The left-wing dividend creed is simple: Whenever dividends are taxed more heavily than capital gains, firms should pay the lowest cash dividend they can get away with. Cash available for payout should be used to repurchase shares.

By shifting their distribution policies in this way, corporations can transmute dividends into capital gains. If this financial alchemy results in lower taxes, it should be welcomed by any taxpaying investor. That is the basic point made by the leftist party when it argues for repurchases instead of dividends.

There is no doubt that high taxes on dividends can make a difference. The leftists quickly run into two problems, however. First, if they are right, why should any firm ever pay a cash dividend? If cash is paid out, repurchases should always be the best channel as long as the firm has taxable shareholders.[1] Second, the difference in the tax rate has now disappeared for both are taxed at rates of 0%, 15%, or a maximum of 20% depending on income.[2] However, capital gains still offer some tax advantage, even at these low rates. Taxes on dividends have to be paid immediately, but taxes on capital gains can be deferred until shares are sold and gains realized. The longer investors wait to sell, the lower the PV of their tax liability.[3]

The distinction between dividends and capital gains is not important for many financial institutions, which operate free of all taxes. For example, pension funds are not taxed. These funds hold $5.7 trillion of common stocks, so their clout in the U.S. stock market is enormous. Only corporations have a tax reason to prefer cash dividends. They pay corporate income tax on only 50% of dividends received.[4] So, for each $1 of dividends received, the firm gets to keep 1 – (.50 X .21) = $.895. Thus the effective tax rate is only 10.5%. But corporations have to pay 21% tax on interest income or realized capital gains.

1. Empirical Evidence on Dividends and Taxes

It is hard to deny that taxes are important to investors. You can see that in the bond market. Interest on municipal bonds is not taxed, and so municipals usually sell at low pretax yields. Interest on federal government bonds is taxed, so these bonds sell at higher pretax yields. It does not seem likely that investors in bonds just forget about taxes when they enter the stock market.

There is some evidence that in the past taxes have affected U.S. investors’ choice of stocks.[5] Lightly taxed institutional investors have tended to hold high-yield stocks and retail investors have preferred low-yield stocks. Moreover, this preference for low-yield stocks has been somewhat more marked for high-income individuals. Nevertheless, taxes have not deterred individuals in high-tax brackets from holding substantial amounts of dividend-paying stocks.

If investors are concerned about taxes, we might also expect that when the tax penalty on dividends is high, companies would think twice about increasing dividend payout. Only about a fifth of U.S. financial managers cite investor taxes as an important influence when the firm makes its dividend decision. On the other hand, firms have sometimes responded to major shifts in the way that investors are taxed. For example, when Australia introduced a tax change in 1987 that effectively eliminated the tax penalty on dividends for Australian investors, firms became more willing to increase dividend payout.[6] Or consider the case of the 2011 tax reform in Japan, which raised the top marginal tax rate on dividend income from 10% to

43.6% for individuals who owned between 3% and 5% of the company’s stock. More than 50% of these investors sold their stock before the tax hike, and companies that continued to have such large investors rapidly adjusted their payout policies.[7]

If tax considerations are important, we would expect to find a tendency for high-dividend stocks to sell at lower prices and, therefore, to offer higher pretax returns, at least in past decades when tax rates on dividends were much higher than on capital gains. Unfortunately, the evidence for this tendency is ambiguous at best.[8]

Taxes are important, but cannot be the whole story of payout. Many companies paid generous dividends in the 1960s and 1970s, when U.S. tax rates on dividends were much higher than today. The shift from dividends to repurchases accelerated in the 2000s, when tax rates on both dividends and capital gains were much lower than historical levels. Payout has also shifted to repurchases in countries such as Australia which have imputation tax systems that remove the double taxation of dividends.

Nevertheless, it seems safe to say that the tax advantages of repurchases are one reason that they have grown so much in the United States and other developed economies.

2. Alternative Tax Systems

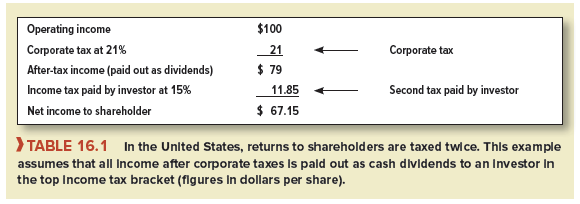

In the United States, shareholders’ returns are taxed twice. They are taxed at the corporate level (corporate tax) and in the hands of the shareholder (income tax or capital gains tax). These two tiers of tax are illustrated in Table 16.1, which shows the after-tax return to the shareholder if the company distributes all its income as dividends. We assume the company earns $100 a share before tax and therefore pays corporate tax of .21 x 100 = $21. This leaves $79 a share to be paid out as a dividend, which is then subject to a second layer of tax. For example, a shareholder who is taxed at 15% pays tax on this dividend of .15 x 79 = $11.85. Only a tax-exempt pension fund or charity would retain the full $79.

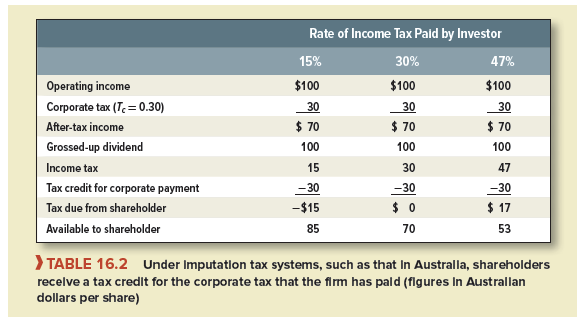

Of course, dividends are regularly paid by companies that operate under very different tax systems. In some countries, such as Australia and New Zealand, shareholders’ returns are not taxed twice. For example, in Australia shareholders are taxed on dividends, but they may deduct from this tax bill their share of the corporate tax that the company has paid. This is known as an imputation tax system. Table 16.2 shows how the imputation system works.

Suppose that an Australian company earns pretax profits of A$100 a share. After it pays corporate tax at 30%, the profit is A$70 a share. The company now declares a net dividend of A$70 and sends each shareholder a check for this amount. This dividend is accompanied by a tax credit saying that the company has already paid A$30 of tax on the shareholder’s behalf. Thus shareholders are treated as if they received a total, or gross, dividend of 70 + 30 = A$100 and paid tax of A$30. If the shareholder’s tax rate is 30%, there is no more tax to pay and the shareholder retains the net dividend of A$70. If the shareholder pays tax at the top personal rate of 47%, then he or she is required to pay an additional $17 of tax; if the tax rate is 15% (the rate at which Australian pension funds are taxed), then the shareholder receives a refund of 30 – 15 = A$15.[9]

Under an imputation tax system, millionaires have to cough up the extra personal tax on dividends. If this is more than the tax that they would pay on capital gains, then millionaires would prefer that the company does not distribute earnings. If it is the other way around, they would prefer dividends.[10] Investors with low tax rates have no doubts about the matter. If the company pays a dividend, these investors receive a check from the revenue service for the excess tax that the company has paid; therefore, they prefer high payout rates.

Look once again at Table 16.2 and think what would happen if the corporate tax rate were zero. The shareholder with a 15% tax rate would still end up with A$85, and the shareholder with the 47% rate would still receive A$53. Thus, under an imputation tax system, when a company pays out all its earnings, there is effectively only one layer of tax—the tax on the shareholder. The revenue service collects this tax through the company and then sends a demand to the shareholder for any excess tax or makes a refund for any overpayment.[11]

24 Jun 2021

25 Jun 2021

25 Jun 2021

25 Jun 2021

24 Jun 2021

24 Jun 2021