On most workdays, the financial manager concentrates on valuing projects, arranging financing, and helping to run the firm more effectively. The valuation of the business as a whole is left to investors and financial markets. But on some days, the financial manager has to take a stand on what an entire business is worth. When this happens, a big decision is typically in the offing. For example:

- If firm A is about to make a takeover offer for firm B, then A’s financial managers have to decide how much the combined business A + B is worth under A’s management. This task is particularly difficult if B is a private company with no observable share price.

- If firm C is considering the sale of one of its divisions, it has to decide what the division is worth in order to negotiate with potential buyers.

- When a firm goes public, the investment bank must evaluate how much the firm is worth in order to set the issue price.

- If a mutual fund owns shares in a company that is not traded, then the fund’s directors are obliged to estimate a fair value for those shares. If the directors do a sloppy job of coming up with a value, they are liable to find themselves in court.

In addition, thousands of analysts in stockbrokers’ offices and investment firms spend every workday burrowing away in the hope of finding undervalued firms. Many of these analysts use the valuation tools we are about to cover.

In Chapter 4, we took a first pass at valuing free cash flows from an entire business. We assumed then that the business was financed solely by equity. Now we will show how WACC can be used to value a company that is financed by a mixture of debt and equity. You just treat the company as if it were one big project. You forecast the company’s free cash flows (the hardest part of the exercise) and discount back to present value. But be sure to remember three important points:

- If you discount at WACC, cash flows have to be projected just as you would for a capital investment project. Do not deduct interest. Calculate taxes as if the company were all-equity-financed. (The value of interest tax shields is not ignored, because the after-tax cost of debt is used in the WACC formula.)

- Unlike most projects, companies are potentially immortal. But that does not mean that you need to forecast every year’s cash flow from now to eternity. Financial managers usually forecast to a medium-term horizon and add a terminal value to the cash flows in the horizon year. The terminal value is the present value at the horizon of all subsequent cash flows. Estimating the terminal value requires careful attention because it often accounts for the majority of the company’s value.

- Discounting at WACC values the assets and operations of the company. If the object is to value the company’s equity, that is, its common stock, don’t forget to subtract the value of the company’s outstanding debt.

Here’s an example.

1. Valuing Rio Corporation

Sangria is tempted to acquire the Rio Corporation, which is also in the business of promoting relaxed, happy lifestyles. Rio has developed a special weight-loss program called the Brazil Diet, based on barbecues, red wine, and sunshine. The firm guarantees that within three months you will have a figure that will allow you to fit right in at Ipanema or Copacabana beach in Rio de Janeiro. But before you head for the beach, you’ve got the job of working out how much Sangria should pay for Rio.

Rio is a U.S. company. It is privately held, so Sangria has no stock market price to rely on. Rio is in the same line of business as Sangria, so we will assume that it has the same business risk as Sangria, and, like Sangria, its debt capacity is 40% of firm value. Therefore, we can use Sangria’s WACC.

Your first task is to forecast Rio’s free cash flow (FCF). Free cash flow is the amount of cash that the firm can pay out to investors after making all investments necessary for growth. Free cash flow is calculated assuming the firm is all-equity-financed. Discounting the free cash flows at the after-tax WACC gives the total value of Rio (debt plus equity). To find the value of its equity, you will need to subtract the 40% of the firm that can be financed with debt.

We will forecast each year’s free cash flow out to a valuation horizon (H) and predict the business’s value at that horizon (PVH). The cash flows and horizon value are then discounted back to the present:

Of course, the business will continue after the horizon, but it’s not practical to forecast free cash flow year by year to infinity. PVH stands in for the value in year H of free cash flow in periods H + 1, H + 2, etc.

Free cash flow and net income are not the same. They differ in several important ways:

- Income is the return to shareholders, calculated after interest expense. Free cash flow is calculated before interest.

- Income is calculated after various noncash expenses, including depreciation. Therefore, we will add back depreciation when we calculate free cash flow.

- Capital expenditures and investments in working capital do not appear as expenses on the income statement, but they do reduce free cash flow.

Free cash flow can be negative for rapidly growing firms, even if the firms are profitable, because investment exceeds cash flow from operations. Negative free cash flow is normally temporary, fortunately for the firm and its stockholders. Free cash flow turns positive as growth slows down and the payoffs from prior investments start to roll in.

