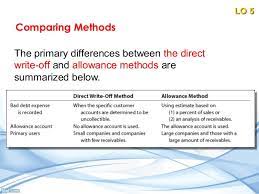

Comparing Direct Write-Off and Allowance Methods

Journal entries for the direct write-off and allowance methods are illustrated and compared in this section. As a basis for illustration, the following transactions, taken from the records of Hobbs Co. for the year ending December 31, 2013, are used: Mar. 1. Wrote off account of C. York, $3,650. Apr. 12. Received $2,250 as