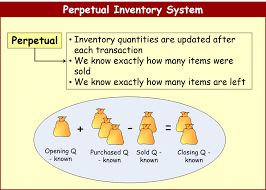

The Periodic Inventory System

Throughout this chapter, the perpetual inventory system was used to record purchases and sales of merchandise. Not all merchandise businesses, however, use the perpetual inventory system. For example, small merchandise businesses, such as a local hardware store, may use a manual accounting system. A manual perpetual inventory system is time consuming and costly to