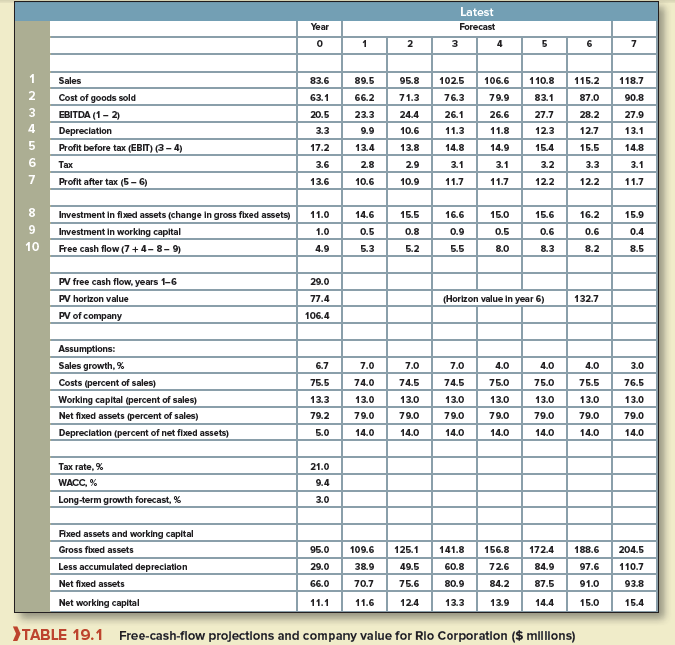

Table 19.1 sets out the information that you need to forecast Rio’s free cash flows. We will follow common practice and start with a projection of sales. In the year just ended, Rio had sales of $83.6 million. In recent years, sales have grown between 5% and 8% a year. You forecast that sales will grow about 7% a year for the next three years. Growth will then slow to 4% for years 4 to 6 and to 3% starting in year 7.

The other components of cash flow in Table 19.1 are driven by these sales forecasts. For example, you can see that costs are forecasted at 74% of sales in the first year with a gradual increase to 76.5% of sales in later years, reflecting increased marketing costs as Rio’s competitors gradually catch up.

Increasing sales are likely to require further investment in fixed assets and working capital. Rio’s net fixed assets are currently about $.79 for each dollar of sales. Unless Rio has surplus capacity or can squeeze more output from its existing plant and equipment, its investment in fixed assets will need to grow along with sales. Therefore, we assume that every dollar of sales growth requires an increase of $.79 in net fixed assets. We also assume that working capital grows in proportion to sales.

Rio’s free cash flow is calculated in Table 19.1 as profit after tax, plus depreciation,5 minus investment. Investment is the change in the stock of (gross) fixed assets and working capital from the previous year. For example, in year 1:

Free cash flow = Profit after tax + depreciation – investment in fixed assets – investment in working capital

= 10.6 + 9.9 – (109.6 – 95.0) – (11.6 – 11.1) = $5.3 million

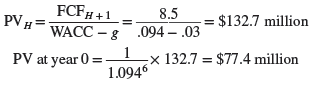

2. Estimating Horizon Value

We will forecast cash flows for each of the first six years. After that, Rio’s sales are expected to settle down to stable, long-term growth starting in year 7. To find the present value of the cash flows in years 1 to 6, we discount at the 9.4% WACC:

Now we need to find the value of the cash flows from year 7 onward. In Chapter 4, we looked at several ways to estimate horizon value. Here we will use the constant-growth DCF formula. This requires a forecast of the free cash flow for year 7, which we have worked out in the final column of Table 19.1, assuming a long-run growth rate of 3% per year.[1] The free cash flow is $8.5 million, so

We now have all we need to value the business:

PV(company) = PV(cash flow years 1 to 6) + PV(horizon value)

= $29.0 + 77.4 = $106.4 million

This is the total value of Rio. To find the value of the equity, we simply subtract the 40% of firm value that will be financed with debt:

Value of debt = .40 X 106.4 = $42.6 million

Total value of equity = $106.4 – 42.6 = $63.8 million

If Rio has 1.5 million shares outstanding, its value per share is:

Value per share = 63.8/1.5 = $42.53

Thus, Sangria could afford to pay up to about $42 per share for Rio.

