating Costs—What If the Target’s Stock Price Anticipates the Merger?

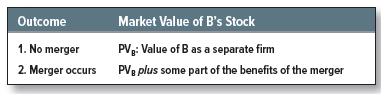

The cost of a merger is the premium that the buyer pays over the seller’s stand-alone value. How can that value be determined? If the target is a public company, you can start with its market value; just observe price per share and multiply by the number of shares outstanding. But bear in mind that if investors expect A to acquire B, or if they expect somebody to acquire B, the market value of B may overstate its stand-alone value.

This is one of the few places in this book where we draw an important distinction between market value (MV) and the true, or “intrinsic,” value (PV) of the firm as a separate entity. The problem here is not that the market value of B is wrong but that it may not be the value of firm B as a separate entity. Potential investors in B’s stock will see two possible outcomes and two possible values:

If the second outcome is possible, MVB, the stock market value we observe for B, will overstate PVB. This is exactly what should happen in a competitive capital market. Unfortunately, it complicates the task of a financial manager who is evaluating a merger.

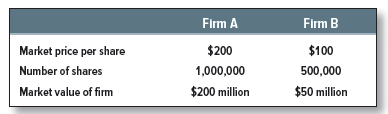

Here is an example: Suppose that just before A and B’s merger announcement we observe the following:

Firm A intends to pay $65 million cash for B. If B’s market price reflects only its value as a separate entity, then

Cost = (cash paid – PVB)

= (65 – 50) = $15 million

However, suppose that B’s share price has already risen by $12 because of rumors that B might get a favorable merger offer. That means that its intrinsic value is overstated by 12 x 500,000 = $6 million. Its true value, PVB, is only $44 million. Then

Cost = (65 – 44) = $21 million

Since the merger gain is $25 million, this deal still makes A’s stockholders better off, but B’s stockholders are now capturing the lion’s share of the gain.

Notice that if the market made a mistake, and the market value of B was less than B’s true value as a separate entity, the cost could be negative. In other words, B would be a bargain and the merger would be worthwhile from A’s point of view, even if the two firms were worth no more together than apart. Of course, A’s stockholders’ gain would be B’s stockholders’ loss because B would be sold for less than its true value.

Firms have made acquisitions just because their managers believed they had spotted a company whose intrinsic value was not fully appreciated by the stock market. However, we know from the evidence on market efficiency that “cheap” stocks often turn out to be expensive. It is not easy for outsiders, whether investors or managers, to find firms that are truly undervalued by the market. Moreover, if the shares are really bargain-priced, A doesn’t need a merger to profit by its special knowledge. It can just buy up B’s shares on the open market and hold them passively, waiting for other investors to wake up to B’s true value.

If firm A is wise, it will not go ahead with a merger if the cost exceeds the gain. Firm B will not consent if A’s gain is so big that B loses. This gives us a range of possible cash payments that would allow the merger to take place. Whether the payment is at the top or the bottom of this range depends on the relative bargaining power of the two participants.

3. Estimating Cost When the Merger Is Financed by Stock

Many mergers involve payment wholly or partly in the form of the acquirer’s stock. When a merger is financed by stock, cost depends on the value of the shares in the new company received by the shareholders of the selling company. If the sellers receive N shares, each worth PAB, the cost is

![]()

Just be sure to use the price per share after the merger is announced and its benefits are appreciated by investors.

Suppose that A offers 325,000 (.325 million) shares instead of $65 million in cash. A’s share price before the deal is announced is $200. If B is worth $50 million stand-alone,[2] the cost of the merger appears to be

Apparent cost = .325 X 200 – 50 = $15 million

However, the apparent cost may not be the true cost. A’s stock price is $200 before the merger announcement. At the announcement it ought to go up.

Given the gain and the terms of the deal, we can calculate share prices and market values after the deal. The new firm will have 1.325 million shares outstanding and will be worth $275 million.[3] The new share price is 275/1.325 = $207.55. The true cost is

Cost = .325 X 207.55 – 50 = $17.45 million

This cost can also be calculated by figuring out the gain to B’s shareholders. They end up with .325 million shares, or 24.5% of the new firm AB. Their gain is

.245(275) – 50 = $17.45 million

In general, if B’s shareholders are given the fraction x of the combined firms,

![]()

We can now understand the first key distinction between cash and stock as financing instruments. If cash is offered, the cost of the merger is unaffected by the merger gains. If stock is offered, the cost depends on the gains because the gains show up in the postmerger share price.

Stock financing mitigates the effect of overvaluation or undervaluation of either firm. Suppose, for example, that A overestimates B’s value as a separate entity, perhaps because it has overlooked some hidden liability. Thus, A makes too generous an offer. Other things being equal, A’s stockholders are better off if it is a stock offer rather than a cash offer. With a stock offer, the inevitable bad news about B’s value will fall partly on the shoulders of B’s stockholders.

4. Asymmetric Information

There is a second key difference between cash and stock financing for mergers. A’s managers will usually have access to information about A’s prospects that is not available to outsiders. Economists call this asymmetric information.

Suppose A’s managers are more optimistic than outside investors. They may think that A’s shares will really be worth $215 after the merger, $7.45 higher than the $207.55 market price we just calculated. If they are right, the true cost of a stock-financed merger with B is

Cost = .325 X 215 – 50 = $19.88

B’s shareholders would get a “free gift” of $7.45 for every A share they receive—an extra gain of $7.45 X .325 = 2.42, that is, $2.42 million.

Of course, if A’s managers were really this optimistic, they would strongly prefer to finance the merger with cash. Financing with stock would be favored by pessimistic managers who think their company’s shares are overvalued.

Does this sound like “win-win” for A—just issue shares when overvalued, cash otherwise? No, it’s not that easy, because B’s shareholders, and outside investors generally, understand what’s going on. Suppose you are negotiating on behalf of B. You find that A’s managers keep suggesting stock rather than cash financing. You quickly infer that A’s managers are pessimistic, mark down your own opinion of what the shares are worth, and drive a harder bargain.

This asymmetric-information story explains why the share prices of buying firms generally fall when stock-financed mergers are announced.[4] Andrade, Mitchell, and Stafford found an average market-adjusted fall of 1.5% on the announcement of stock-financed mergers between 1973 and 1998. There was a small gain (.4%) for a sample of cash-financed deals.[5]

It’s really a great and helpful piece of info. I’m glad that you shared this useful information with us. Please keep us informed like this. Thank you for sharing.

Very interesting information!Perfect just what I was looking for!