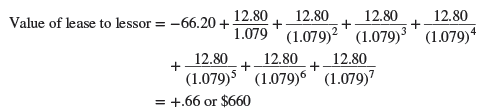

We have examined the value of a lease from the viewpoint of the lessee. The lessor’s criterion is simply the reverse. As long as lessor and lessee are in the same tax bracket, every cash outflow to the lessee is an inflow to the lessor, and vice versa. In our numerical example, the bus manufacturer would project cash flows in a table like Table 25.2, but with the signs reversed. The value of the lease to the bus manufacturer would be

In this case, the values to lessee and lessor exactly offset (-$660 + $660 = 0). The lessor can win only at the lessee’s expense.

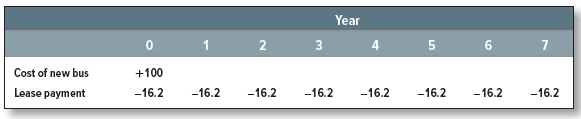

But both lessee and lessor can win if their tax rates differ. Suppose that Greymare paid no tax (Tc = 0). Then the only cash flows of the bus lease would be

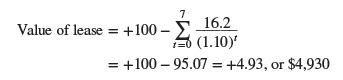

These flows would be discounted at 10% because rD(1 – Tc) = rD when Tc = 0. The value of the lease is

In this case, there is a net gain of $660 to the lessor (who has the 21% tax rate) and a net gain of $4,930 to the lessee (who pays zero tax). This mutual gain is at the expense of the government. On the one hand, the government gains from the lease contract because it can tax the lease payments. On the other hand, the contract allows the lessor to take advantage of depreciation and interest tax shields that are of no use to the lessee. However, because the depreciation is accelerated and the interest rate is positive, the government suffers a net loss in the present value of its tax receipts as a result of the lease.

Now you should begin to understand the circumstances in which the government incurs a loss on the lease and the other two parties gain. Other things being equal, the combined gains to lessor and lessee are highest when

- The lessor’s tax rate is substantially higher than the lessee’s.

- The depreciation tax shield is received early in the lease period.

- The lease period is long and the lease payments are concentrated toward the end of the period.

- The interest rate rD is high—if it were zero, there would be no advantage in present value terms to postponing tax.

Leasing around the World

In most developed economies, leasing is widely used to finance investment in plant and equipment.[1] But there are important differences in the treatment of long-term financial leases for tax and accounting purposes. For example, some countries allow the lessor to use depreciation tax shields, just as in the United States. In other countries, the lessee claims depreciation deductions. Accounting usually follows suit.

A number of big-ticket leases are cross-border deals. Cross-border leasing can be attractive when the lessor is located in a country that offers generous depreciation allowances. The ultimate cross-border transaction occurs when both the lessor and the lessee can claim depreciation deductions. Ingenious leasing companies look for such opportunities to double-dip. Tax authorities look for ways to stop them.[2]

25 Jun 2021

24 Jun 2021

24 Jun 2021

25 Jun 2021

24 Jun 2021

16 Jan 2018