You now have an estimate of the value of Rio Corporation. But how confident can you be in this figure? Notice that only about a quarter of Rio’s value comes from cash flows in the first six years. The rest comes from the horizon value. Moreover, this horizon value can change in response to minor changes in assumptions. For example, if the long-run growth rate is 4% rather than 3%, firm value increases from $106.4 million to $110.5 million.

Thus, faster growth increases Rio’s horizon value and PV(company). At this point, we must check the two warnings from the concatenator valuation example in Chapter 4. Did we account for the extra investment required to support the faster long-run growth? Yes. Growth at 4% instead of 3% increases year 7’s investment in fixed assets from $15.9 to $16.9 million and investment in working capital from $0.4 to $0.6 million. (To confirm this, go to the Rio Spreadsheet Beyond the Page and change the long-run growth rate.) Did we assume that Rio can earn more that its cost of capital in perpetuity? Yes, because the increased investment in year 7 and after added NPV. In other words, the horizon value contains positive PVGO, the present value of growth opportunities.

Will competition eliminate the PVGO? The financial manager will have to think hard about the competitive landscape. Perhaps he or she will decide that the long-run cost forecast at 76.5% of sales is too optimistic.

The financial manager will probably also look at the values that investors place on comparable listed companies. For example, suppose that similar lifestyle companies commonly trade at a ratio of company value to EBITDA of 4.8. Then Sangria’s manager might judge that Rio’s horizon value is 4.8 X $27.9 million = $133.9 million in year 6 and $78.1 million discounted to year 0. This would suggest that Rio is currently worth $29.0 + 78.1 = $107.1 million, marginally higher than our initial DCF estimate. The manager might also look at the market-to- book ratio for comparable businesses and calculate what Rio would be worth if it sold at a similar ratio.

Financial managers should also check whether a business is worth more dead than alive. Sometimes a company’s liquidation value exceeds its value as a going concern. Sometimes financial analysts can ferret out idle or underexploited assets that would be worth much more if sold to someone else. Such assets would be valued at their likely sale price and the rest of the business valued without them.

3. WACC vs. the Flow-to-Equity Method

When valuing Rio, we forecasted the cash flows assuming all-equity financing and we used the WACC to discount these cash flows. The WACC formula picked up the value of the interest tax shields. Then, to find the equity value, we subtracted the value of debt from the total value of the firm.

If our task is to value a firm’s equity, there’s an obvious alternative to discounting the total cash flows at the firm’s WACC: Discount cash flows to equity after interest and after taxes at the cost of equity capital. This is called the flow-to-equity method. If the company’s debt ratio is constant over time, the flow-to-equity method should give the same answer as discounting total cash flows at the WACC and then subtracting the value of the debt.

Suppose that you are asked to value Rio by the flow-to-equity method, assuming that the company adjusts its debt each year to maintain a constant debt ratio. You are given as a starter an estimate of Rio’s horizon value at the end of year 6. Perhaps this value was obtained by discounting subsequent cash flows by Rio’s WACC or perhaps it was estimated by l ooking at how investors value comparable, publicly traded companies. You decide to expand the spreadsheet in Table 19.1 by calculating each year’s interest payments and issues or repayments of debt. You recompute taxes, recognizing that the interest payments are a tax-deductible expense. Finally, you discount the free cash flow to equity at the cost of equity, which in our example is rE = 12.5%.

It sounds straightforward, but in practice, it can be tricky to do it right. The problem arises because each year’s interest payment depends on the amount of debt at the start of the year, and this depends in turn on Rio’s value at the start of the year (remember Rio’s debt is a constant proportion of value). So you seem to have a catch-22 situation in which you first need to know Rio’s value each year before you can go on to calculate and discount the cash flows to equity. Fortunately, a simple formula allows you to solve simultaneously for the company’s value and the cash flow in each year. We won’t get into that here, but if you would like to see how the flow-to-equity method can be used to value Rio, click on the nearby Beyond the Page feature to access the worked example.

Great write-up, I am normal visitor of one’s blog, maintain up the excellent operate, and It is going to be a regular visitor for a long time.

I dugg some of you post as I cerebrated they were very useful extremely helpful